USD: Dollar rebounds as markets look past hot CPI print

May CPI did not give the Fed a clean report, but it did give markets enough to avoid a fresh panic. Headline inflation rose 0.5% on the month and 4.2% from a year earlier, the highest annual reading since April 2023, while core CPI came in at 0.2% on the month and 2.9% on the year, a touch softer than expected underneath the surface. Traders responded to the split, not the headline alone: Treasury yields backed off earlier highs, the two-year was around 4.12%, and the dollar eased slightly as the first reaction gave way to a more measured read. As markets digest the inflation story, fresh tensions between US and Iran see the US Dollar erasing weekly losses. With no end in sight in the Middle East conflict, the macro picture remains unchanged.

The headline was an energy story. The energy index rose 3.9% in May and accounted for more than 60% of the monthly increase in overall prices, while gasoline prices were up 40.5% from a year earlier. Other pressure points were visible as well: airline fares rose 26.7% year over year, shelter costs climbed 3.6%, and beef and veal prices were up 13.9%, a reminder that the squeeze is not limited to the pump. Markets largely saw it for what it was, another energy-led inflation burst, not clear evidence that every part of the basket is heating up again at once.

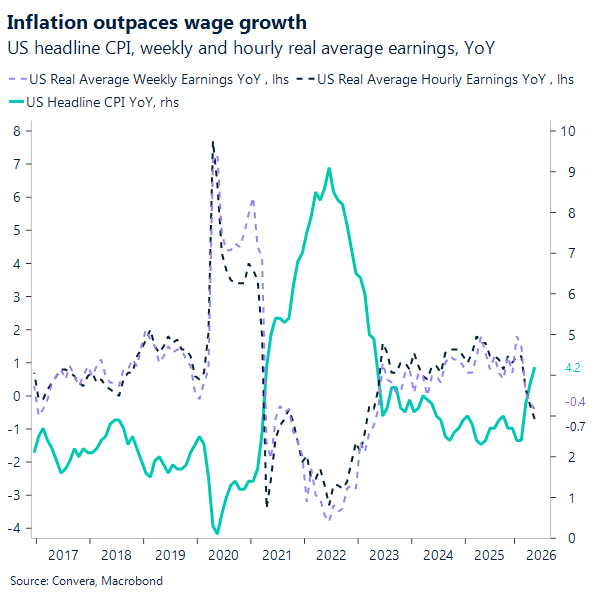

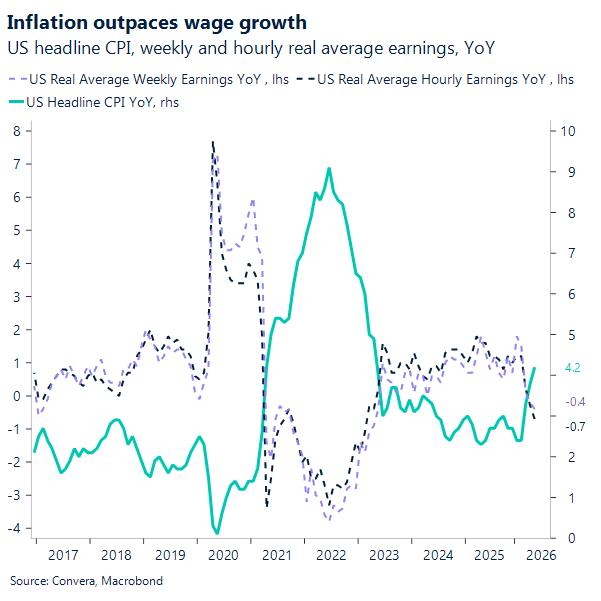

That distinction helps explain why the core details carried more weight than the headline shock. Core inflation is still too high for comfort, but a 0.2% monthly print is not the kind of number that forces the Fed to change course in June. The problem is that households are still losing ground: real average hourly earnings fell 0.7% from a year earlier in May, and real average weekly earnings fell 0.4%, extending the slide shown in the attached chart. Inflation is running ahead of wage growth again, which keeps pressure on consumption even if core CPI is not breaking higher in a straight line.

So the Fed is still boxed in. Markets continue to price roughly one 25-basis-point increase by year-end, with the implied policy midpoint around 3.87% versus 3.625% now, but the softer core print argues for a hawkish hold on June 17 rather than an immediate move. What comes next depends less on one CPI report than on whether oil stays elevated and whether supply shocks start seeping further into the core. With Middle East risk still hanging over energy and new bottlenecks tied to the AI buildout adding another layer of supply pressure, rates, the dollar and risk assets are still trading a market that sees no end in sight in the Middle East conflict.

CAD: The BoC trade got harder to call

The Bank of Canada delivered the hold markets expected. It left the policy rate at 2.25% for a fifth straight meeting, but the tone shifted in a more hawkish and more uncertain direction against the April message.

In April, the Bank said growth had resumed, inflation was expected to peak around 3% and then ease back, and any future rate changes would likely be small if the base case held. By June, that framework had weakened: first-quarter GDP had contracted 0.1%, inflation had risen to 2.8% in April, oil was running about $10 a barrel above the Bank’s earlier assumption, and policymakers said inflation could hover close to 3% for the next few months.

What changed most was the Bank’s description of the policy problem. In April, the message was that a rate near current settings looked broadly appropriate and that policy changes, if needed, would probably be small. In June, that line disappeared. Governor Tiff Macklem instead described economic weakness (not recession) and rising inflation as a dilemma, saying higher rates could further slow a soft economy while lower rates could let inflation become persistent.

The growth side of the story also turned less comfortable. In April, the Bank said growth had resumed after the late-2025 contraction and projected GDP would expand 1.2% this year. By June, it acknowledged that the economy had unexpectedly shrunk 0.1% in the first quarter, with weak business investment, softer housing activity and a pullback in government spending offsetting consumer demand. The Bank still expects growth to resume in the second quarter, but it now also says the economy is likely to remain in excess supply even if that rebound materializes.

Inflation is where the June statement became more uncomfortable. In April, the Bank expected inflation to rise to around 3% and then fall back toward target as oil prices eased toward US$75 by mid-2027. In June, it said inflation had already reached 2.8% in April, that oil prices remained elevated, and that CPI would likely hover close to 3% in coming months before easing only gradually. Policymakers also said they were still looking through the war’s near-term effect on headline inflation but made clear they would not tolerate broader pass-through into generalized price pressure.

That leaves the Bank with a more awkward reaction function than the market was trading a few weeks ago. It said outright that policy may need to move in either direction: rate cuts if the US imposes significant new trade restrictions on Canada, or consecutive hikes if high energy prices start feeding into persistent inflation. That is a sharper formulation than the April version and a harder one for markets to discount. Add the July 1 CUSMA review and tensions ahead of that review and the mix becomes more complicated.

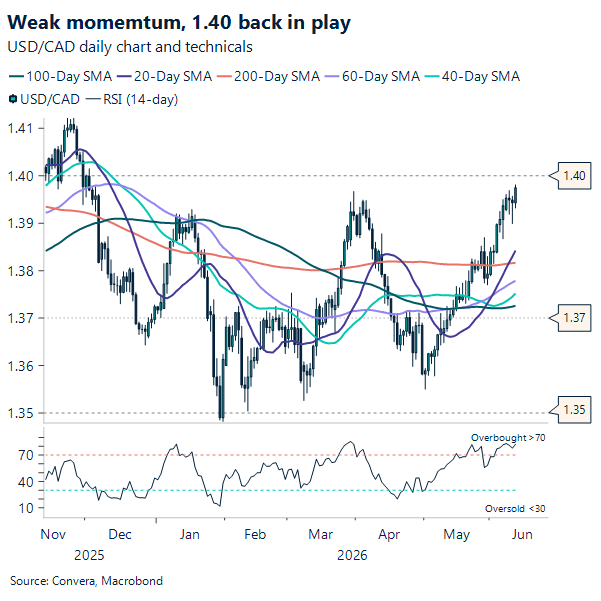

In FX, after trading for the most part of the week within the 1.39-1.395 range, upside pressure has built up against the USD/CAD, with the US Dollar seeing fresh bid on escalating rhetoric between US and Iran. The currency has hit a new 2026 high at 1.398. The 1.40 is back on play, while investors lean more bearish against the Loonie. Speculative positioning moved net short Canadian-dollar widening to 94,100 contracts from 68,900 a week earlier.

EUR: Insurance hike, limited lift

EUR/USD edged higher yesterday following a relatively tame US inflation report before pairing back gains on renewed tensions between the US and Iran. The ongoing impasse around Hormuz, combined with a still-resilient hawkish repricing narrative supporting the dollar, continues to cap attempts at a more forceful move back toward the 1.16 handle.

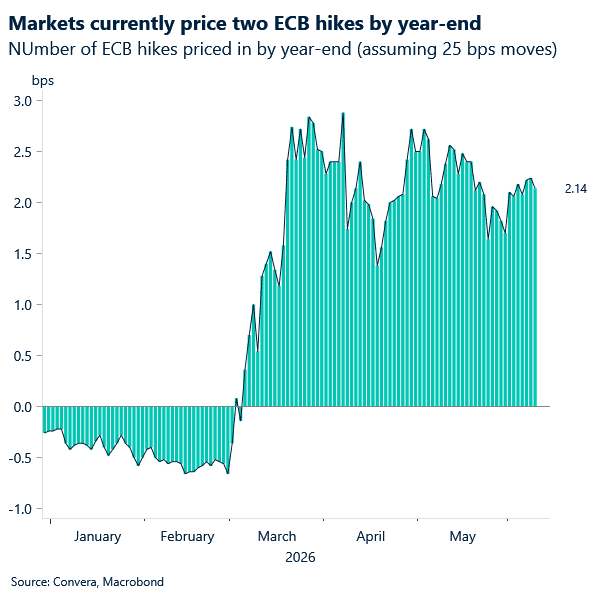

Focus now turns to today’s ECB policy meeting, with markets expecting a rate hike. The move is largely viewed as an insurance step, aimed at signalling readiness in an environment where accelerating inflation dovetails with a deteriorating macro backdrop that could, over time, justify a more accommodative bias. In response, we expect forward guidance to emphasize a data-dependent, meeting-by-meeting approach, with markets likely to place greater weight on updates to the ECB’s staff projections. These may highlight a more pronounced two-sided risk profile, with risks skewed toward higher inflation and weaker growth. Absent a discernible shift toward the inflation side, the event is unlikely to offer meaningful support to the euro.

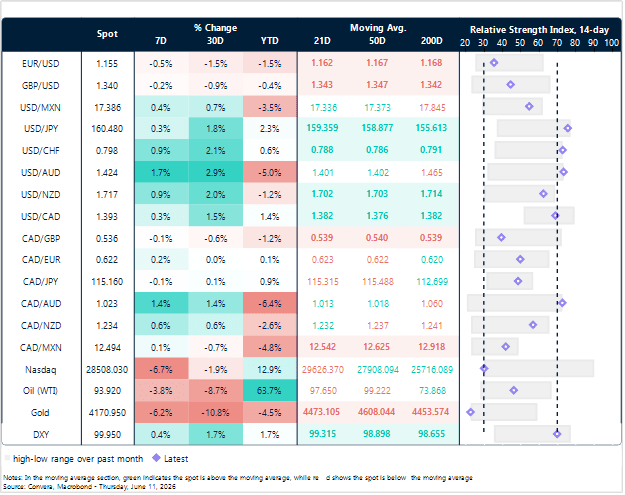

Market snapshot

Table: Currency trends, trading ranges & technical indicators

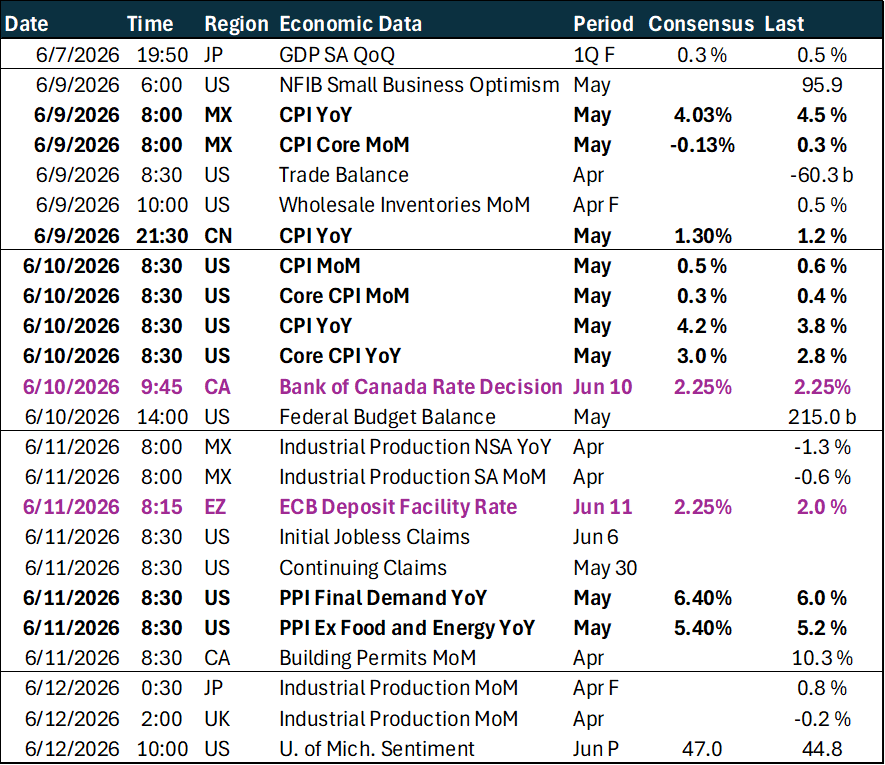

Key global risk events

Calendar: June 08 – 12

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.