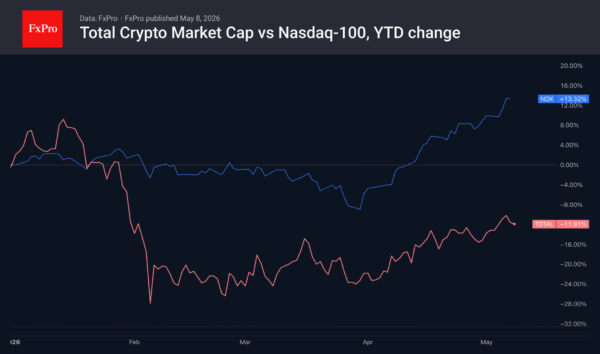

📌 Top story — scroll down for more updates

Micron Recovers as Memory Demand Holds

4:20 pm — MU +15.49% today

That was quite a 24-hour stretch for Micron (MU +15.40%)! Shares tumbled 3% Thursday after Bernstein raised the alarm on the computer memory spot market, then rocketed 9% Friday morning, with Bernstein once again pulling the strings, to end the day up 15.5%. (Leave it to Wall Street…) The worry is that DRAM and NAND prices have gotten so hot that some buyers are being priced out, which could pump the brakes on gains heading into Q2 2026. But here’s the twist. April DRAM prices surged 57% versus Q1 averages, and NAND jumped 65–70%. The buyers who can afford memory are still buying — aggressively — and that’s keeping the bull case very much alive.

- Don’t panic about Q2: Analysts still expect Micron to earn about $19/share in the May quarter on $33.5 billion in revenue, a jaw-dropping 260% sales increase year over year.

- That price target, though: Bernstein’s buy rating hasn’t budged but it’s sitting on a $510 target while Micron trades well above it — an awkward position that suggests a revision is coming, and probably soon. Foolish investors would do well to tune out the noise. After all, Micron is among the highest-scoring companies in both the Hidden Gems primary and Rule Breakers primary Moneyball databases.

Today’s Change

(15.40%) $99.59

Current Price

$746.22

Key Data Points

Market Cap

$729B

Day’s Range

$676.28 – $746.52

52wk Range

$84.68 – $746.52

Volume

2.6M

Avg Vol

42M

Gross Margin

58.54%

Dividend Yield

0.08%

Closing Bell

4:06 pm

The S&P 500 and Nasdaq hit all-time intraday highs Friday after April’s jobs report showed nonfarm payrolls rising 177,000 — that was well above the 130,000 economists expected — while the unemployment rate held at 4.2%. The Nasdaq gained 4.5% over the past 5 days, powered by AI-driven tech earnings. Tempering the mood: a skirmish between U.S. and Iranian forces in the Strait of Hormuz sent oil prices up 1% to around $95 per barrel, though President Trump called the exchange “just a love tap” and Secretary of State Rubio said a ceasefire response from Iran was expected Friday.

- Burry’s dot-com warning: Michael Burry says the market “feels like the last months of the 1999–2000 bubble,” pointing to stocks rising simply because they’ve been rising — on a “two-letter thesis” (AI) everyone thinks they understand.

- Memory stocks on fire: Micron Technology (MU +15.40%) and Sandisk (SNDK +16.60%) each surged about 13% Friday and are up 35% and 27% respectively on the week, as the Philadelphia Semiconductor Index climbs 10%+ and notches 65% gains in 2026.

Toast Drops 15% Despite AI Wins

3:50 pm — TOST -14.21%

By Tim Beyers

Team Rule Breakers

Shares of Toast (TOST 14.74%) are down close to 15% today on what appears to be concern about input costs — particularly hardware costs — as a result of tariffs impacting the supply chain. Macro concerns may also be in place. And yet Toast had a decent quarter. Already, 40,000 locations use the Toast IQ AI chatbot and those using the new Toast IQ Grow agent are seeing a meaningful uptick in order size. I’ll report more after carefully listening to the conference call.

Today’s Change

(-14.74%) $-4.33

Current Price

$25.05

Key Data Points

Market Cap

$17B

Day’s Range

$24.03 – $25.98

52wk Range

$24.03 – $49.66

Volume

1.7M

Avg Vol

11M

Gross Margin

25.84%

HubSpot Drops 20% on Soft Guidance

3:27 pm — HUBS -19.64%

HubSpot (HUBS 19.44%) got absolutely walloped Friday — down 20% — despite actually beating Q1 estimates. Revenue climbed 23% to $881 million, and adjusted EPS of $2.73 cleared the bar handily. What went wrong? Q2 revenue guidance of $897–$898 million landed just shy of the $902 million Wall Street wanted, and that was enough to send investors scrambling for the exits.

- The agentic growing pains are real: HubSpot slashed prices on its Customer Agent and Prospecting Agent products in April, threw in 28-day free trials, and then discovered its own sales team needed retraining on the new usage-based plans. It was a perfect storm for a soft quarter start.

- Bargain or value trap? At just 16.0x this year’s earnings estimates, HUBS looks genuinely cheap. But until software companies prove they can thrive — not just survive — in the agentic AI era, the “SaaS-pocalypse” discount is likely here to stay.

| Metric (GAAP unless noted) | Q1 2026 | Q1 2025 | Y/Y Change |

|---|---|---|---|

| EPS (Non-GAAP) | $2.72 | $1.78 | +52.8% |

| Revenue (millions) | $881.0 | $714.1 | +23.4% |

| Operating Margin (Non-GAAP) | 17.8% | 14.0% | +3.8 pp |

| Free Cash Flow (Non-GAAP, millions) | $153.7 | $122.3 | +25.6% |

| Customers (Non-GAAP) | 299,458 | 258,147 | +16.0% |

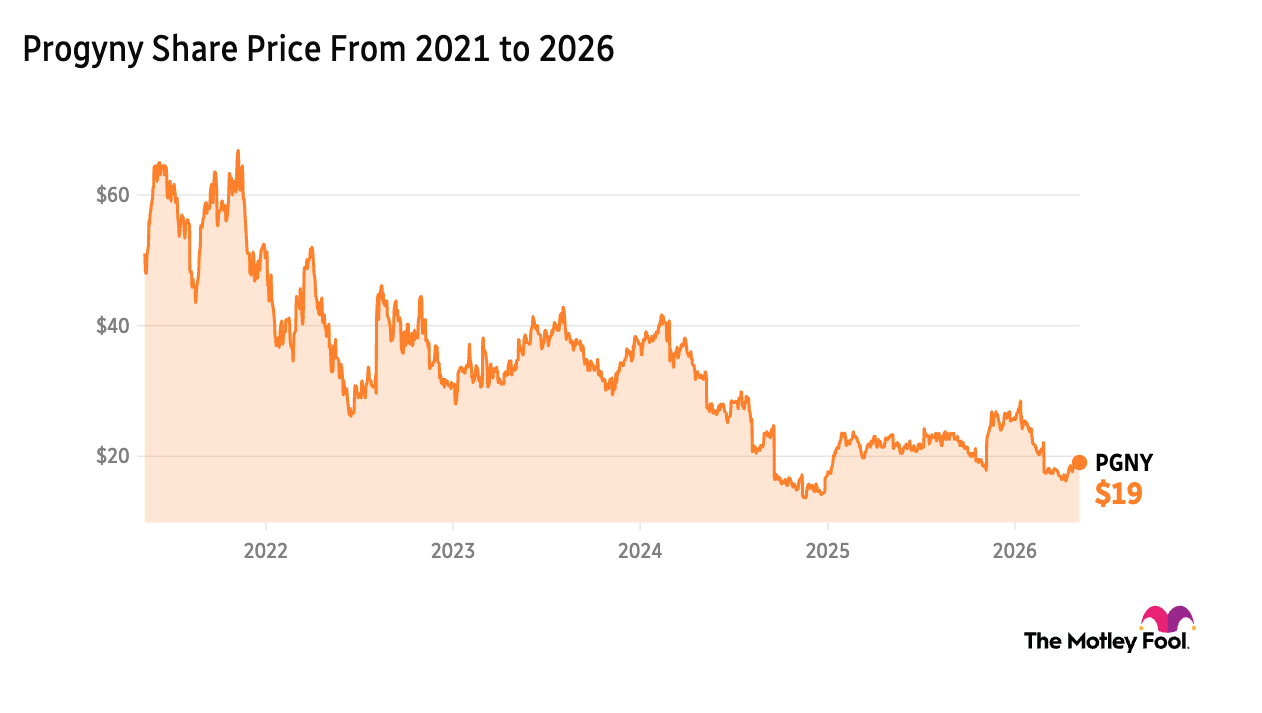

Baby Boom Fuels Progyny’s Rally

2:46 pm — PGNY +20.41%

By Alicia Alfiere

Team Rule Breakers

Progyny’s (PGNY +23.80%) stock is up today, partly because of the conservative guidance issued during its fourth-quarter earnings call. Back in March, Progyny projected that benefit usage could slip to the lower end of its historical range. That conservative guidance likely caused Progyny’s share price to decline after its fourth-quarter results were released.

The company reported first-quarter earnings and, instead of historically low benefit utilization, said member engagement came in at the higher end of expectations.

Nelnet’s Growth Continues

2:26 pm — NNI -15.07%

By Buck Hartzell

All divisions of Nelnet (NNI 13.43%) grew YoY. The biggest driver of growth is their acquisition of Klarna’s (KLAR 1.50%) BNPL loans. That balance reached $766.2 million at quarter end. Their provision for loan losses was $48.5 million vs $13.0 million in Q1 2025. This was entirely due to portfolio growth. Their bank saw net loan and interest income grow 43.5% YoY to $17.8 million. Loan Servicing grew revenues 5.8% to $128.8 million. Education Technology and Payments grew revenues 4.8% YoY to $154.4 million. Nelnet still has two very large assets in ALLO Communications and Hudl that I believe are undervalued on their balance sheet. The stock is still a buy.

Today’s Change

(-13.43%) $-18.98

Current Price

$122.38

Key Data Points

Market Cap

$5.1B

Day’s Range

$116.62 – $132.22

52wk Range

$107.45 – $144.38

Volume

305K

Avg Vol

135K

Gross Margin

88.52%

Dividend Yield

0.88%

Amazon Data Center Overheats

1:10 pm — AMZN +0.8%

Amazon (AMZN +0.56%) Web Services is battling a “thermal issue” at a Northern Virginia data center that has crippled major trading and betting platforms. Starting Thursday night, the overheating in a primary US-East-1 availability zone triggered server impairments for Coinbase Global (COIN +4.30%) and Flutter Entertainment‘s (FLUT 0.01%) FanDuel. While Coinbase reported core services are resolving, FanDuel users faced extended lockouts, preventing crucial mid-game bet cash-outs. AWS, which controls a third of the cloud market, expects a full recovery to take several hours as technicians bring supplemental cooling capacity online to rescue the affected hardware.

- The Cost of Centralization: This single-zone failure highlights the systemic risk for fintech firms reliant on AWS, as even localized hardware heat can disconnect millions from global markets.

- Infrastructure Fragility: The reliance on EC2 virtual servers means that until the physical Virginia facility cools down, digital platforms remain vulnerable to intermittent “instance impairments.”

Today’s Lunchtime News

1:05 pm — PGNY +17.5%

Progyny (PGNY +23.80%) posted higher first-quarter revenue and profit while expanding its client base and completing a $200 million share repurchase program, signaling continued momentum despite the loss of a previously disclosed large client. Revenue rose 1.4% year over year to $328.5 million, or 12.2% excluding the lapsed contract.

- Operational highlights: Net income jumped to $24.2 million, or $0.29 per diluted share, from $15.1 million a year earlier, while gross margin expanded to 25.3% from 23.4% on operational efficiencies and lower stock-based comp. Fertility benefit services revenue rose 1.5% to $209.4 million, and the company served 595 fertility and family building clients, up from 532 a year earlier.

- Capital return push: Progyny repurchased more than 5.5 million shares for $116.4 million during the quarter, completing its $200 million authorization. The board is currently evaluating a new repurchase plan. CEO Pete Anevski said the early selling season is pacing ahead of last year, with new pipeline build “substantially favorable” versus a year ago.

Today’s Change

(23.80%) $4.56

Current Price

$23.72

Key Data Points

Market Cap

$1.5B

Day’s Range

$21.19 – $23.76

52wk Range

$16.10 – $28.75

Volume

4.4M

Avg Vol

1.5M

Gross Margin

23.63%

MercadoLibre’s Revenue Surges 49%

12:20 pm

By Buck Hartzell

MercadoLibre‘s (MELI 12.69%) margins shrank as they invested in future growth. Credit expansion, improved logistics, first party sales, cross border trade and free shipping are all working well.

- Revenue + 49% YoY (46% FXN) to $8.8 B USD (fastest growth since Q2 2022)

- Income from ops -19.9% to $611 M (6.9% margin vs 12.9% in Q1 25)

- Net income -15.5% to $417 M (4.7% margin vs 8.3% in Q1 25)

- TPV + 50% YoY (55% FXN) to $87.2 B

- Credit portfolio + 87% YoY to $14.6 B

Issued 2.7 M credit cards in Q1 26. Credit growth requires reserving, which hurts near term margins. The stock remains attractive for patient capital.

Today’s Change

(-12.69%) $-237.31

Current Price

$1632.70

Key Data Points

Market Cap

$95B

Day’s Range

$1623.00 – $1702.49

52wk Range

$1593.21 – $2645.22

Volume

149K

Avg Vol

517K

Gross Margin

44.50%

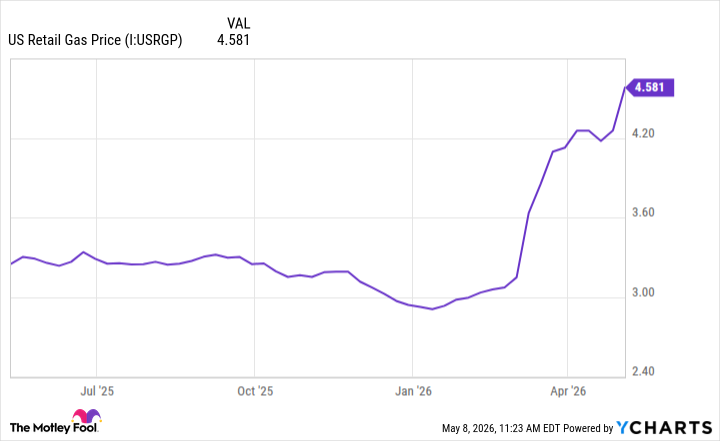

Gas Prices Sink Sentiment to New Low

11:25 am

Consumer sentiment plummeted to a preliminary reading of 48.2 in May, marking a fresh record low as the Iran war continues to drive energy costs higher. Despite a strong labor report, the University of Michigan survey revealed that one-third of respondents blame surging gas prices — now averaging $4.54 nationally — for their deteriorating outlook. While retail giants like Walmart (WMT +0.34%) and Amazon (AMZN +0.56%) have remained resilient, the 9% drop in current conditions suggests major purchases are being shelved. Sentiment is unlikely to recover until supply disruptions resolve, though stock indexes stayed positive as long-term inflation expectations eased slightly to 3.4%.

- The Double-Whammy Effect: Beyond the pump, another third of consumers cited aggressive tariffs as a primary headwind, creating a challenging environment for import-heavy companies like Target (TGT 0.60%).

- Inflationary Silver Lining: While current attitudes are grim, the one-year inflation projection dipped to 4.5%, offering the Federal Reserve a slim hope that price expectations are not becoming permanently unanchored.

The High Cost of Scaling AI

10:25 am

The AI infrastructure race is becoming a high-stakes cash-flow test for Alphabet (GOOG +0.44%), Microsoft (MSFT 1.33%), Amazon (AMZN +0.56%), and Meta Platforms (META 1.18%). Capital expenditures for data centers and chips are consuming an increasingly large share of operating cash, with Amazon spending nearly everything it generates on build-outs. Alphabet is the most striking example of this tension; its forward price-to-free-cash-flow multiple has soared above 200x. While these “hyperscalers” can afford the massive investment, the market is closely watching for when this capital-intensive “backbone” starts yielding clear bottom-line payoffs as free cash flow gets squeezed.

- The 100% Threshold: If capex exceeds operating cash, these giants must look beyond daily profits to fund growth, a pivot that historically triggers investor anxiety.

- Valuation Disconnect: Alphabet’s surging multiple suggests investors are pricing in future AI dominance while simultaneously ignoring the shrinking pile of cash that survives the build-out.

Opening Bell

9:35 am

Markets are climbing this Friday as a robust jobs report and resilient tech earnings override geopolitical friction. Nonfarm payrolls added 115,000 positions in April, shattering the 55,000 estimate, while the unemployment rate held steady at 4.3%. Chipmakers are providing the muscle, with Qualcomm (QCOM +8.17%) up 6% and Micron Technology (MU +15.40%) rising 4%. Despite a brief exchange of fire in the Strait of Hormuz, which President Trump characterized as a “love tap,” markets remain optimistic. Investors are closely watching for Iran’s formal response to a peace proposal as the S&P 500 continues to flirt with all-time highs.

- Broad-Based Earnings Power: Analysts expect 20% year-over-year earnings growth to persist through 2026, suggesting the current market momentum has significant fundamental support beyond just a few tech giants.

- Energy Market Tension: Crude prices hover near $95 as the U.S. Navy destroyers intercepted attacks, though the continued ceasefire suggests traders are pricing in a diplomatic resolution rather than a full-scale oil supply shock.

Trade Desk’s Real Risk Is the Publicis Standoff

9:15 am — TTD -13.11% in pre-market trading

By Sanmeet Deo

Team Rule Breakers

It seems the most pressing concern coming out of The Trade Desk‘s (TTD 2.15%) Q1 2026 earnings is not the macro nor the EPS miss but whether the Publicis situation represents an isolated negotiating dispute or the beginning of a broader agency pushback against TTD’s pricing and transparency practices.

Omnicom’s subsequent audit found no issues, which suggests the Publicis allegations may be overstated. But the market does not trade on what Omnicom found. It trades on uncertainty, and the uncertainty here is significant. Publicis manages enormous ad budgets for global brands. If their advisory against TTD sticks with even a portion of their clients, the revenue impact in Q2 and Q3 could be material, and TTD’s guidance would be giving no credit to that risk.

The secondary concern is margin trajectory. A full-year target of at least 40% adjusted EBITDA margin requires a dramatic improvement from the 30% reported in Q1. That ramp requires either a meaningful revenue acceleration in the back half of the year or aggressive cost containment. The call gave investors no clear picture of which lever management is pulling.

The bull case remains intact in the long-term, the open Internet thesis, retail media, AI search, objectivity as competitive advantage. Jeff Green’s $150 million personal stock purchase is not nothing. But the near-term is genuinely cloudy, and the call did more to validate investor anxiety than to resolve it.

Today’s Change

(-2.15%) $-0.51

Current Price

$22.98

Key Data Points

Market Cap

$11B

Day’s Range

$20.75 – $22.98

52wk Range

$19.74 – $91.45

Volume

2.1M

Avg Vol

20M

Gross Margin

78.63%

U.S. Hiring Surges Past Expectations

9:15 am

The U.S. labor market demonstrated surprising resilience in April, adding 115,000 jobs–nearly doubling economist forecasts of 65,000. While the tech-heavy information sector continues to contract, essential services like healthcare and logistics are propping up the S&P 500. Wage growth moderated to a 3.6% annual clip, providing a “Goldilocks” scenario for the Federal Reserve: strong enough to prevent a recession, but cool enough to avoid an inflationary spiral. This stability likely cements a “higher-for-longer” interest rate path, favoring companies with robust cash flows over speculative growth names.

Lime’s IPO Filing Signals Thaw in IPO Market

8:00am

Micromobility pioneer Lime, officially incorporated as Neutron Holdings, has filed for an initial public offering to list on the Nasdaq under the ticker symbol “LIME.” The start-up arrives at the public gates with significant institutional backing, most notably from Uber Technologies (UBER 1.67%), and a narrative centered on robust revenue expansion and a surging global user base. While the filing remains “placeholder” in nature–omitting specific pricing terms and valuation targets–the heavy-hitting underwriting team led by Goldman Sachs (GS +1.15%) and JPMorgan Chase (JPM 1.36%) suggests a high-conviction push to capitalize on the recent thaw in the IPO market.

- Strategic Ecosystem Value: As a key partner in the Uber app ecosystem, Lime’s public performance will be a critical litmus test for the long-term viability of the rental scooter and e-bike business model.

- Wall Street Heavyweights: The inclusion of top-tier bookrunners like Jefferies (JEF +2.95%) and Evercore (EVR +2.99%) indicates that institutional appetite for late-stage venture success stories is returning to the transportation sector.

This Morning’s Breakfast News

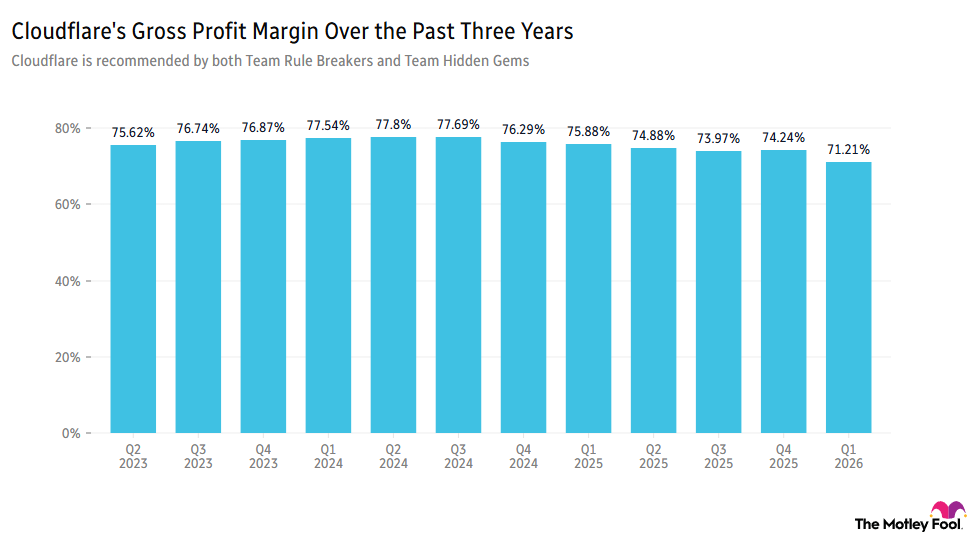

7:30 am — NET -17.75% in pre-market trading

Cloudflare (NET 23.53%) fell over 18% ahead of the opening bell as investors see the company belatedly playing catch-up on AI, with management noting it’s “the biggest tailwind we’ve ever seen,” along with quarterly results showing a 4.67% fall in gross profit margins from the prior-year period.

- “Cloudflare’s usage of AI has increased by more than 600% in the last three months alone”: 1,100 staff are being cut, with an email sent to staff saying management “have to be intentional in how we architect our company for the agentic AI era,” with the job cuts representing 20% of the current workforce.

- News overshadows strong set of results: Despite the fall in gross margin, revenue rose by 34% versus the same period last year, with the outlook for full-year fiscal 2026 revenue and earnings raised.

ICYMI: Thursday’s Scoreboard

6:30 am — COST unchanged in pre-market trading

Costco (COST 0.33%) was the subject of the latest Scoreboard video.

Rocket Lab’s Best Quarter Is the Drama-Free One

6:00 am — RKLB +6.83% in pre-market trading

By Lou Whiteman

Team Hidden Gems

Rocket Lab (RKLB +34.08%) beat expectations for the quarter, but the real story of the earnings report was how little drama there was about the quarter.

The company generated $200 million in revenue in the quarter and posted a $12 million EBITDA loss, better than Wall Street’s $190 million and a loss of $26 million expectation. But note that the company had guided for $185 million to $200 million in revenue, and the EBITDA beat was largely because of accounting: Rocket Lab benefited from a reversal of some 2025 bonus compensation accruals.

Rocket Lab needs to be viewed as a long-term growth story, not a quarter-to-quarter standout. And the company’s forecast for the future, though not surprising, was encouraging. The company grew its backlog by 20% since last quarter thanks to strong bookings in its launch business.

Today’s Change

(34.08%) $26.78

Current Price

$105.36

Key Data Points

Market Cap

$45B

Day’s Range

$85.87 – $105.38

52wk Range

$20.23 – $105.38

Volume

3.3M

Avg Vol

21M

Gross Margin

31.66%

TSMC’s AI Demand Drives April Revenue Higher

5:15 am — TSM +0.63% in pre-market trading

TSMC (TSM 0.84%) reported a robust 17.5% year-over-year revenue increase for April, totaling NT$410.73 billion ($13.08 billion), as the global appetite for advanced AI hardware remains insatiable. While monthly sales dipped a marginal 1.1% from March, the year-to-date trajectory is formidable, with revenue up nearly 30% through the first four months of 2026. The world’s leading foundry is successfully navigating a complex macro environment, leveraging its dominance in 3nm and 5nm nodes to support “Magnificent Seven” clients like Nvidia (NVDA +1.73%) and Apple (AAPL +2.08%). Management’s bullish Q2 guidance of up to $40.2 billion suggests that the bottleneck for growth remains production capacity rather than a lack of orders.

- Aggressive Capex Expansion: To meet “extremely strong” demand, the company has raised its 2026 capital expenditure target to a range of $52 billion to $56 billion, focusing on advanced packaging and new global fabs.

- Geopolitical Balancing Act: Despite tightening U.S. technology restrictions on high-end silicon, TSMC’s record-high margins of 66.2% prove its specialized manufacturing moat currently outweighs the risk of regional trade friction.

Taiwan Semiconductor Manufacturing

Today’s Change

(-0.84%) $-3.48

Current Price

$410.67

Key Data Points

Market Cap

$2.1T

Day’s Range

$400.98 – $417.01

52wk Range

$176.47 – $420.00

Volume

889K

Avg Vol

13M

Gross Margin

61.02%

Dividend Yield

0.81%

Top of the Morning

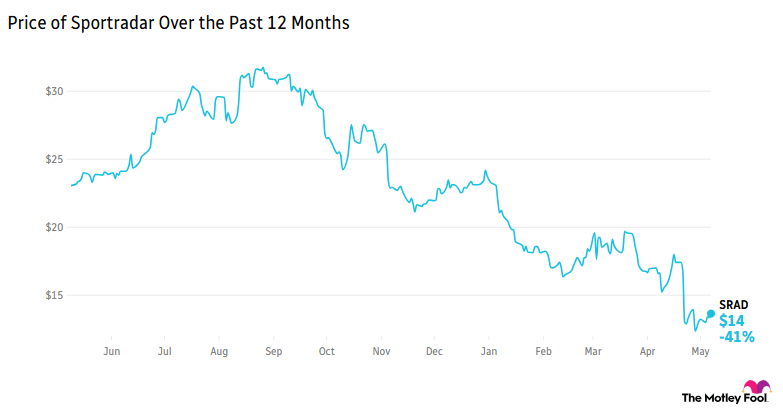

5:00 am — SRAD +0.88% in pre-market trading

By Morning Show host Jim Mueller, CFA

Team Rule Breakers

What should you do if you’re the CEO of a company when a short attack article comes out about your company?

If you’re smart, very little. At most, comment on any errors of fact, answer analyst questions, and then shut up.

That’s what Carsten Koerl, CEO of Sportradar (SRAD 4.40%), has done.

A bit over two weeks ago, Muddy Waters and Calisto Research put out nearly identical short reports on the company claiming, among other things, that the company should be unprofitable because it was purposefully doing business with criminal enterprises. Evidence given was an interaction with a sales rep and finding evidence of Sportradar’s code on various illegal gambling websites.

Shares fell over 20% that day. Good for Muddy Waters, I guess.

In reply, the company moved up its earnings release and did nothing else until the new release date. Then, on the day of earnings, they filed with the SEC a document explaining that there were three ways for their code to be found on various sites, only one of which was legitimate. Further, the way Muddy Waters detected the code couldn’t distinguish among the three.

During the conference call Koerl also answered questions posed by analysts about various points raised by Muddy Waters. For example, he said that the sales rep was quite young (as in inexperienced) and that talk is talk until due diligence has been performed. He strongly implied that such due diligence would have not led anywhere if the Muddy Waters reps were legitimate instead of trying to entrap the rep.

He answered a few other questions, but then he did a smart thing. He shut up.

4:30 am — ABNB -0.98% in pre-market trading

By Morning Show host Alicia Alfiere

Team Rule Breakers

Airbnb (ABNB +0.73%) reported that gross booking value, which is the value of bookings on the booking platform, grew 19% to total $2.9 billion in the first quarter. That’s impressive, but what’s more fascinating is that the company’s new “Reserve Now, Pay Later” bookings drove roughly 20% of global gross booking value. This new feature has changed how guests can book and Airbnb reports that the increased flexibility has caused long lead times and travelers booking pricier accommodations.

And there were other signs of a platform that continues to grow-like an increase in first time bookers. The growth in these new-to-Airbnb travelers grew 10% in the first quarter-which is the highest rate seen since early 2022. Additionally, this new Airbnb-er expansion is driven by younger customers and travelers who live in Airbnb’s expansion markets, like Brazil, Japan, and India.

Today’s Change

(0.73%) $1.03

Current Price

$141.49

Key Data Points

Market Cap

$84B

Day’s Range

$137.25 – $146.97

52wk Range

$110.81 – $147.25

Volume

7.7M

Avg Vol

4.3M

Gross Margin

72.27%

Before the Opening Bell

4:45 am

U.S. stock futures advanced early Friday as optimism over a potential diplomatic resolution to the U.S.-Iran conflict outweighed Thursday’s slight retreat from record highs. Despite the Dow’s 314-point slide yesterday, all three major benchmarks remain on track for a winning week, buoyed by a resilient tech earnings season. The Nasdaq Composite leads the charge with a projected 2.8% weekly gain, while the S&P 500 and Dow Jones Industrial Averagehave risen 1.5% and 0.2%, respectively. All eyes now pivot to the April nonfarm payrolls report, which will serve as a critical health check for the economy amid shifting geopolitical undercurrents.