Currency markets is heading to the end of the week on a subdued note as a series of developments across Canada, Japan and the Middle East ultimately reinforced existing narratives rather than triggering a meaningful repricing. Canadian Dollar gained modest support after another resilient employment report, while Yen held onto earlier gains sparked by Japan’s pension fund initiative. Yet neither move developed into a sustained trend. Elsewhere, easing tensions between the US and Iran helped keep Brent crude comfortably below the critical USD 80 mark, allowing broader FX trading to settle into consolidation.

Canada Jobs Reinforce BoC Hold

Canadian Dollar firmed modestly in the early US session after June employment data came in slightly stronger than expected. Employment rose by 18.2k against expectations for a 10.0k increase, while the unemployment rate unexpectedly fell to 6.5% from 6.6%. The report was further supported by a steady participation rate and firmer wage growth, presenting a broad picture of a labor market that continues to outperform expectations.

The figures pose a meaningful challenge to any outright dovish Bank of Canada narrative. They reinforce Governor Tiff Macklem’s assessment that the domestic economy has remained resilient despite growing uncertainty surrounding Canada’s evolving trade relationship with the United States. At the same time, the report falls well short of making a convincing case for renewed tightening. With structural uncertainty surrounding the USMCA review still clouding the medium-term outlook, markets continue to expect the BoC to leave rates unchanged through the remainder of the year. Next week’s policy meeting is unlikely to produce a material shift in guidance.

Japan’s Structural Idea Needs Time

Yen also remained generally firmer after Finance Minister Katayama suggested encouraging pension funds to increase investment in domestic financial assets. Investors viewed the comments as pointing toward a potential structural solution to one of the Ten’s longstanding weaknesses—persistent capital outflows into overseas assets—rather than another round of tactical currency intervention.

However, the initial enthusiasm has begun to fade. The proposal remains an idea rather than a formal policy initiative, and any meaningful portfolio reallocation would require decisions by independent institutional investors such as GPIF. Even if implemented, the process would unfold gradually over years rather than weeks, while the wide interest-rate differential between Japan and the United States continues to underpin carry trades. As a result, today’s gains lacked strong follow-through despite the favorable initial market reaction.

Oil Retreat Keeps Broader Markets Calm

Meanwhile, geopolitical concerns also moderated after another round of hostilities between the United States and Iran earlier in the week. While attacks briefly renewed worries about global energy supplies and the security of Strait of Hormuz transit, Brent crude eased back toward USD 76 after failing to sustain gains above USD 80. The pullback suggests markets continue to view the latest flare-up as another episode within an ongoing negotiation process rather than the beginning of a renewed regional conflict.

Reports that both sides have returned to technical discussions further supported that interpretation. As long as Brent remains below the USD 80 threshold, investors appear reluctant to rebuild a significant geopolitical risk premium across broader financial markets.

For the week so far, New Zealand Dollar remains the strongest major currency, followed by Sterling and Canadian Dollar, while Swiss Franc, Yen and Euro lag the performance table.

Yen Jumps as Markets See Katayama’s Pension Fund Push as Structural Fix for Currency Weakness

The Yen’s latest rally wasn’t driven by intervention speculation. Markets instead focused on a potential structural shift in Japan’s capital flows after Finance Minister Katayama encouraged greater domestic investment by pension funds. Find out why investors believe this could have a more lasting impact than traditional FX intervention. Read More.

Canada Employment Tops Forecast as Jobless Rate Falls Again

Canada’s employment rose by 18.2k in June while the unemployment rate fell to 6.5%, reinforcing labor market resilience ahead of next week’s Bank of Canada meeting. Read More.

Japan PPI Hits Fastest Pace Since 2023 as Energy, AI Demand Drive Costs Higher

Japan’s wholesale inflation accelerated to its fastest pace since March 2023 as the Middle East energy shock, booming AI-related metals demand and a weaker yen combined to push producer prices higher. Read More.

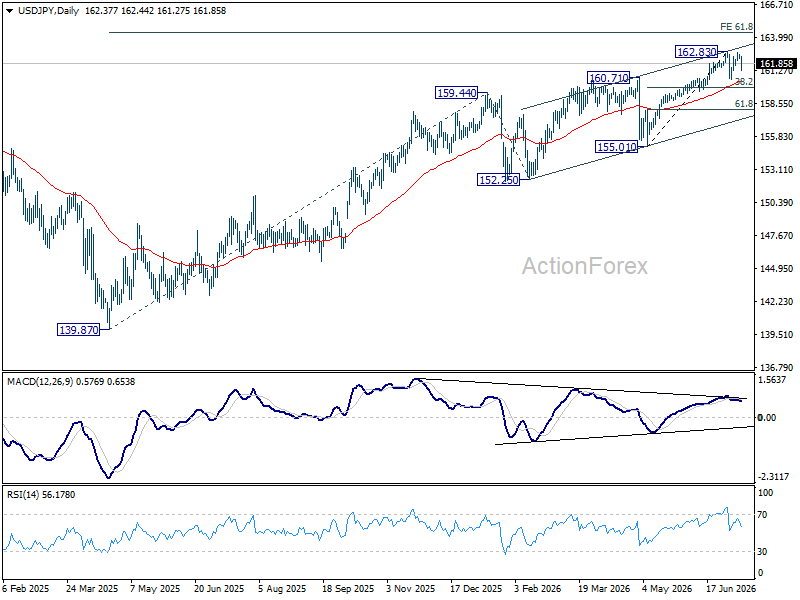

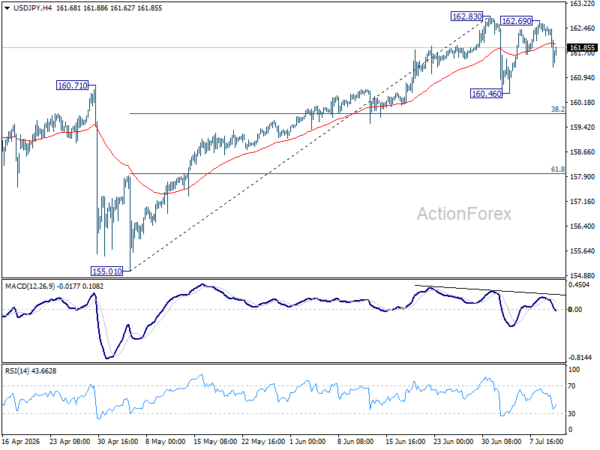

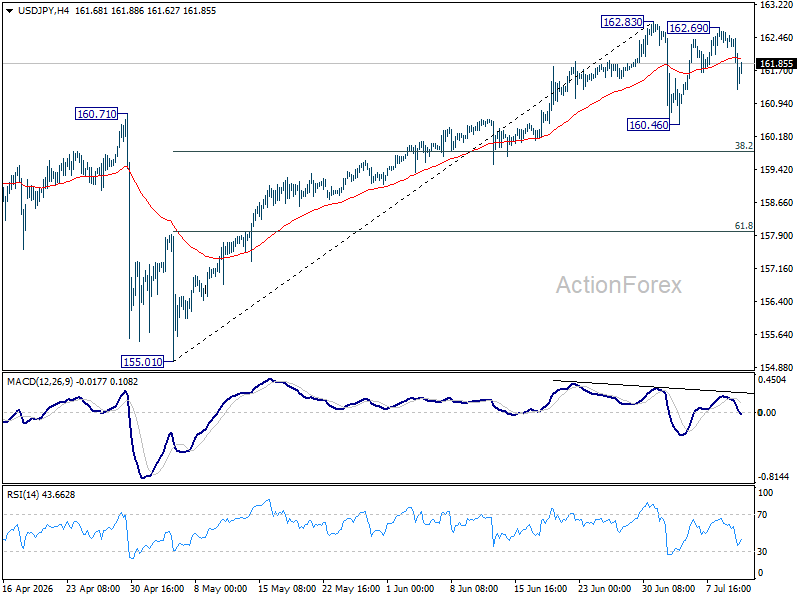

USD/JPY Daily Outlook

USD/JPY falls sharply today but still it’s bounded in range below 162.83. Intraday bias remains neutral and more consolidations would be seen. In case of deeper pullback, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.