The US-Iran-deal stock market rally stalled where June’s meltdown began, even as the good news kept coming. Will the new Fed chair give traders a reason to cheer?

- Stocks paused right at their prior high, showing similar fading volume and momentum that preceded the last breakdown

- Crude oil kept falling and Hormuz headlines seemed hopeful, yet the sentiment boost evaporated anyway

- Kevin Warsh’s first meeting as Fed chair is ahead, yet a dovish policy pivot looks unlikely

Markets paused after an exuberant response to signs of a US-Iran peace deal. The striking part is where they paused — and what they ignored to do it. The bellwether S&P 500 climbed right back to the swing high where June’s meltdown began, then stalled, even as the very developments that inspired the rally kept unfolding.

The rally ran out of breath at the worst possible spot

The index returned to the level that capped it before the mid-June selloff, carrying the same warning signs as last time: fading volume and negative divergence on the relative strength index (RSI). Because this run set a marginally higher intraday high, that momentum divergence is now only more acute.

Tellingly, the pause arrived while the bullish catalyst was still playing out — crude oil kept falling as geopolitical risk continued to drain away. For example, Qatar floated the hopeful prospect of restoring up to 80% of natural gas capacity within two months of a durable reopening of the Strait of Hormuz. Yesterday that kind of news was a sentiment boon. Not so today.

Other key markets for the “war trade” tell the same story. Gold staged a bounce but stalled at former support turned resistance, its sequence of lower highs and lower lows intact. The US dollar pulled back only slightly before reasserting the uptrend it has held since April. Treasury bonds — whose prices move inversely to yields — remained locked in a narrow range, leaving the wartime rise in yields firmly entrenched. Across the board, the message seemed to be that traders are unwilling to extrapolate the peace dividend forward, at least for now.

A truce doesn’t undo the inflation scarring

The reason is that – from the markets’ perspective – the US-Iran deal seems to address the wrong problem. From the war’s first days, markets read it not as a geopolitical calamity but as an inflation shock: crude spiked, and that translated into higher yields, a firmer dollar, and softer gold. Easing tensions may pull the geopolitical risk premium out of near-term oil prices, but it does nothing for the inflationary scarring the shock has already left behind.

That damage is visible in the data — sharp upticks in warehousing and freight costs feeding core inflation in both the consumer price index (CPI) and producer price index (PPI) over recent months. Reopening Hormuz, whenever it happens, will not reverse what has already seeped into the cost structure. For now, the war’s legacy seems to be a structurally higher-rate environment, and that is what the bond market continues to say.

The Fed may be worried about more than oil

There is a subtler worry buried in the Federal Reserve’s own thinking. Its March projections raised expectations for growth and inflation — and crucially lifted the longer-run growth and interest-rate paths as well.

That combination is revealing. A pure energy shock is cost-push inflation, a jump in prices that would tend to drag growth down, not up. By marking growth higher alongside inflation, the Fed signaled it sees demand-pull pressure too — procyclical inflation from an economy speeding up, layered on top of the oil shock. The latest CPI fits: sticky core services inflation, the largest slice of the pie, is strengthening even as core goods prices slip on early signs of demand destruction, as seen in cars and auto parts.

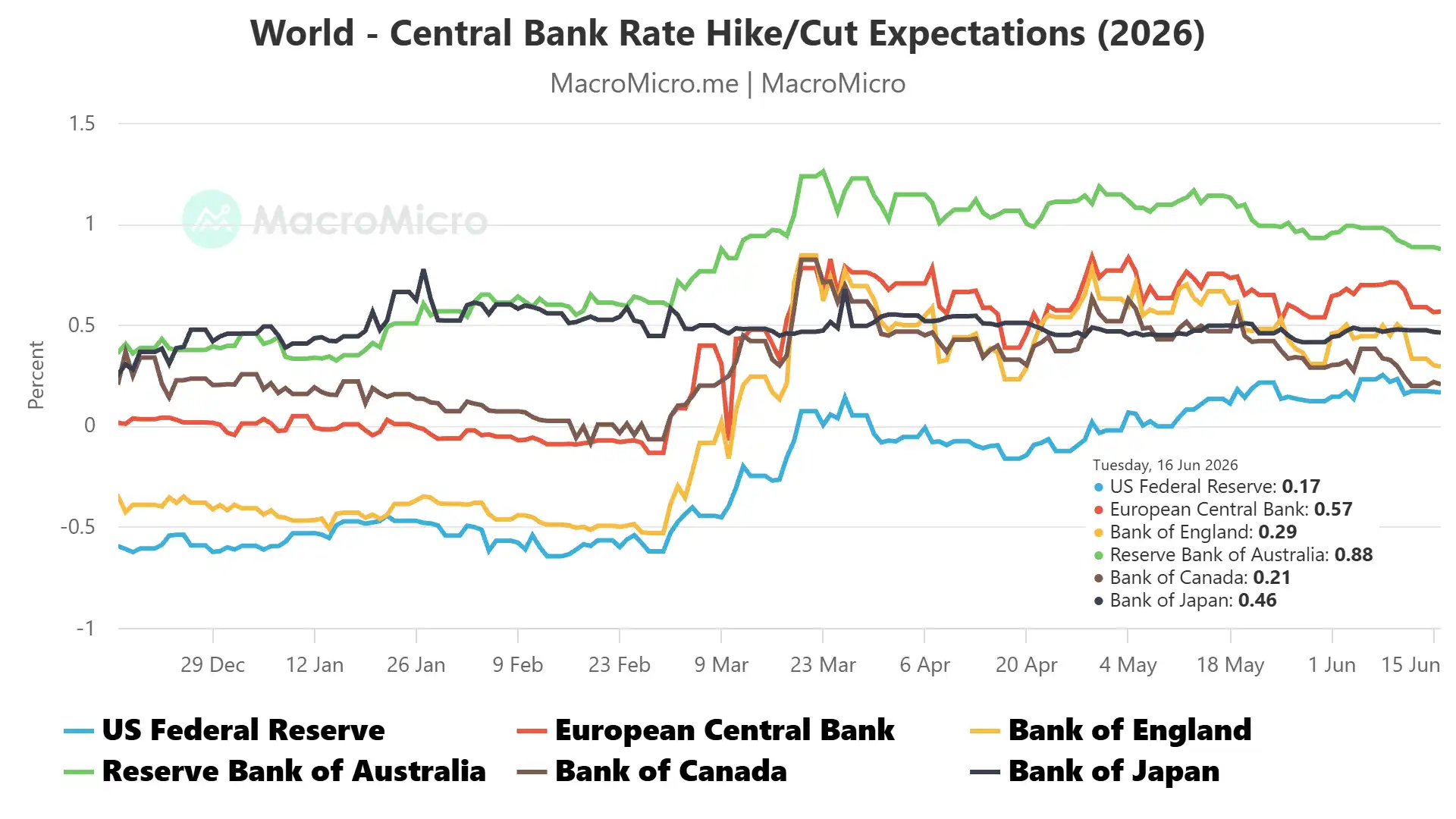

Other central banks are already acting on the same logic. This week the Reserve Bank of Australia (RBA) held after three straight hikes amid signs of weakening demand, while the Bank of Japan (BOJ) lifted rates to 1%, the highest since 1995, citing among other things the war’s knock-on effects on inflation.

For the Fed, interest rate futures now discount about 17 basis points (bps) of tightening by year-end. That puts the probability of a single 25bps rate hike at 68%, or slightly better than even. The cumulative math across a range of scenarios is starker: the odds of at least one hike are closer to 80%. The contrast with the 50bps of cuts expected back in January could hardly be sharper.

Why Warsh is unlikely to rescue the rally

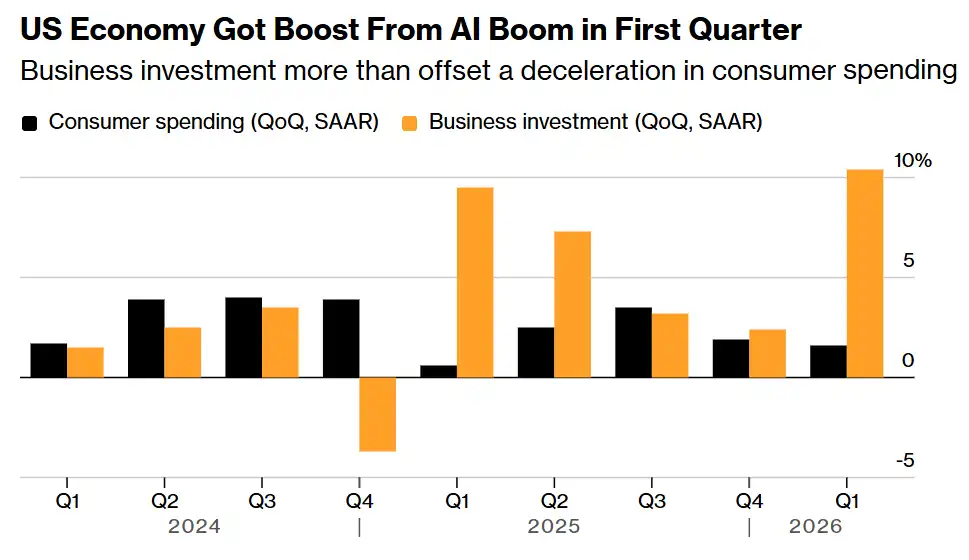

That backdrop traces to the fragile shape of US growth. First-quarter gross domestic product (GDP) clawed back only about half the ground lost to the fourth-quarter government shutdown, and it managed that only because business investment — about 14% of the economy — grew at a blistering 10.4% annualized clip and out-contributed consumption, which is 68% of output and decelerated for a second straight quarter.

An economy spinning one of its lesser engines that fast just to crawl forward may be overheating beneath a moderate-looking surface, an inflation risk all its own before the war’s scarring is even considered.

All of which lands on the first policy announcement under new Fed chair Kevin Warsh, due in less than 24 hours. The markets will parse his debut press conference for any hint of relief. The bullish hope is that a resolved war reopens the door to rate cuts.

The more likely message is the one the Fed delivered last time: that it is wary of inflation risk and content to stand aside while events wash over the economy. If that is what arrives, the stalled stock market rally may be left with little to sustain it, with the relief priced this week looking less like a turning point than a pause before the trend reasserts itself.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.