Three major events dominate the week ahead, but they all revolve around a single question: how much of the recent oil shock will ultimately feed into inflation and alter the policy outlook?

Last week’s stronger-than-expected US employment report reinforced the view that Fed can afford to keep its focus squarely on inflation. With labor market concerns fading into the background, investors are increasingly debating whether higher energy prices could eventually force another rate hike later this year.

Against that backdrop, Wednesday’s US CPI report stands as the week’s most important event, carrying the greatest potential to move Treasury yields, currencies and global equities. The ECB meeting follows closely behind, though the focus is likely to be on updated forecasts rather than the widely anticipated rate increase. Meanwhile, the Bank of Canada faces a very different challenge as policymakers balance recessionary conditions at home against what they continue to view as a temporary, oil-driven rise in inflation.

The US inflation report is likely to set the tone for global markets. Following three consecutive months of solid payroll growth, the labor market is no longer providing an argument for easier monetary policy. Instead, the resilience in employment gives Fed officials greater flexibility to focus on inflation developments and the pass-through effects of higher energy prices.

Consensus forecasts point to headline CPI accelerating from 3.8% year-on-year to 4.2% in May, while core CPI is expected to edge up from 2.8% to 2.9%. While a rise in headline inflation is largely anticipated due to energy costs, markets will pay closer attention to the core reading. Any upside surprise in core inflation would likely reinforce expectations that the Fed may need to tighten policy further, pushing Treasury yields and Dollar higher while weighing on equity valuations.

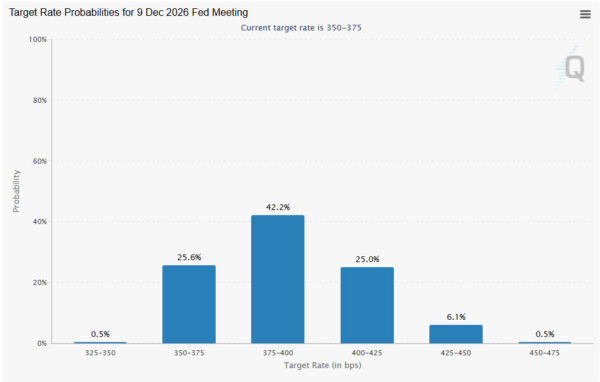

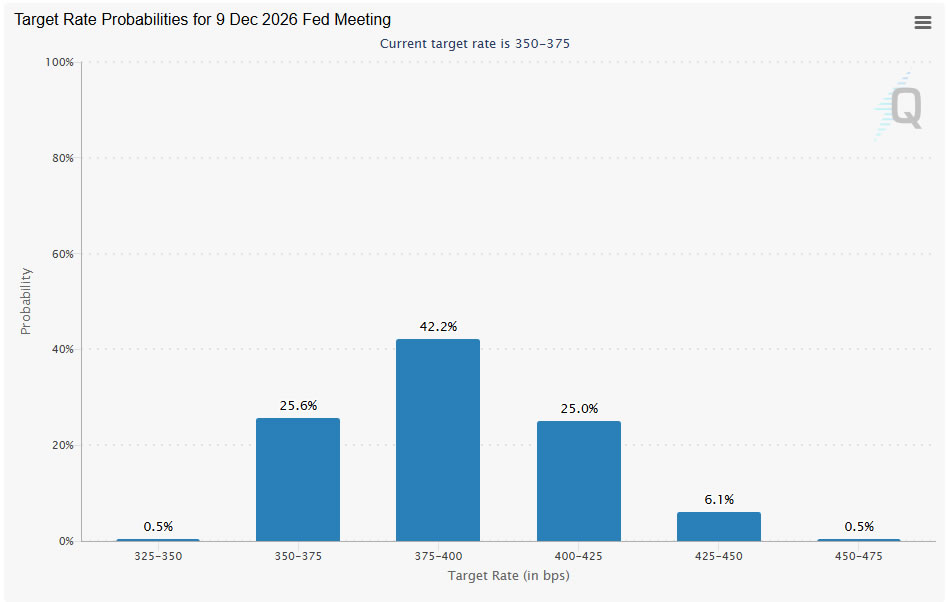

The market reaction function has changed significantly over the past month. Rate cuts are effectively off the table, and Fed funds futures now imply nearly a 75% probability of at least one additional rate increase by year-end. The CPI report will therefore serve as a critical test of whether those expectations are justified.

For the ECB, a 25 basis point increase in the deposit rate to 2.25% is widely expected. Because the decision itself is fully priced, investors will focus instead on President Christine Lagarde’s guidance and, more importantly, the updated staff projections. Recent PMI surveys have painted an increasingly challenging picture for Eurozone growth, raising concerns that the region may be drifting toward recession even as inflation pressures intensify.

Nevertheless, Lagarde is likely to maintain a balanced tone, acknowledging upside inflation risks while emphasizing growing concerns about economic activity. Markets should not expect strong forward guidance. Instead, the new projections may provide the clearest policy signal. Upward revisions to near-term inflation forecasts combined with downgrades to 2026 growth projections toward the 0.3% to 0.5% range would reinforce the stagflation narrative currently emerging across Europe.

While a Reuters survey found that more than 60% of economists expect one additional ECB rate increase later this year, likely in September, conviction remains limited. Confirmation of weaker growth prospects could cap Euro gains even if policymakers retain a tightening bias.

The Bank of Canada enters the week from a markedly different position. Canada’s economy has already recorded two consecutive quarters of contraction, meeting the technical definition of recession. As a result, the central bank’s policy framework differs substantially from that of both Fed and ECB.

Recent employment data have provided policymakers with some breathing room. Strong May job growth reduced pressure for immediate policy easing and supports the Bank’s decision to keep rates steady. At the same time, officials have repeatedly indicated a willingness to look through temporary inflation increases driven by energy prices, arguing that domestic economic weakness should absorb part of the shock.

A hold at 2.25% is widely expected. According to Reuters polling, more than 80% of economists expect rates to remain unchanged through the end of the year. The policy statement and press conference are likely to reinforce the view that the Bank remains on hold, though uncomfortably, as it balances recession risks against temporary inflation pressures.

Highlights for the week:

| Date | Currency | Event |

| Tue, June 9 | AUD | Consumer & Business Confidence |

| Wed, June 10 | CNY | China CPI & Trade Balance |

| Wed, June 10 | USD | US Consumer Price Index (CPI) |

| Wed, June 10 | CAD | BoC Rate Decision |

| Thu, June 11 | EUR | ECB Rate Decision |

| Thu, June 11 | USD | US Producer Price Index (PPI) |

| Fri, June 12 | GBP | UK GDP |

| Fri, June 12 | USD | U. of Michigan Consumer Sentiment (Prelim) |