Investors have been warned over the risk of a summer correction as consumer credit indicators begin to show signs of stress.

America’s $2 trillion private credit industry is coming under increasing pressure, with high interest rates contributing to a worrying rise in defaults.

The war in Iran has sparked an energy price crisis, fuelling inflation and delaying rate cuts. As a result, the speculative-grade default rate is expected to rise to 4 per cent by March 2027, up from 3.9 per cent in March 2026.

That’s according to the latest assessment by analysts at S&P Global, who say the outlook for private credit is skewed to the downside, with the potential for the default rate to reach 5 per cent in a “pessimistic” scenario.

It comes after the ratings agency Fitch reported a rise in the private credit default rate to 6 per cent in April, the highest level on record. Analysts noted “sustained pressure on consumer issuers” as a result of both structural and cyclical headwinds.

Consumer defaults are often seen as an indirect but significant risk to the stock market – when consumers can’t pay off their mortgages, car loans or medical bills, corporate profits shrink and lending tightens.

It’s against this backdrop that the CEO of the deVere Group, Nigel Green, has warned investors to prepare for volatility ahead, and to countenance the possibility of a correction in the short to medium term.

Speaking on Friday, June 5, Green said that rising consumer defaults should give investors cause for concern:

“Right now, the American consumer is under serious pressure. The rate of delinquencies has hit a record high and 20 per cent of Americans now owe over $10,000 on a credit card.

“In all, American consumers now owe a collective $1.25 trillion, and that’s on credit cards alone.

“This level of debt is simply unsustainable. Making matters worse, inflation is coming in hot. Prices rose at their fastest level in three years in April as higher energy prices pass through onto consumer goods.

“We have to be prepared for a reckoning, and the possibility for a contraction in consumer spending – a major risk to the economy, and to markets.”

But consumer credit isn’t the only warning sign flashing amber. After a parabolic rally since early April, the S&P 500 is now up almost 15 per cent, and is trading around all-time highs.

Some analysts now believe the rally may be overbought, and that a correction could be on the cards. With the index now heavily concentrated among a small number of tech stocks, any setback in the sector could have an outsized downside impact in the markets.

In view of this concentration risk, renewed inflation, and rising consumer credit defaults, Green has advised investors to remain diversified, to help protect their portfolios from the threat of a correction:

“With this outlook, you’ve got to diversify. Right now energy prices are driving inflation, the Fed can’t cut rates and AI, the engine room of US equities, relies on significant debt-financed capex.

“What’s more, there is trouble brewing in the private debt market, with record numbers of delinquencies being reported and enormous credit card debts piling up.

“Put simply, something has to give. My argument is that in the face of this, investors should stay diversified. While there are still opportunities in the market, the risks are real too.

“Right now is a time for caution. There will be significant pressure over the summer and into the autumn.

“There will be opportunities; I think Nvidia is a great stock, but I believe there will be better times to buy stock like that in the future.”

Consumer Credit Defaults a ‘Warning Sign’

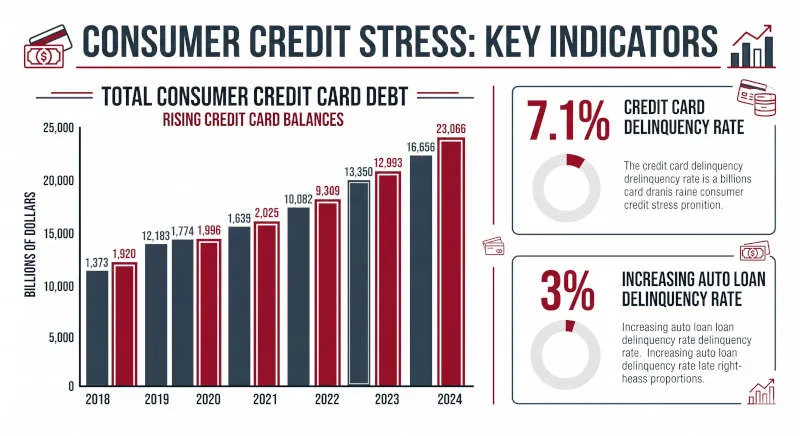

Household debt rose to $18.8 trillion in the first quarter, according to the New York Fed, while credit card balances stood at $1.25 trillion even after a seasonal decline.

The issue for markets is not just that consumers are borrowing more, but that borrowers are struggling to stay current.

The New York Fed said 4.8 per cent of outstanding household debt was in some stage of delinquency, with flows into serious delinquency on credit cards at 7.1 per cent and auto loans at almost 3 per cent.

If households are forced to divert more income towards interest payments, they have less to spend on discretionary goods and services. Retailers, restaurants, travel companies and carmakers are among the first to feel the squeeze, but the pressure can quickly spread to banks, lenders and credit funds.

There are already signs of strain beyond households. Reuters reported that unrealised losses at US private credit lenders reached their worst level since 2022 in the first quarter, while Fitch says US private credit defaults hit a record 6 per cent in April.

Investors Warned of Rising Stock Market Correction Risk

A number of fund managers are beginning to join a chorus of warnings, urging investors to be alive to the risk of a stock market correction in the short to medium term.

Managers are particularly alarmed by the soaring cost of government borrowing, after a sell-off in the bond markets sent US bond yields to their highest level in over a year.

For Vincent Mortier, chief investment officer of Amundi, the only question around a correction is ‘when, not if.’

A number of managers who spoke to the FT identified a clear discrepancy between the sentiment in the equity markets and the reality in the energy markets.

Among them, Raphaël Thuin, at Tikehau Capital, who said there was good reason to be “nervous” in the near term:

“There’s an incompatibility between having equities at all-time highs, [credit] spreads at tights, high bullishness . . . and at the same time, interest rates and energy [markets] pricing in a lasting impact on the economy,”

Short-term, there are good reasons to be nervous…It does feel like the rally is very stretched [and] the market is due a pause.”

This incongruity, between uber-bullishness in the stock market, and a depressed outlook for rate cuts and resurgent inflation, raises questions over the sustainability of today’s rally.

So far, investors have largely ignored the geopolitical turmoil and its fallout, with AI continuing to shrug off the headwinds and set new records.

But there may come a point where the chasm between sentiment and reality stretches to a breaking point.

That breaking point could come in the near future, if a recent poll of fund managers is to be believed. BofA’s latest survey found fund managers shifted to overweight on equities in April, but analysts at the bank said their Bull & Bear Indicator was approaching a “sell signal”, and warned of the potential for profit taking in June.

Strong corporate profits have been a key catalyst for the rally, but with earnings season nearing its end, sentiment could wane, and markets may go into retreat. That’s according to Nancy Tengler at Laffer Tengler, who believes once the good news is out of the headlines, minds will begin to focus on the reality of events in the Gulf:

“We’re a little bit concerned that the market’s going to test once earnings season is over in totality…Then we have a lack of news flow, so the market will turn its attention to the Fed, to the Middle East.”

Why The Correction Risk is Rising, but a Crash Remains Less Likely

While the rally may have road to run, investors have been urged to take the risk of a correction seriously.

The New York Fed says total household debt rose to $18.8 trillion in the first quarter, with credit-card balances still at $1.25 trillion and 4.8 per cent of outstanding debt in some stage of delinquency; flows into serious delinquency were 7.1 per cent for credit cards and almost 3 per cent for auto loans.

At the same time, the pressure is spreading up the credit chain. Unrealised losses at listed US private-credit lenders deepened to their worst level since 2022, and Blackstone has capped withdrawals at its flagship private-credit fund after investors sought to redeem 10 per cent of shares.

The Financial Stability Board warned in May that private credit’s leverage, opacity and interconnectedness could amplify stress in an adverse scenario. When the consumer is stretched, and lenders are marking down assets, equity investors cannot assume the problem will remain contained.

This comes against the backdrop of a market which is increasingly concentrated, with around 39 per cent of the S&P 500 now comprised by tech stocks, the highest share on record and well beyond levels seen during the dotcom bubble.

The equal-weight S&P 500 has lagged badly too, further evidence that the rally is being driven by a narrow group of giants rather than a broad advance across corporate America. In options markets, strategists have warned that demand for upside has become unusually aggressive, while record-low stock correlation can disguise fragility before a sudden burst of volatility.

The macro backdrop gives further cause for caution. Government bond yields have risen sharply, with the 10-year US Treasury around 4.6 per cent in May and the 30-year above 5 per cent, while the 60-day correlation between the S&P 500 and Treasury returns has climbed to its highest level in more than two decades.

Meanwhile, the IMF said this week that persistent energy shocks and tariff pass-through mean a return to the Fed’s 2 per cent inflation target is now not expected until the end of 2027, and Boston Fed researchers argue the current oil shock is more likely to feed inflation than trigger the kind of labour-market weakness that would force a swift pivot to rate cuts.

Even so, the balance of expert opinion still points more towards a correction than a crash. Citi has already trimmed equity exposure after the latest run, and Barclays said on Friday that momentum in AI and semiconductors looks shakier amid crowded positioning, looming liquidity events and policy risks.

With next week’s SpaceX IPO, fresh CPI data and earnings from Oracle and Adobe all on the calendar, the market may not need a major shock to pull back.