Key Points

-

Tesla beat analysts’ revenue and earnings expectations in the first quarter (Q1) of 2026.

-

A down quarter in Q1 2025 makes Tesla’s year-over-year growth look more impressive than it is.

-

Tesla had around $480 million in one-time reliefs in Q1 2026.

- These 10 stocks could mint the next wave of millionaires ›

When Tesla (NASDAQ: TSLA) reported its first-quarter (Q1) 2026 earnings on April 22, they were met with mixed reactions.

On one hand, Tesla’s headline financial performance checked off many boxes and beat analysts’ expectations. Revenue, earnings per share (EPS), and free cash flow were all higher than expected. On the other hand, everything that glitters isn’t gold. The “why” behind the impressive numbers may dampen investors’ optimism or enthusiasm.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Let’s take a deeper dive into Tesla’s Q1 financial performance.

Image source: The Motley Fool.

What you’re comparing revenue against matters

For perspective on how Tesla’s Q1 revenue could be misleading, let’s imagine you’re a runner who runs 10-minute miles but gets hurt one day and can run only 20-minute miles. If you recover a bit and can now run 15-minute miles, yes, you are faster than before. However, you’re still slower than you were. That’s why your comparison point matters.

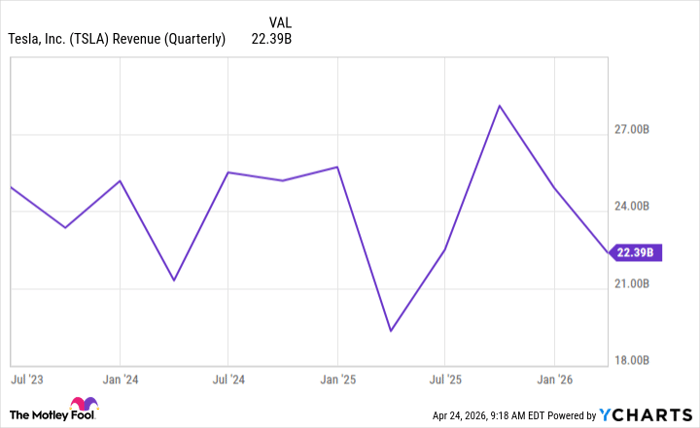

That’s more or less the story of Tesla’s revenue. During Q1 2025, Tesla modified some factories to begin producing its Model Y line. This slowed production and caused revenue for the quarter to drop by 9% from the previous year to $19.3 billion. That was more than $6 billion less than it made the quarter before.

So although Tesla’s $22.4 billion in Q1 2026 revenue was up 16% year over year (YOY), it’s worth remembering that it’s being compared to revenue in a down quarter. It was around $2.7 billion less than the previous quarter, and Tesla missed its vehicle delivery target.

TSLA Revenue (Quarterly) data by YCharts

Profits boosted by one-off events

Tesla’s gross profit increased by 50% YOY, and its non-GAAP (adjusted) EPS was $0.41 (beating analysts’ expectation of $0.36).

Much of the improved profit came from what Tesla described as an “increase in automotive one-time benefits related to warranty and tariffs.” Around $250 million came from a refund on tariffs it paid in previous quarters, and around $230 million came from warranty write-downs (whereby Tesla reduces how much it has set aside for repairs).

This roughly $480 million in one-time reliefs is largely why Tesla’s operating income increased by 136% YOY.

Free cash flow got an accounting boost

Tesla’s $1.4 billion in free cash flow might have been the biggest surprise because many people expected it to lose money in the quarter. However, one change in accounting management has much to do with it.

Typically, Tesla pays its suppliers in 61 days, but in Q1 2026, it extended the payment term to 71 days. This allowed Tesla to delay payments and keep more cash for the time being. It’s like getting an extension on your credit card bill: Yes, you get to keep more money in the bank for now, and it looks nice, but eventually you’ll have to pay.

Tesla says it expects negative cash flow for the rest of the year, especially as it increases spending, with $25 billion in capital expenditures.

Should investors be skeptical?

Tesla’s car business is struggling; there’s no doubt about that. However, it’s pretty clear that the company has no real interest in being a traditional car manufacturer. The long-term goals are its robotaxi network, robotics, and AI. Automotive sales are more than 72% of its total revenue, so it can’t completely deprioritize its core business, but it’s going through a transitional period.

If you’re a current and long-term investor and believe in Tesla’s vision, then this quarter shouldn’t change your mind about that. The struggling car business should be a yellow flag, but you’re banking on it being able to buy itself enough time to make its autonomous ambitions work.

If you’re thinking about making your first Tesla investment, now isn’t a great time, in my opinion. The company’s car business is declining, it still has a lot to prove in its businesses apart from cars, and it’s extremely expensive.

Tesla’s stock is trading at 182 times its projected earnings over the next 12 months. For perspective, that’s around 5.5 times as expensive as the second-most-expensive “Magnificent Seven” stock, Amazon (33). That’s expensive for any stock at any time, but especially for a company with as many question marks as Tesla.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $540,224!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $51,615!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $498,522!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of April 25, 2026.

Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Tesla. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.