The EV market moderated in June following a stronger May, as both new and used EV sales declined month over month. Despite softer demand, new EV inventory remained well below year-ago levels, reflecting a market that continues to operate with relative discipline. At the same time, used EV sales remained substantially above year-ago levels as off-lease returns and trade-ins increase availability. Together, these trends highlight the growing importance of the used market in improving affordability and broadening EV adoption.

New and Used EV Sales – June

New EV Sales: New EV sales totaled an estimated 74,967 units in June, down 15.2% from May and 27.8% from a year earlier. EVs accounted for 5.4% of total new-vehicle sales, a decline from May’s improving share, as the EV market remained softer than last year.

Tesla remained the volume leader with 40,460 units sold, followed by Rivian, Toyota, Cadillac and Hyundai. Tesla’s share of total EV sales increased to roughly 54%, as its sales decline was less severe than the broader market. Rivian was the only higher-volume EV brand to post a month-over-month sales increase in June, rising 8.3% from May and moving into the No. 2 position.

The June slowdown was broad-based, with most EV brands posting month-over-month declines, including several higher-volume automakers such as Hyundai, Ford and Chevrolet.

Used EV Sales: Used EV sales declined 15.6% month over month in June to 35,253 units but remained 20.3% higher versus 2025. Used EV market share slipped modestly to 2.4%, as a majority of brands saw month-over-month declines. The market was again led by Tesla, with 12,848 units sold through non-Tesla dealers, a slight decline from May. Sales of used Hyundai, BMW, Ford and Chevrolet EVs rounded out the top five.

Despite the monthly pullback, used EV sales remained well above year-ago levels, reflecting continued growth in off-lease returns and trade-ins while highlighting the ongoing expansion of the used EV market, which historically has been mostly Tesla products.

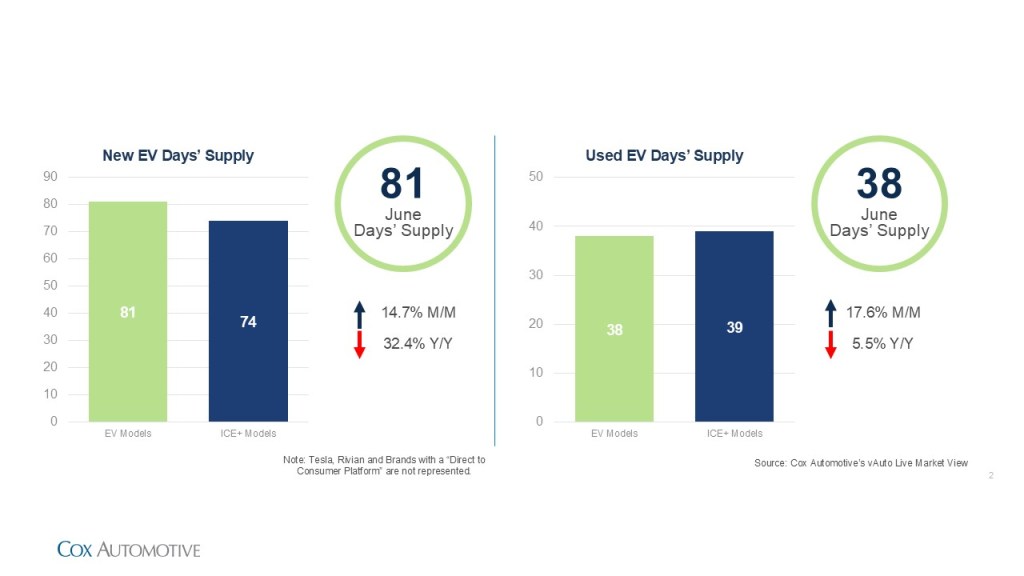

New and Used EV Days’ Supply – June

New EV Days’ Supply: Days’ supply increased to 81 days in June, up 14.7% month over month. Despite the increase, EV inventory remained significantly below year-earlier levels, with days’ supply down 32.4% year over year. EV days’ supply also moved back above ICE+ levels in June, after briefly falling below in May.

Inventory levels remained uneven among manufacturers. Volkswagen, Porsche, Nissan and Chevrolet recorded some of the highest days’ supply levels in the market, while Subaru, Lexus, Hyundai, Mercedes-Benz and Cadillac ranked among the lowest.

Used EV Days’ Supply: Days’ supply rose to 38 days in June, up 17.6% month over month but 5.5% below year-earlier levels. Used EV days’ supply remained below ICE+ for a fourth consecutive month, though the gap narrowed to just one day as ICE+ inventory also tightened.

Availability increased across many high-volume brands, led by Volkswagen, Audi, Nissan, Toyota and Chevrolet. Among major used EV brands, Cadillac, Ford, Mercedes-Benz and BMW carried the highest inventory levels, while Genesis, Rivian, Tesla and Hyundai maintained some of the leanest inventory positions. Despite the month-over-month increase, used EV days’ supply suggests the market is absorbing the growing availability.

Note: Tesla and Rivian figures reflect only vehicles available through traditional dealerships and exclude vehicles at factory-owned outlets.

New and Used EV Prices – June

New EV ATP: The average transaction price (ATP) for a new EV rose to $56,238 in June, up 3.5% month over month, the largest monthly increase since June 2025, but still down 4.5% year over year. Incentives eased to 13% of ATP, or approximately $7,290 per vehicle, down from 14% in May.

Unlike recent months, the increase was not primarily driven by Tesla, as the EV leader’s ATP rose only modestly to $53,107 and remained 2.1% below year-ago levels. Instead, the month-over-month increase reflects a broader mix shift as sales declined sharply among lower-priced, high-volume brands, particularly Hyundai and Chevrolet. The result: Higher-priced EVs accounted for a larger share of the market.

For more details, read the June Kelley Blue Book ATP report.

Used EV Listing Price: The average listing price for a used EV was $38,342 in June, up 3.5% from May and 7% year over year. The increase was broad-based, including several high-volume brands such as Tesla, Chevrolet, Hyundai and Kia. The increase also reflected a modest mix shift, as higher-priced brands such as Cadillac and BMW gained share in the used EV market while lower-priced brands, including Chevrolet, Nissan and Volkswagen, lost share.

Compared with ICE+, the used EV premium widened to $3,382 in June, up from $2,193 in May, as used EV prices continued to increase at a faster pace.

Looking Ahead:

The EV market is expected to remain in a more measured growth phase in the months ahead. While June sales softened, inventory levels remain well below year-ago levels, suggesting supply conditions remain relatively disciplined. Competitive pressure is likely to remain elevated in the new market as automakers balance pricing, incentives and production plans, while expanding used EV availability continues to support broader consumer access and long-term adoption.

The EV Market Monitor gauges the health of the new and used electric vehicle (EV) markets by monitoring sales volume, days’ supply and average pricing. Each metric will be measured month over month and year over year.

Follow the link to view the entire series of EV Market Monitor reports.

For the official quarterly report on EV sales data, see the Q2 Electric Vehicle Sales Report.