The US jobs report gave stock markets exactly what they wanted — proof the economy is still holding up without reigniting fears of runaway inflation. Stocks liked it, the Fed will likely like it, and recession fears eased further. Yet despite the upbeat reaction, traders still seem unwilling to fully commit because the biggest market risk remains geopolitical, not economic.

Dollar slipped broadly in early US trading after the payrolls release, though the move lacked strong follow-through against most major currencies. That hesitation says a lot about the current market environment. Even after a stronger-than-expected jobs report, investors are still treating developments surrounding the US-Iran conflict as the dominant macro driver.

The April payrolls report itself was clearly solid. Non-Farm Payrolls rose by 115k, almost double market expectations, while March’s already strong reading was revised higher to 185k. The unemployment rate held steady at 4.3%, suggesting the labor market continues showing resilience despite geopolitical uncertainty and slowing global growth concerns.

At the same time, the inflation side of the report stayed relatively calm. Average hourly earnings increased just 0.2% mom, below expectations, even though annual wage growth ticked up modestly to 3.6% yoy. For markets, that combination created the ideal “Goldilocks” outcome: strong enough to reassure investors the economy is not sliding toward recession, but soft enough to avoid reviving fears of a more hawkish Federal Reserve.

That dynamic helped reinforce the powerful risk-on environment that has driven S&P 500 and NASDAQ toward repeated record highs in recent sessions. Investors could believe the Fed can comfortably stay on hold for the rest of the year without needing to either rescue the economy or aggressively tighten policy further. Market pricing now shows more than 70% probability that rates remain unchanged through year-end.

Meanwhile, Canadian Dollar became the major underperformer after Canada’s labor market delivered a sharp negative surprise. Employment fell by -17.7k in April instead of posting expected gains, while unemployment rose to 6.9%. The report reinforced concerns that Canada’s economy is losing momentum more quickly than the US.

While BoC Governor Tiff Macklem has warned that persistent inflation could eventually require multiple rate hikes, deteriorating employment conditions make it increasingly difficult for the central bank to realistically follow through on that threat.

Still, even the strong US payrolls report failed to fully dominate market attention. Markets are now turning back toward geopolitics as the dominant macro driver. US Secretary of State Marco Rubio said Washington expects a response from Tehran later Friday regarding the proposed agreement aimed at ending the conflict. “We’ll see what the response entails. The hope is it’s something that can put us into a serious process in negotiation,” Rubio said.

For now, the broader market tone remains cautiously constructive. Kiwi leads currency gains for the week, followed by Aussie and Swiss Franc, while Loonie, Dollar, and Yen underperform. But despite the encouraging payrolls report, investors appear unwilling to fully extend risk positioning until there is greater clarity on whether the fragile path toward a US-Iran agreement can hold.

US Payrolls Beat Expectations With 115k Growth, But Wage Growth Stays Calm

US payrolls surprised to the upside in April, reinforcing the view that the labor market remains resilient despite slowing growth concerns. At the same time, softer monthly wage growth helped keep the broader “Goldilocks” soft-landing narrative intact. Read More.

Canada Employment Falls -17.7k as Unemployment Rises to 6.9%

Canada’s labor market weakened in April. Employment unexpectedly fell, full-time jobs dropped heavily, and unemployment climbed to 6.9%, adding to concerns about slowing economic momentum. Read More.

Japan Real Wage Growth Extends Gains Despite Slower Nominal Pay Growth

Japan’s real wages rose for a third consecutive month in March, supported by easing inflation and the strongest stretch of base pay growth in more than three decades. Read More.

Japan PMI Services Finalized at 51.0 as Middle East War Fuels Cost Pressures

Japan’s services sector lost momentum in April just as inflation pressures intensified sharply. Rising energy costs linked to the Middle East conflict pushed input prices to a three-and-a-half-year high and selling prices to their steepest increase in nearly two decades. Read More.

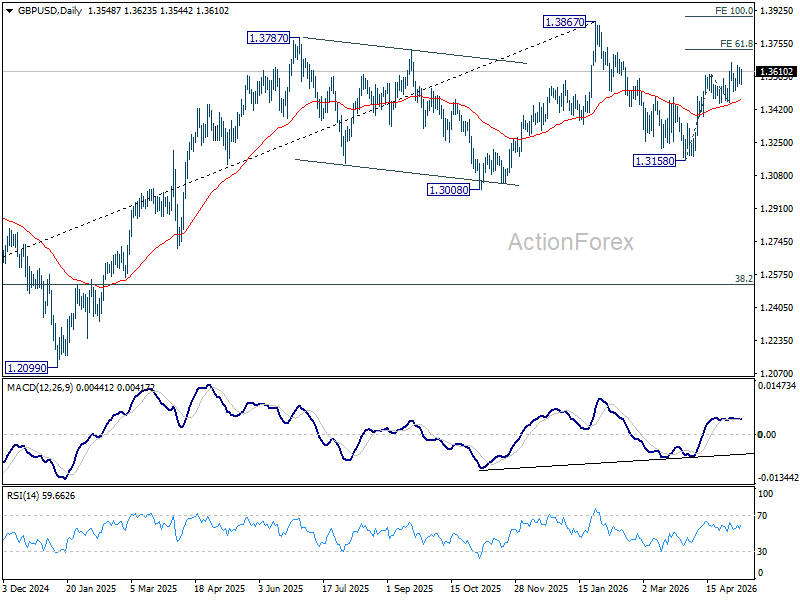

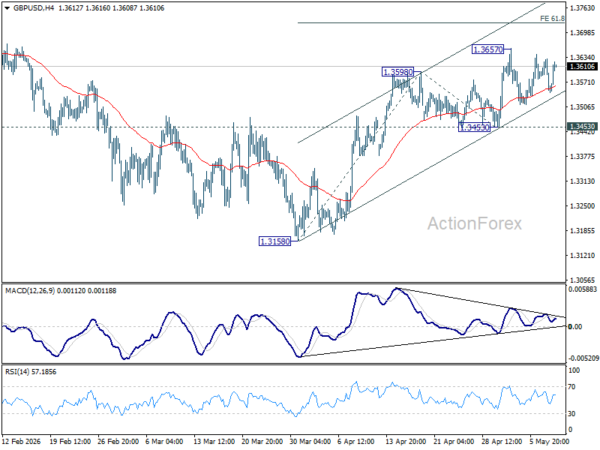

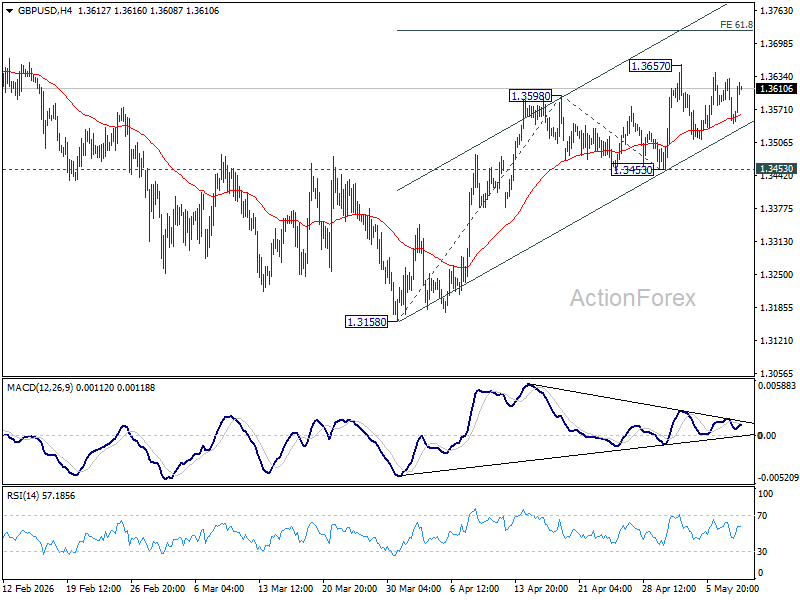

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3522; (P) 1.3577; (R1) 1.3607; More…

GBP/USD rebounded after drawing support from 55 4H EMA, but stays below 1.3657 resistance. Intraday bias remains neutral and more consolidations could still be seen. Further rise is expected with 1.3453 support intact. On the upside, above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).