Netflix NFLX is the world’s largest subscription streaming platform, while Apple AAPL is the consumer-technology powerhouse whose Apple TV service sits inside a sprawling, high-margin Services franchise. Both compete fiercely for global viewers’ attention and entertainment spending.

The comparison is timely. Both reported results in April 2026 and used spring 2026 events to unveil ambitious 2026 content slates and clarify their advertising strategies, leaving investors to weigh which stock offers stronger risk-adjusted upside today.

Let’s delve deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

The Case for NFLX Stock

Netflix enters mid-2026 as the clear scale leader in subscription streaming, and management’s guidance reflects that confidence. The company reiterated full-year 2026 revenues of $50.7-$51.7 billion, representing 12-14% growth, alongside a targeted 31.5% operating margin. It also raised its full-year free cash flow guidance to $12.5 billion from a prior $11 billion.

Monetization is the central catalyst. Advertising revenue is on track to roughly double to about $3 billion in 2026, and the ad-supported plan represented over 60% of Q1 sign-ups in ad-enabled markets. Netflix’s advertiser base has expanded to more than 4,000 clients, up 70% year over year. The second-half 2026 content slate is also dense, featuring Denzel Washington’s Here Comes the Flood, Greta Gerwig’s Narnia, David Fincher’s follow-up to Once Upon a Time in Hollywood, Will Ferrell’s The Hawk, One Hundred Years of Solitude season two, and Lupin Part 4, plus the heavyweight Tyson Fury-Anthony Joshua fight as a marquee live event.

Still, the picture is balanced rather than uniformly bullish. Netflix flagged that content amortization growth peaks in 2026 before decelerating to mid-to-high single-digit rates in the second half, meaning near-term programming costs run high and weigh on quarterly margins. The streaming market also remains intensely competitive, engagement growth is hard to sustain at the company’s scale, and continued revenue gains lean partly on further price increases that could test subscriber tolerance over time. Newer bets such as video podcasts, cloud gaming and generative-AI creator tools add useful optionality but remain unproven revenue contributors for now. On balance, Netflix offers a credible growth runway, yet its current forward setup carries both visible catalysts and real, near-term execution risks.

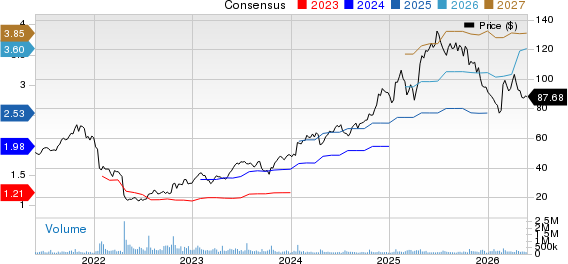

The Zacks Consensus Estimate for 2026 earnings is pegged at $3.60 per share, up 2% over the past 30 days. This indicates a 42.29% increase from the previous year.

Netflix, Inc. Price and Consensus

Netflix, Inc. price-consensus-chart | Netflix, Inc. Quote

The Case for AAPL Stock

Apple’s investment appeal rests on a simple structural advantage: Apple TV is one component of a vast, high-margin Services franchise rather than a standalone streaming bet. In fiscal second-quarter 2026, Apple delivered its best March quarter ever, with revenues of $111.2 billion, up 17%, and Services reaching another all-time record at a 49.3% gross margin. Management guided fiscal third-quarter revenues to grow 14-17%, with Services expected to grow at a rate similar to the strong March quarter, a reassuring forward signal.

The content strategy reinforces that strength. Apple TV plans a new original almost every week in 2026, and its second-half slate is deliberately premium, headlined by Ted Lasso‘s fourth season this summer, a new For All Mankind, and theatrical-style films such as Matchbox The Movie and Way of the Warrior Kid, alongside live F1, MLB, and MLS rights. This “fewer, bigger, better” approach is designed to extend viewing windows and temper subscriber churn. Apple has chosen to keep Apple TV ad-free, betting that uninterrupted, quality-first viewing strengthens loyalty and ecosystem engagement across more than one billion screens.

Capital returns add further support. Apple authorized an additional $100 billion buyback and raised its dividend. The upcoming WWDC in June, centered on AI advancements and a more conversational Siri, could lift Services engagement and deepen ecosystem stickiness. Headwinds exist, including rising memory costs, component supply constraints, and tariff exposure, but Apple’s scale, cash generation, and ecosystem give it room to absorb them. The forward setup looks comparatively durable and reassuring.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $8.74 per share, up 2.6% over the past 30 days, suggesting 17.2% year-over-year growth.

Apple Inc. Price and Consensus

Apple Inc. price-consensus-chart | Apple Inc. Quote

Valuation and Price Performance Comparison

On valuation, both stocks trade at a premium. Apple carries a forward price-to-sales (P/S) ratio of 9.02X, while Netflix sits at 6.86X. Although Netflix’s multiple is lower, Apple’s richer valuation appears better justified, supported by a diversified, high-margin Services engine, sturdy cash generation and broad-based, double-digit revenue growth.

NFLX vs. AAPL: P/S F12M Ratio

Image Source: Zacks Investment Research

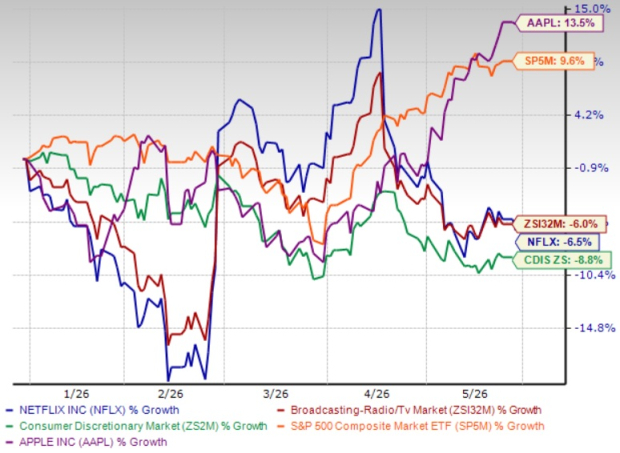

On price performance, Netflix shares have lost 6.5% in the year-to-date period, outperforming both the Zacks Broadcast Radio and Television industry and the broader Consumer Discretionary sector, yet clearly underperforming Apple’s 13.5% return over the same period. Apple thus pairs a premium multiple with stronger momentum and a more defensible earnings base.

NFLX Underperforms AAPL Year-to-date

Image Source: Zacks Investment Research

Conclusion

Weighing both names, Apple emerges with the clearer edge. Its streaming ambitions sit within a diversified, high-margin Services franchise rather than a single revenue stream, its fiscal third-quarter guidance points to durable double-digit growth, and a premium, ad-free 2026 content slate reinforces ecosystem loyalty. Sizable buybacks, a rising dividend, and stronger year-to-date price performance add support, and its premium valuation looks better justified. Netflix offers a credible growth story and expanding advertising, but front-loaded content costs, competition and price-hike reliance temper its setup. Investors should buy Apple for better upside potential, while holding Netflix or awaiting a better entry point. AAPL carries a Zacks Rank #2 (Buy), while NFLX has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI’s Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren’t likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

Apple Inc. (AAPL) : Free Stock Analysis Report

Netflix, Inc. (NFLX) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.