Key Takeaways

- US stock market trading at 5% discount to our valuations

- Growth and value categories at similar discounts to fair value

- Opportune time to reallocate back to a barbell-shaped portfolio from overweight growth

- Elevated volatility expected to persist

Barbell Portfolio Reallocation Update

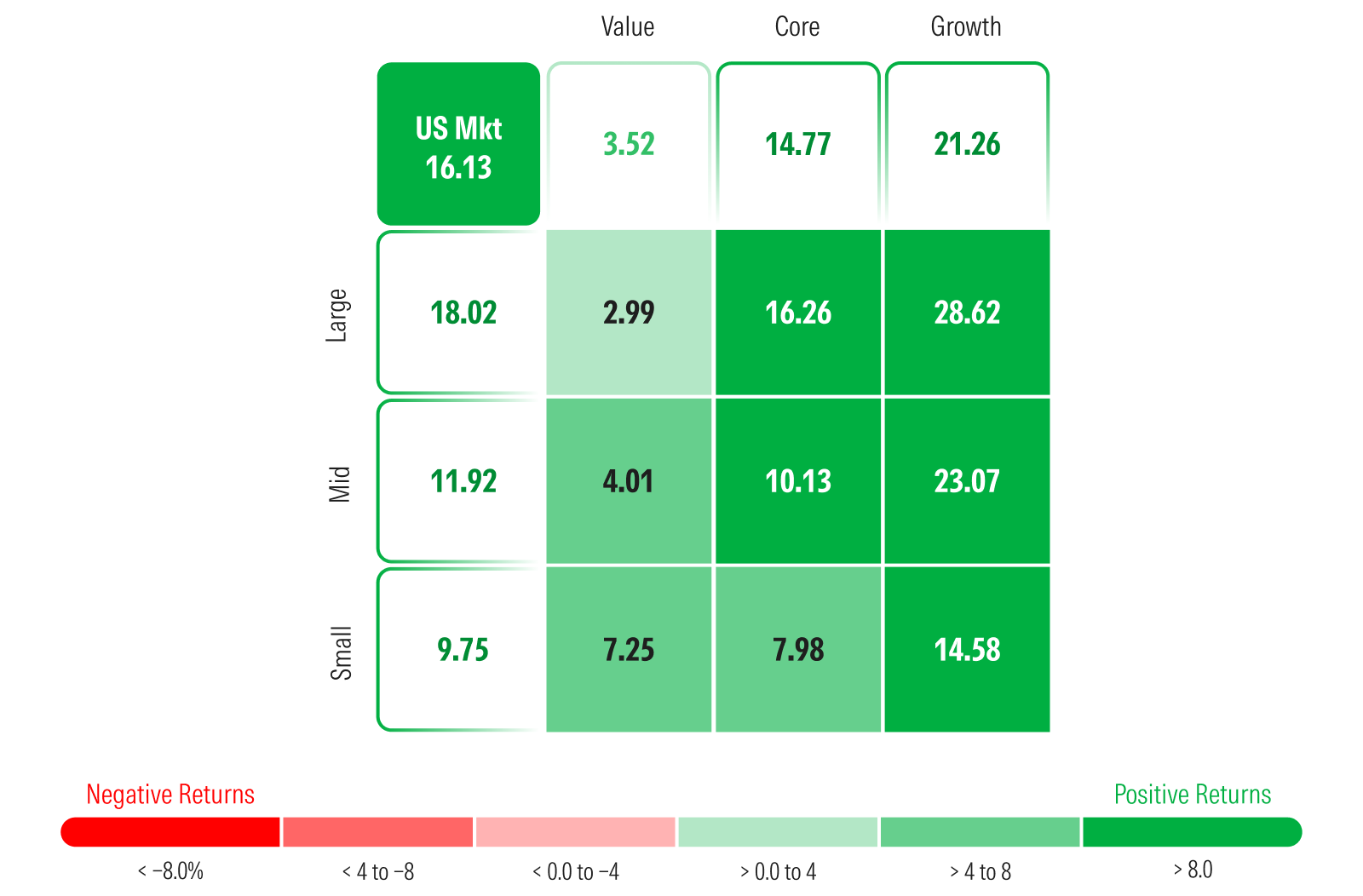

According to our valuations, now is an opportune time to harvest profits from being overweight in growth stocks and move back to a balanced barbell-shaped portfolio. On the March 30 episode of The Morning Filter, we recommended increasing allocations into the growth category (specifically into technology and AI stocks) by reallocating out of the value category (specifically energy stocks). Since then, growth (mainly technology and artificial intelligence) has rallied significantly, while value has only gained modestly. As long-term investors, we don’t try to time the market, but look to adjust portfolio positions when warranted as markets and valuations move.

From March 31 to May 29, the Morningstar US Growth Index has risen 21.26%, whereas value only increased by 3.52%. Over this period, nine of the top 10 contributors to the market return were directly tied to AI and contributed two-thirds of the total market return. The technology sector was by far the fastest-growing, rising 35.78% over the same time frame.

Looking forward, we think returning to a barbell-shaped portfolio (half value and half growth) provides the balance between protecting against downside volatility yet still allowing investors to participate in future upside.

The growth category is now trading at only a 5% discount to fair value, whereas on March 31, it was trading at a 19% discount, a much greater margin of safety than today. Value stocks are similarly valued at a 6% discount.

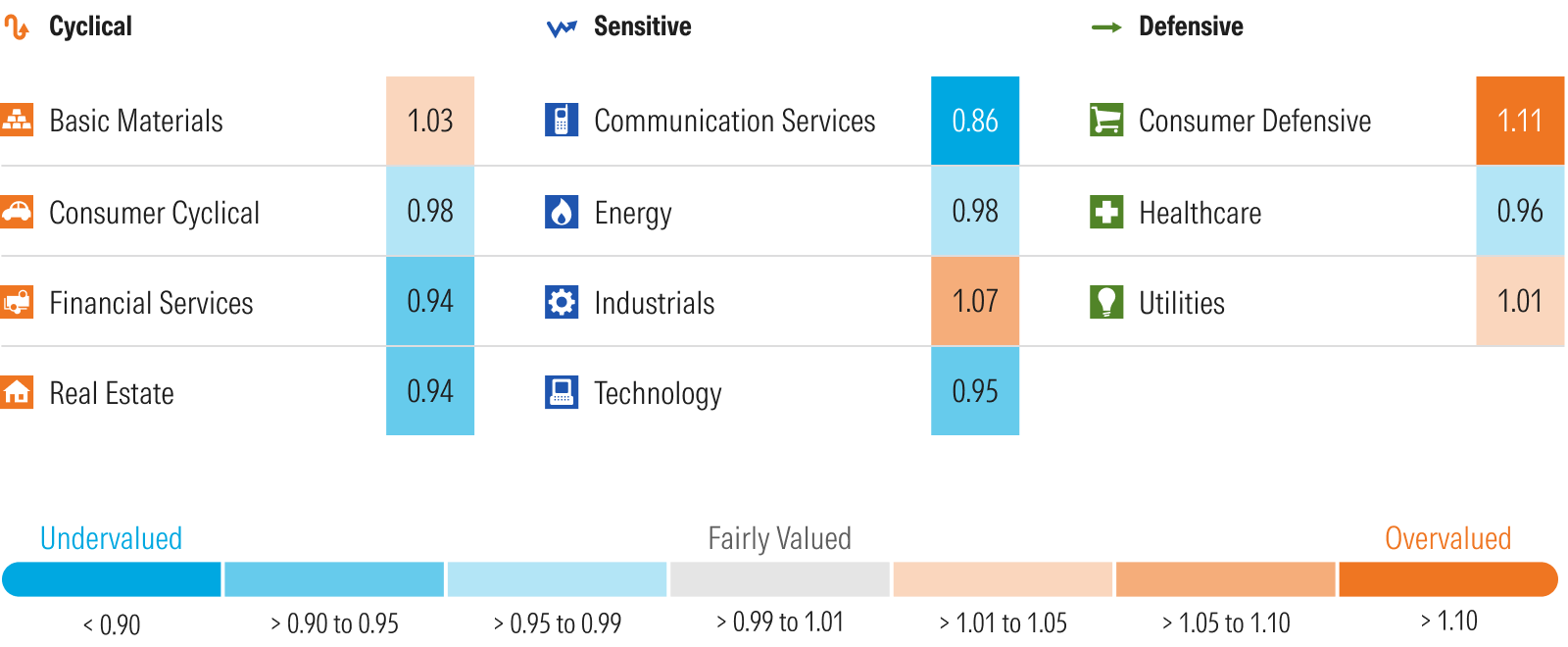

Sector Valuations

Communications is currently the most undervalued sector, trading at a 14% discount to fair value. Yet much of that discount is concentrated in Alphabet GOOGL and Meta Platforms META. Meta makes up almost 20% of our sector index and is trading at a 30% discount to our fair value. Alphabet accounts for 57% of the index and is trading at 14% discount.

The technology sector remains undervalued at a 7% discount to a composite of our fair valuations, but considering it was trading at a 25% discount on March 30, it no longer provides as much excess margin of safety. While stocks for commodity-oriented tech hardware have soared as the insatiable demand from the AI buildout boom has led to near-term shortages, we think the market is overestimating how long these companies will generate excess returns. In fact, many of these stocks are now some of the most overvalued under our US coverage. We see much better value in those stocks of companies that are at the forefront of AI technology. We also think the death of software by AI has been greatly exaggerated and see a number of stocks in the software industry as having sold off too much over the past year.

Financial services and real estate tie for the third most undervalued sector, trading at 5% discounts. The financial-services sector was the second most overvalued coming into the year and is the worst-performing sector for the year to date. We opined that the market was overestimating the amount of net interest income growth this year, and as it appears the Fed will not be lowering interest rates anytime soon, financials have retreated. Real estate started the year as the most undervalued sector and has performed admirably, rising almost 10% for the year to date. Within the real estate sector, we continue to prefer real estate with defensively oriented tenants and to steer clear of urban office space.

One of the greatest swings in valuation we have seen this year has occurred in the energy sector. In our 2026 US Market Outlook, we noted that energy started the year as one of the most undervalued sectors, trading at a 10% discount. As oil prices surged following the military conflict with Iran, energy rose to an 18% premium on March 31. As oil prices have subsided, energy stocks gave up those premiums and are now trading at only a 2% discount as of the end of May.

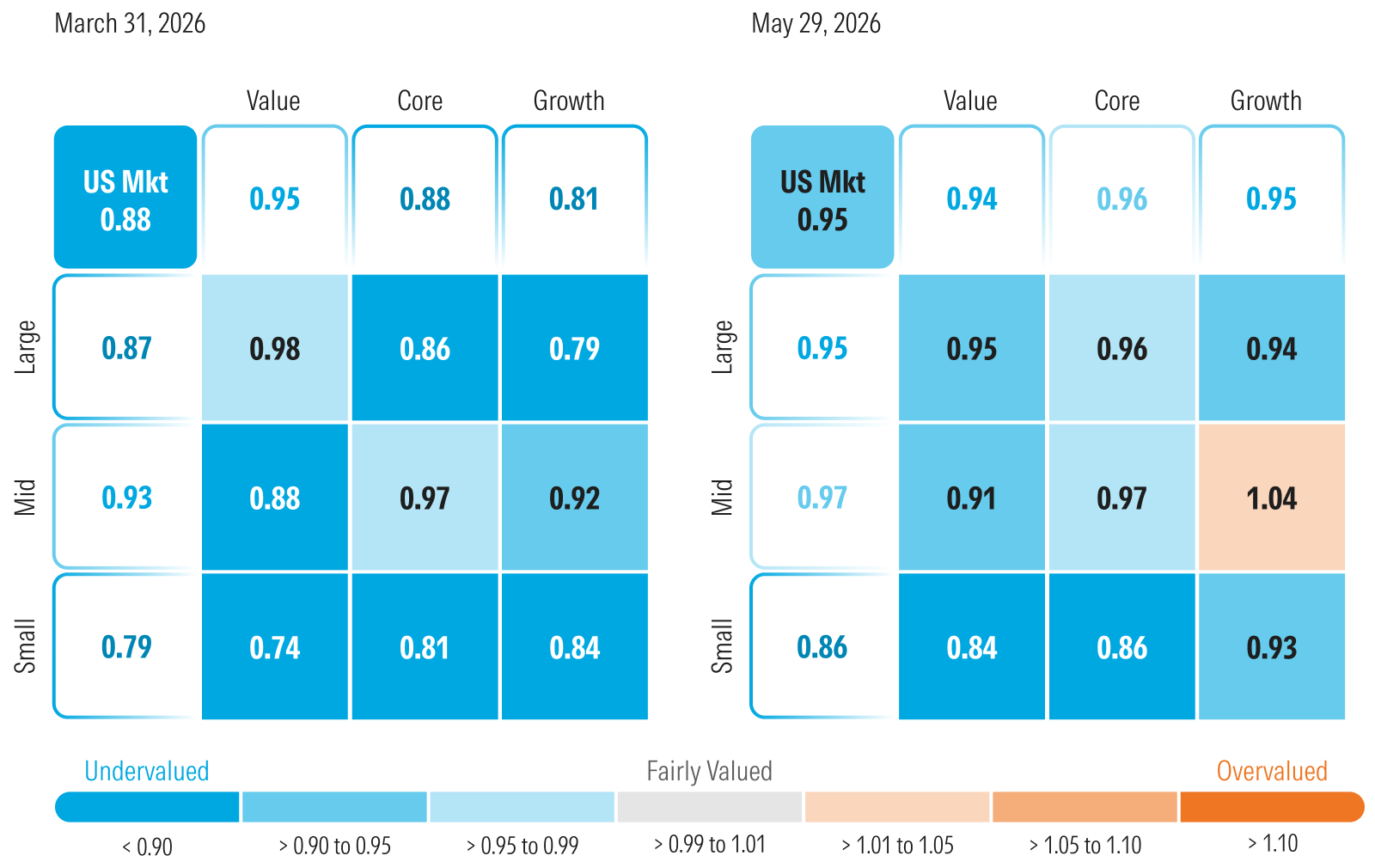

Following the Rally, US Stocks No Longer as Undervalued

As of May 29, 2026, the US equity market was trading at a 5% discount to a composite of our fair valuations.

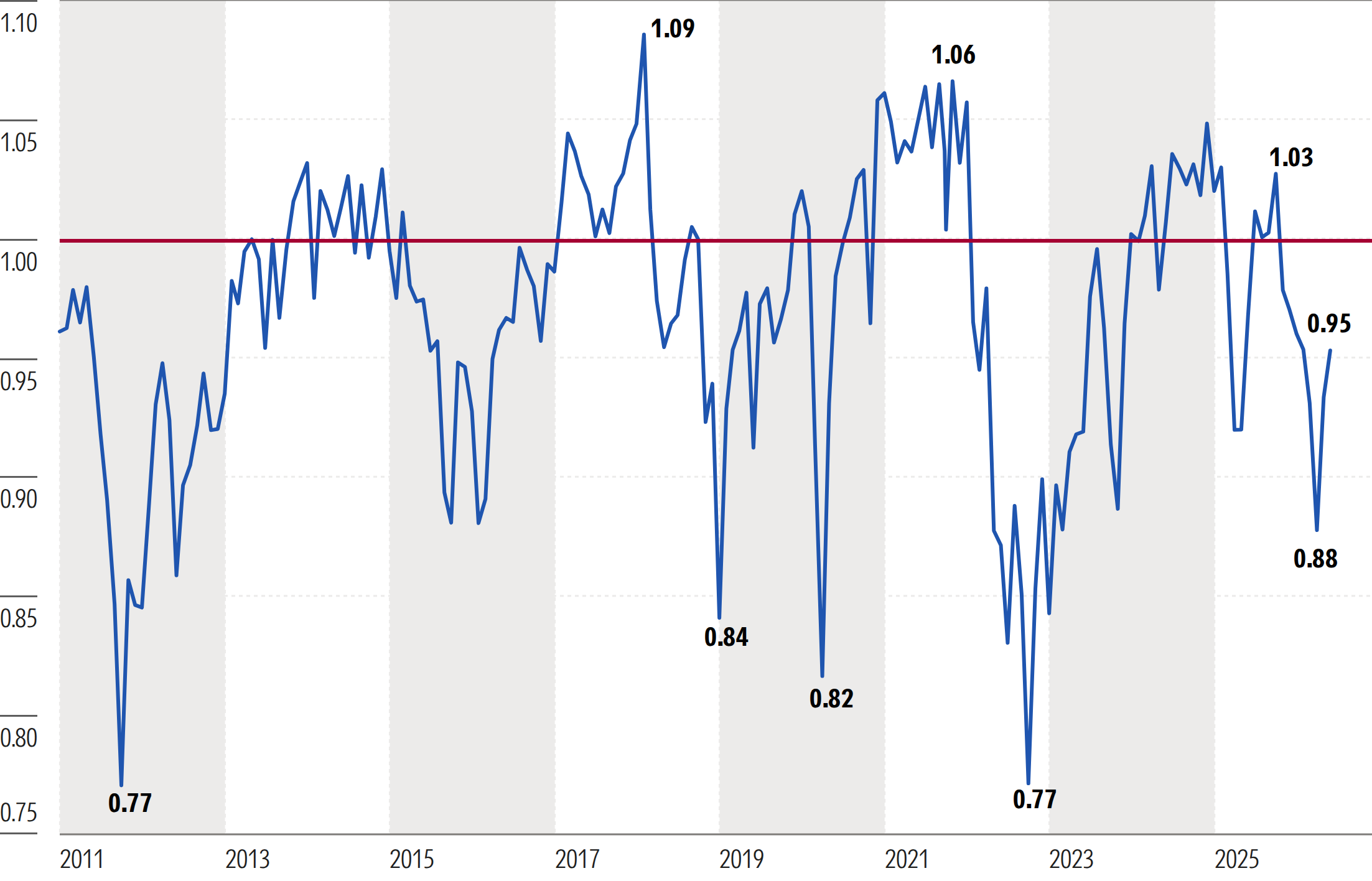

Elevated Volatility Likely to Persist

In our 2026 US Market Outlook, we warned that a number of emerging risks could make this year more volatile than last. To position portfolios for that environment, we recommended a barbell strategy: one side anchored in high-quality value stocks (especially undervalued energy), balanced by exposure to growth equities, especially undervalued technology and AI stocks.

The strategy behind this allocation remains intact. As we have seen over the past two months, during market rallies, we expect undervalued technology stocks (especially AI stocks) to outperform meaningfully. As those names approached fair value, investors could lock in gains and redeploy capital into lagging value stocks. Conversely, during periods of market stress (such as earlier this year), we expect the market to rotate out of growth into value. As value stocks near fair value, profits can be harvested and rotated back into undervalued growth opportunities. This disciplined rebalancing approach is designed to systematically capture dislocations created by volatile market conditions.

Many of the catalysts we expected to drive volatility remain unresolved, and several new risks have emerged:

- Momentum in AI-focused equities appears to be stalling

- Inflation is reaccelerating

- Interest rates are generally rising globally

- The Federal Reserve is likely constrained from cutting rates and will not be able to ease monetary policy

- Economic growth is heavily tied to the AI buildout boom

- Oil prices remain elevated amid ongoing geopolitical tensions with Iran

- Trade and tariff tensions are likely to reemerge as a market focus this summer

- Recent data indicate China’s economy is slowing more than expected

- President Donald Trump’s recent trip to China did not yield meaningful new agreements

- US midterm elections are approaching, adding another layer of uncertainty

Despite these risks, investment in the AI build-out boom remains full steam ahead, and the long-term opportunity in AI remains compelling.

We advocate for investors to maintain exposure to AI, but with a disciplined focus on valuation and competitive positioning. History suggests that during transformative tech cycles, it is critical to differentiate between companies with durable competitive advantages versus those benefiting primarily from shortages in commodity-oriented hardware as opposed to long-term changes in business dynamics.

We continue to favor companies at the forefront of AI innovation with strong, defensible market positions. In contrast, we remain cautious on more commoditized hardware providers, where stock price performance and momentum are driven by shorter-term excess gains that we expect to be competed away over time.