Key Points

Micron Technology (NASDAQ: MU) has become one of the key players in the artificial intelligence (AI) boom. When we think of AI, our first thought may be the chips powering AI tasks — but these chips must be accompanied by something else, and that’s memory and storage capabilities. This is where Micron comes in, offering a wide range of solutions.

And this has translated into explosive growth for the company. Earnings have reached record levels, and the latest quarterly report reinforced this trend. Micron’s revenue soared in the triple digits to more than $41 billion, and net income jumped in the quadruple digits to $28 billion. Both largely beat analysts’ estimates. The company’s message was positive too: Demand from AI customers is soaring, and we may be in the early stages of this growth opportunity.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a “Double Down” signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same “Total Conviction” signal is flashing for a company 1/100th the size of Nvidia. Continue »

As for Micron stock, investors have recognized the company’s potential and piled in: The shares have skyrocketed in recent times, gaining more than 260% this year alone.

Considering all of this, is Micron a buy after its blowout earnings report? Let’s find out.

Image source: Getty Images.

A memory specialist

First, a bit of background on Micron. The company makes various types of memory and storage, including DRAM, NAND, and HBM. These products, offering memory as a computer or processor works, long-term storage, and fast memory access, cover the various needs of AI projects. Customers, as they run AI workloads, need chips from players like Nvidia, but they also need this memory capacity — and that’s created enormous demand for Micron and others in the field.

In fact, demand is so high that, even with multiple players in the space, from Seagate Technology to SK Hynix, it’s steadily surpassed supply. This means that competition hasn’t been a problem for Micron.

All of this has led to tremendous earnings growth for this memory player, as we’ve seen in recent quarters, and the company confirmed the trend in the latest period. Quarterly revenue reached record levels for the fifth consecutive time. Free cash flow climbed to record levels of $18 billion, and importantly, gross margin came in at more than 84%. Gross margin is particularly key because it shows the company is highly profitable on sales.

16 customer agreements

Micron also signed 16 customer agreements that offer the company and investors visibility on revenue ahead, reinforcing the idea that the demand we’ve seen so far is set to continue. The deals, with data center, consumer, and automotive customers, run through 2030 and involve commitments to purchase a certain volume of memory products. The company expects $22 billion in commitments from the deals signed so far, and it expects half of its revenue to eventually come from such strategic agreements.

This visibility on revenue ahead is positive as it helps guide Micron as it invests in areas such as manufacturing capacity.

“The early innings” of AI

And speaking of the future, the company offered an extremely positive message, saying we’re in “the early innings” of the AI revolution and that the expansion of AI into various industries represents key memory opportunities. For example, humanoid robots carry 10 times the memory of a vehicle with a driver assistance system — this means that, as robotics systems advance, Micron may see a new and lasting wave of growth down the road.

Now let’s return to our question: Considering all of this exciting news, is Micron a buy? Or is it too late to get in on this stock after its enormous gain? Though Micron’s stock has soared, and its valuation has climbed, the valuation level still remains reasonable.

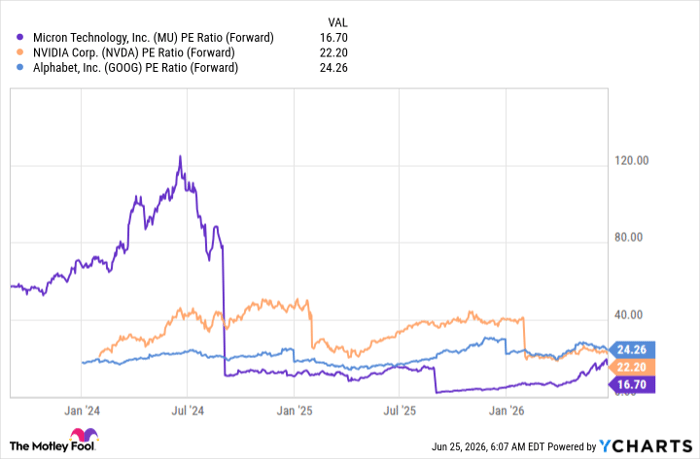

MU PE Ratio (Forward) data by YCharts

Today, Micron trades at 16x forward earnings estimates, which is lower than levels just a year ago — and the stock remains cheaper than other tech giants such as Nvidia and Alphabet, for example.

This price level, along with clues that suggest Micron may benefit from the AI boom for quite some time make now — even after the stock’s big gain — a good time for growth investors to add this stock to their portfolios.

Should you buy stock in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $387,428!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,221,398!*

Now, it’s worth noting Stock Advisor’s total average return is 895% — a market-crushing outperformance compared to 205% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of June 25, 2026.

Adria Cimino has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Micron Technology, and Nvidia. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.