Luckin Coffee stock has delivered a strong 132.3% gain over the past 5 years, yet its current valuation checks still suggest the shares trade on the cheap side rather than looking stretched.

- Over 5 years, a 132.3% return indicates that early investors have already seen substantial value created, so the current price around this level needs to be weighed against what is already embedded in expectations.

- For a business built on scaling a physical retail network, the long term value case can hinge on whether store level economics and cash generation improve steadily. At the same time, any sustained pressure on margins or funding costs may limit how much investors are willing to pay for further expansion.

- Luckin Coffee screens as undervalued on a broad set of metrics, with the company passing 6 of 6 valuation checks. This points to the broader checks leaning cheap rather than suggesting the stock is fully priced.

The issue now is whether Luckin Coffee’s current share price still leaves enough implied upside from those valuation checks to compensate for the risks in the underlying business model.

Find out why Luckin Coffee’s -15.2% return over the last year is lagging behind its peers.

Is Luckin Coffee a Bargain on Earnings?

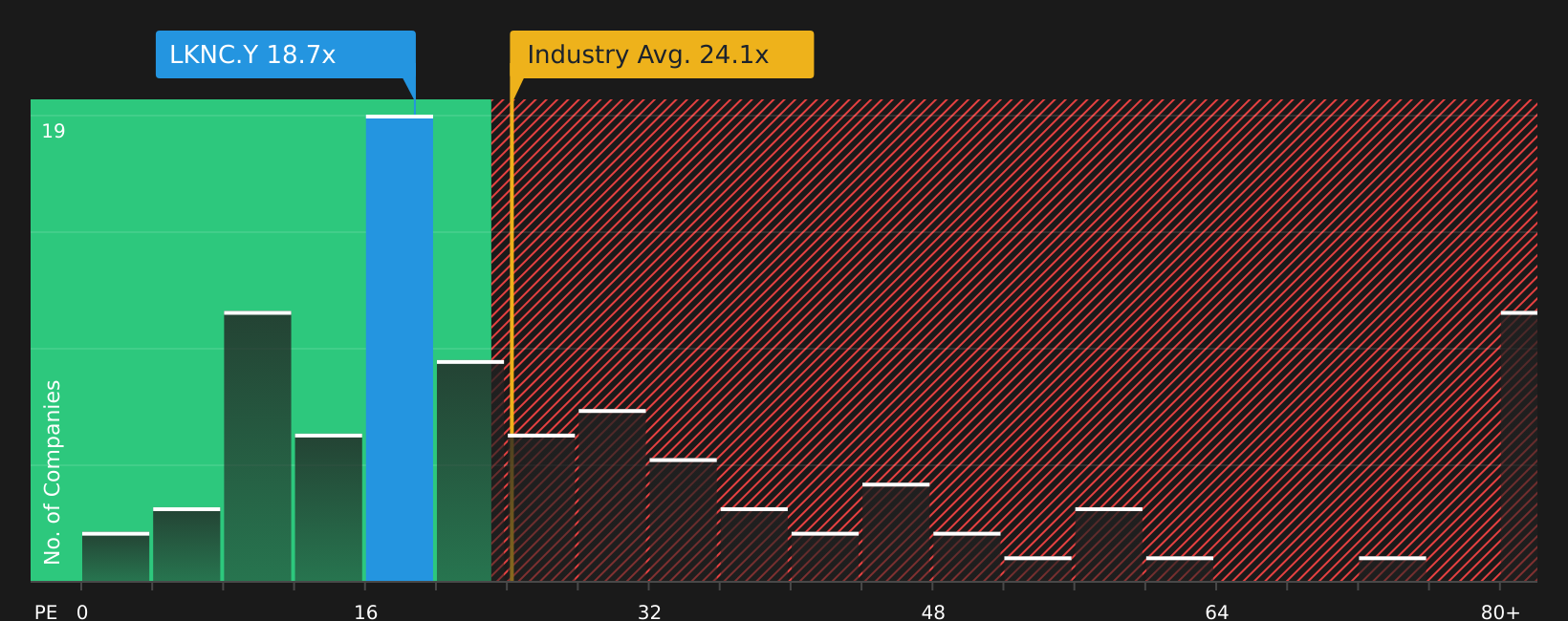

The P/E multiple is a useful way to look at Luckin Coffee because earnings are a central reference point for how the stock is being valued right now. On this basis, Luckin Coffee trades at about 18.7x earnings, which sits below the hospitality industry average of roughly 24.1x and well under the wider peer group average of about 73.8x. That comparison suggests investors are paying less for each unit of current earnings than they are for many comparable stocks in the sector.

A more tailored lens is the modelled fair P/E ratio of around 30.9x, which factors in elements such as the company’s size, profitability profile and sector risks. Compared with this benchmark, the current 18.7x points to a sizeable gap, indicating the market is assigning a lower multiple than the framework suggests might be reasonable for Luckin Coffee on its recent earnings base.

On the P/E yardstick, Luckin Coffee stock currently screens as undervalued relative to both sector norms and its own fair multiple estimate.

See what the numbers say about this price — find out in our valuation breakdown.

The Luckin Coffee Narrative: What Would Justify Today’s Price?

Simply Wall St Narratives for Luckin Coffee pick up where the P/E puzzle leaves off by explaining which combinations of sales growth, profit margins and earnings would need to occur for Luckin Coffee’s stock to be worth meaningfully more or less than today’s price. Each scenario clearly connects its figures to a specific view of how growth, profitability and risks might evolve, giving you a reference point to revisit as new information becomes available.

You can add your voice to the Simply Wall St community by sharing a Narrative on Luckin Coffee that lays out your numbers based view of where its growth, margins and execution could go from here.

Set out your thesis in a structured way, then see how it holds up as new data on Luckin Coffee’s business and valuation becomes available over time.

Do you think there’s more to the story for Luckin Coffee? Head over to our Community to see what others are saying!

The Bottom Line

Luckin Coffee currently screens as undervalued on market multiples, with the P/E sitting well below both sector averages and the tailored fair ratio reference point. The broader valuation checks also lean supportive, which suggests the market is still pricing in a meaningful discount to peers.

What matters from here is whether Luckin Coffee can sustain attractive store level economics and margin quality without leaning too heavily on costly expansion or funding. The key question for investors is whether that apparent discount reflects genuine mispricing or an appropriate cushion for execution and business model risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com