US and global markets reversed early-year declines in the second quarter of 2026, despite ongoing tensions in the Middle East. A stunning rise in oil prices at the onset of the Iran war gave way to extended declines in the price of Brent crude oil and a rebound in most global stock markets.

Even bonds fared well, with every major fixed-income sector rising in the second quarter and just one falling over the past year. Yields remain attractive, too.

Elsewhere, semiliquid funds continue to gobble up assets despite opaque fee structures. Momentum roared back. Rate hikes are expected. And in case you missed it, Space Exploration Technologies SPCX, better known as SpaceX, made its public market debut on June 12.

Much more happened in the second quarter of 2026 than can be covered here, though. The quarterly Morningstar Markets Observer dives deeper into each of these headlines and unpacks several other important market trends.

Stocks Rebound

Oil rose and global stocks tumbled when the Iran war began on Feb. 28, resulting in an ugly March across most asset classes and regions. While efforts to end the fighting have foundered, the on-again-off-again ceasefire appears to have calmed equity markets and reversed oil’s price spike.

US President Donald Trump, however, declared that the ceasefire was dead and renewed strikes on Iran, increasing uncertainty and jeopardizing Brent crude’s two-month decline.

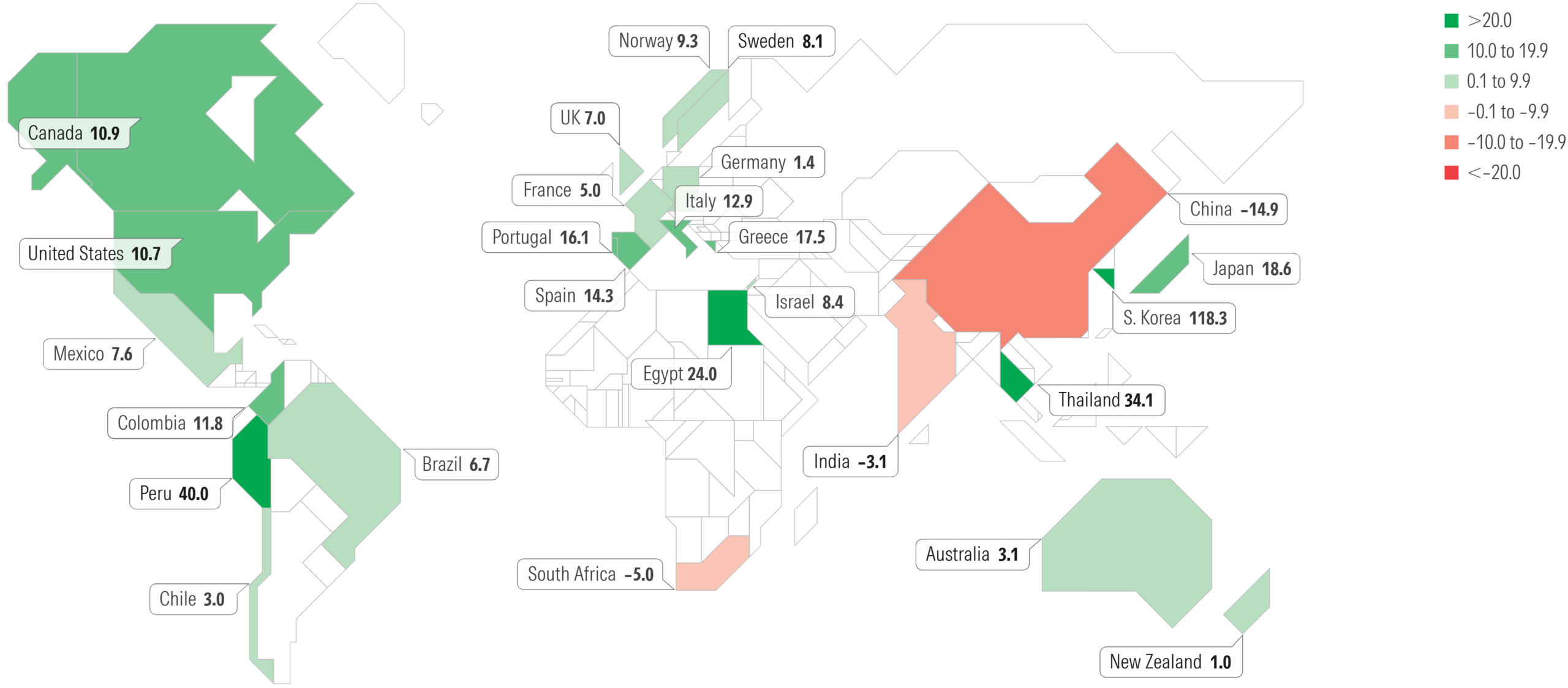

The second quarter’s rebound flipped several major markets from red to green and overall brought the Morningstar Global Markets ex US Index almost 13% higher for the year, after its 10% March decline. Every major European stock market is now positive for the year, with six—Sweden, Germany, Italy, Greece, France, Spain—bouncing back from modest declines in the first quarter.

South Korea continues to be one of the most interesting stock markets to watch. Artificial intelligence infrastructure and semiconductor companies Samsung Electronics 005930 and SK Hynix’s rapid ascent means the two stocks now make up more than half of the Morningstar Korea Index, powering that index to a 118% gain over the first six months of this year. SK Hynix SKHY capitalized on its recent form by becoming the biggest US IPO for a foreign company, giving US investors the chance to invest directly in its shares—though upside may be limited given its recent spike.

Bonds Stay Resilient

Stocks weren’t the only game in town in the second quarter of 2026. Amid geopolitical uncertainty and inflationary worries throughout the quarter, most fixed-income sectors eked out positive gains. Credit-sensitive sectors such as emerging-market debt, municipal bonds, and high-yield credit outperformed high-quality and long-duration bonds, like US Treasuries and agency mortgage-backed securities. Strong corporate fundamentals and a healthy economy continued to provide tailwinds for credit-focused strategies as spreads tightened further during the quarter.

Bond prices move inversely to yields. And despite broad gains across fixed-income sectors, yields still appear attractive relative to recent history, making the asset class an attractive place for income-seeking investors.

Yield changes across fixed-income sectors were a mixed bag in the second quarter. Investors’ risk appetite was relatively strong, which drove yield levels in riskier sectors, like high-yield bonds and emerging-market sovereign debt, lower during the quarter. However, heightened inflation readings and increased expectations of rate hikes in 2026 caused Treasury yields and other rate-sensitive parts of the market, like US core bonds and mortgage-backed securities, to rise. Still, yields are above 10-year median levels across sectors.

Looking ahead, there’s a chance rates will remain relatively high and yields attractive. The market now expects two federal-funds rate hikes (0.5 points total) in 2026. In parallel, the European Central Bank and the Bank of Japan are expected to continue their rate hike campaigns. The oil price shock is only one contributor among several fueling expectations of rate hikes. Hence, oil prices easing off their April/May highs hasn’t much altered expectations for key policy interest rates.

A softer-than-expected US June inflation reading may reduce the need for hikes, but rate cuts are likely not on the table for 2026.

What to Watch in the Third Quarter

None of this is to say it will be smooth sailing the rest of the year. Headwinds remain across asset classes and economies. China is expecting slower growth. The Bank of Japan is hiking interest rates. And Middle East tensions are far from extinguished.

Markets proved resilient in the second quarter, suggesting investors are likely looking past these short-term headwinds to a healthy, growing economy on the backs of AI-driven productivity gains, a strong labor market, and lower inflation.

No matter what transpires, long-term investors are wise to tune out short-term noise and use market volatility as an opportunity to take inventory of their portfolios and rebalance as necessary. Few short-term events have proved detrimental to the stock market over the long term, even if immediate effects are sometimes grim. The first quarter was down; the second quarter was up. Let’s see what the third quarter brings.

Joe Bullard, Preston Caldwell, Sbidag Demerjian, and Mary Marshall contributed to this article.

Subscribe to the Morningstar Research Insider newsletter to receive this report and other key research pieces directly to your inbox every month.