Top European Undervalued Small Caps With Insider Action In April 2026

Uncategorized

Top European Undervalued Small Caps With Insider Action In April 2026

08 mins

As European markets experience a notable upswing, with the STOXX Europe 600 Index climbing over 3% amid improved geopolitical conditions, investors are keenly observing the small-cap segment for opportunities. In this environment of cautious optimism, identifying stocks that demonstrate strong fundamentals and potential insider confidence can be crucial in navigating the evolving market landscape.

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Value Rating: ★★★★☆☆

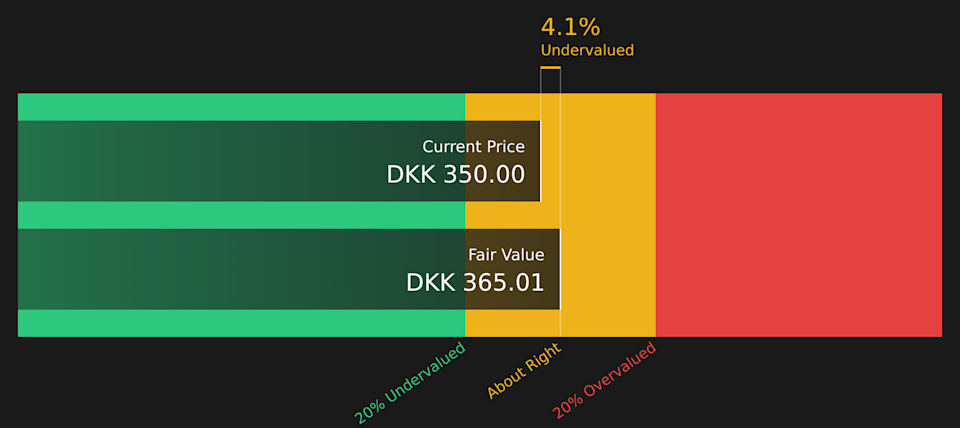

Overview: Gubra is a company that specializes in contract research organization (CRO) services and biotechnology, with a focus on developing treatments for metabolic diseases, and has a market cap of DKK 1.96 billion.

Operations: The company generates revenue primarily from its Biotech segment, which significantly outpaces the CRO segment. Over recent periods, the gross profit margin has shown an upward trend, reaching 96.96% by December 2025. Operating expenses are largely driven by R&D and General & Administrative costs.

PE: 3.4x

Gubra, a biotechnology company, has recently reported impressive financial results for 2025 with sales soaring to DKK 2.6 billion from DKK 265.74 million the previous year and net income reaching DKK 1.7 billion compared to a loss previously. However, earnings are expected to decline by an average of 37% annually over the next three years. The company has launched Gubra Ventures to foster biotech innovation while its clinical trial application for GUB-UCN2 aims at addressing obesity-related issues through innovative therapies. Despite high external borrowing risks, insider confidence is reflected in share purchases over recent months, indicating potential value recognition within this small-cap stock’s strategic initiatives and growth prospects.

CPSE:GUBRA Share price vs Value as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

Overview: CellaVision is a Swedish company specializing in digital solutions for medical microscopy, primarily focusing on hematology, with a market capitalization of approximately SEK 7.50 billion.

Operations: CellaVision generates revenue primarily through its sales, with recent figures showing SEK 758.97 million in revenue. The company’s gross profit margin has shown fluctuations, recently recorded at 68.50%. Operating expenses include significant allocations toward sales and marketing, as well as research and development efforts.

PE: 24.9x

CellaVision, a player in the digital cell morphology industry, recently launched its Bone Marrow Aspirate Application across EMEA, enhancing diagnostic capabilities for blood diseases. The application’s CE marking underlines its compliance with EU safety standards. Financially, CellaVision’s sales rose to SEK 759 million in 2025 from SEK 723 million the previous year, while net income increased to SEK 153 million. Insider confidence is evident as Christer Fahraeus acquired shares worth approximately US$15.69 million this year.

OM:CEVI Share price vs Value as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

Overview: Karnov Group is a provider of legal and tax information services, with operations primarily in the Nordic region and a market capitalization of SEK 4.28 billion.

Operations: The company generates revenue primarily from Region North and Region South, with recent figures indicating SEK 1.32 billion and SEK 1.32 billion respectively. Over the observed periods, its gross profit margin has shown variability, reaching as high as 52.99% in the past but most recently recorded at 43.65%. Operating expenses have fluctuated significantly, impacting net income margins which have varied widely from negative to positive values over time.

PE: 7.6x

Karnov Group, a player in the European market, has been actively reshaping its financial landscape. Recently, they announced an increase in their equity buyback plan to SEK 750 million as of March 25, 2026. This move aims to optimize capital structure and enhance shareholder value. Despite a forecasted earnings decline of nearly 30% annually over the next three years, insider confidence remains evident through significant share repurchases. The company posted a net income of SEK 970 million for the full year ending December 2025, reversing from a previous loss.

OM:KAR Share price vs Value as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CPSE:GUBRA OM:CEVI and OM:KAR.