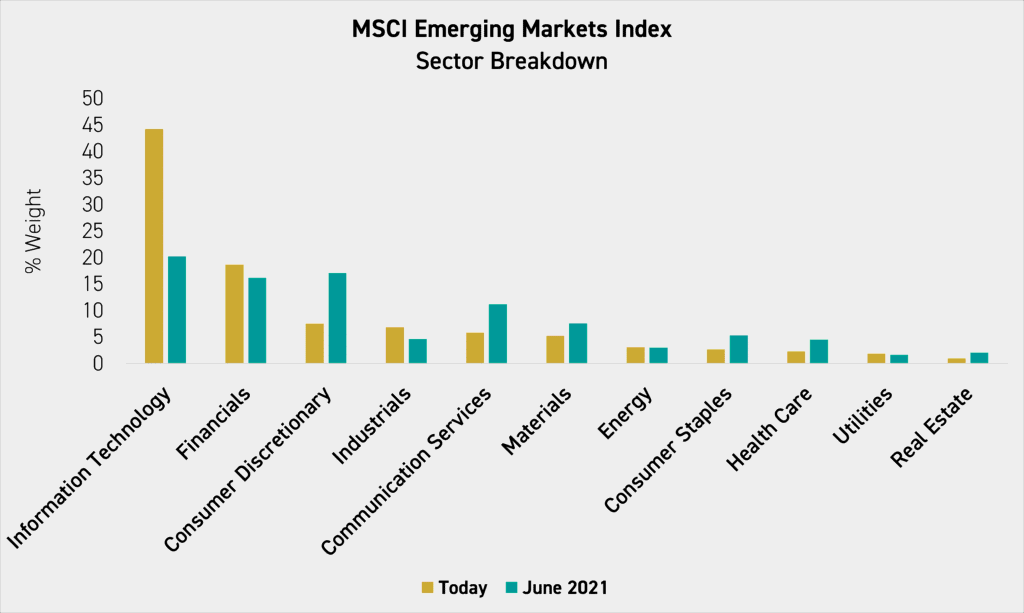

The outperformance of AI “picks and shovels”, i.e. chipmakers and hardware suppliers, in key emerging markets like Korea and Taiwan means that the MSCI Emerging Markets Index is now more heavily weighted toward technology stocks compared to just five years ago. The sector weight of Information Technology within the index has nearly doubled since 2021.

While this has been reflected in strong performance for long-term holders, we believe the sector shift begs the following questions:

- Does this change the fundamental thesis of investing in emerging markets from rising middle-class consumption to a story of technological supply chain development?

- Have emerging markets become too tied to developed markets to make them a good source of diversification*?

Thesis Change

The answer to the first question is nuanced. Yes, technology shares have been the main driver of emerging-market performance over the past two years. And, yes, consumption growth in certain larger emerging economies, such as China and Indonesia, has slowed. However, we believe investors in emerging markets should still assume long-term spending growth overall, which remains a core reason to invest in these markets. They may just need to dive a little deeper to find it.

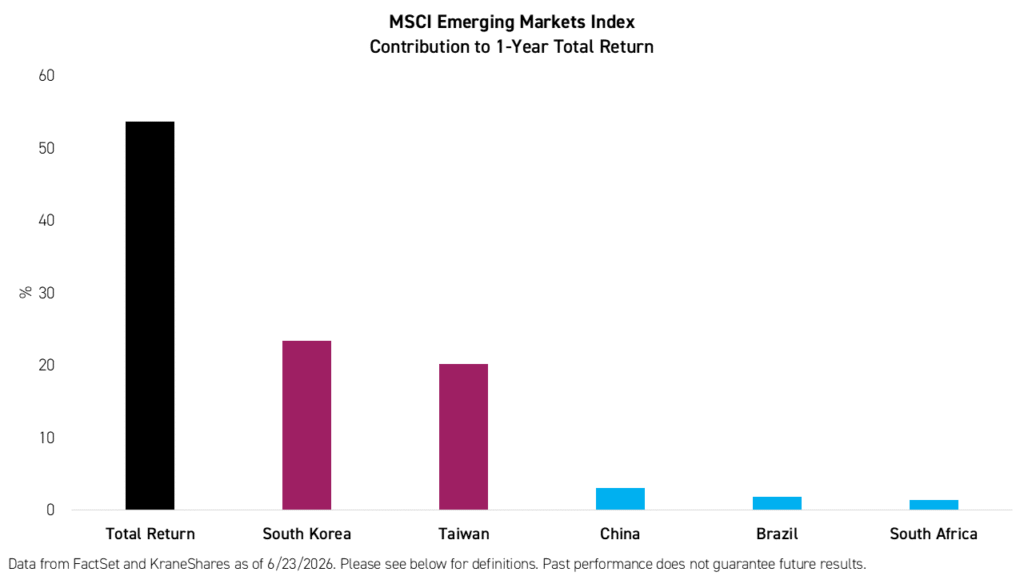

Technology stock gains have, by and large, been driven by a single narrative: global AI development and adoption. It just so happened that when AI enthusiasm reached a fever pitch, the largest nodes in the production of the powerful microchips required for the technology were based in Taiwan and Korea, both of which are emerging markets under MSCI’s definition. As a result, these two countries alone have accounted for 81% of the total return of the MSCI Emerging Markets Index over the past year.

In 2024, we highlighted the potential for a technology breakout in emerging markets, particularly Taiwan and Korea, with firms such as TSMC and SK Hynix. So, it did not surprise us when we saw these firms take off on AI demand.

However, we now believe investors may want to consider diversifying their exposure and breaking out different parts of emerging markets (EM) from the broader index. Investors may be able to accomplish this by rebalancing into other AI-related stocks from names including TSMC and SK Hynix, which have outperformed, and by overweighting specific markets where the consumption story could be stronger.

We believe focusing specifically on China’s internet sector, for example, accomplishes both goals by adding internet platforms that are exposed to both a potential consumption recovery in China and the AI theme. Our China Internet ETF the KraneShares CSI China Internet ETF (Ticker: KWEB) is designed to focus on the largest internet platforms in China, including AI hyperscalers such as Alibaba and Tencent. KWEB’s holdings currently trade at an average of 12 times earnings, representing a discount to the 18 times earnings average for the MSCI Emerging Markets Index.2 This difference is even starker when you consider that the MSCI Emerging Markets Index includes industrial and financial firms that are not within the AI theme.

Some economies are growing faster than others within EM, and investors may want to consider adding specific country exposures to depart from the technology theme and align themselves with a middle class consumption growth story. Vietnam recorded GDP growth of 8% in 2025 and is forecasted to be the fastest-growing economy in the Asia-Pacific region in 2026.1 Our Vietnam ETF the KraneShares Dragon Capital Growth of Vietnam Index ETF (Ticker: KPHO) is designed to provide investors with exposure to Vietnam’s locally-listed stocks using a proprietary fundamental growth methodology and is the only US-listed ETF to capture stocks otherwise restricted to foreign investors.3

Diversification

As the MSCI Emerging Markets Index has become increasingly concentrated in chipmakers, we believe it has also become heavily driven, from a revenue perspective, by capital expenditure (CapEx) from large firms in developed markets. As such, any disruption in these firms’ CapEx patterns could have a significant negative impact on emerging markets. In our opinion, this may reduce the inherent diversification that emerging markets can offer.

Looking under the hood can help solve for this, too. Investors may want to consider markets where reliance on developed-market CapEx might be lower. China may also be a good option here. Our China Technonogy & Semiconductor ETF the KraneShares China Technology STAR Market 50 Index ETF (Ticker: KSTR) is designed to focus on the 50 largest companies listed on China’s STAR (Science & Technology Innovation) Market. Most of its holdings are hardware suppliers currently geared towards China’s AI buildout.

Using US revenue exposure as a proxy for developed-market AI CapEx dependence, we observe that reliance is much higher in broader emerging markets than it is in China. According to data compiled by FactSet from the latest earnings releases, the share of revenue of KSTR’s holdings derived from the United States is 6%, compared to nearly 24% for the MSCI Emerging Markets Index as a whole.2

Conclusion

Although emerging markets have provided strong returns to investors in the past two years, these returns have been at the expense of true diversification from developed markets, in our opinion, and have effectively turned the MSCI Emerging Markets Index into a technology factor within investors’ portfolios. We believe the historical thesis behind investing in emerging markets, namely, middle-class consumption growth, remains intact, but investors may need to dig deeper to find it. Meanwhile, investors may also want to dig deeper into the index to find lower-valuation technology companies as well as those that are less dependent on CapEx from large firms located in developed markets.

*Diversification does not ensure a profit or guarantee against a loss.

For KWEB standard performance, risks, and top 10 holdings, please click here.

For KPHO standard performance, risks, and top 10 holdings, please click here.

For KSTR standard performance, risks, and top 10 holdings, please click here.

Citations:

- World Bank Data and estimates as of 12/31/2025.

- Data from FactSet as of 6/22/2026.

- Data from KraneShares and Bloomberg as of 3/31/2025.

Definitions:

MSCI Emerging Markets Index: The MSCI Emerging Markets Index is a free-float weighted equity index that captures large and mid cap representation across Emerging Market (EM) countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country. The index was launched on January 1, 2001.

Price to Earnings (P/E) Ratio: The P/E ratio measures how much investors are paying for each unit of a company’s earnings, calculated as share price divided by earnings per share (EPS). It is one of the most widely used quick-and-dirty valuation multiples in equity analysis.

Earnings per Share (EPS): A company’s total net profit or earnings divided by its total shares outstanding.

Capital Expenditure (CapEx): The money a company spends to buy, build, or significantly improve long‑term physical assets like property, plant, and equipment that will benefit the business for more than one year. It is capitalized on the balance sheet, rather than expensed immediately, and then depreciated or amortized over time.

Source link