Wall Street Expected a Slowdown in Q2. Corporate America Had Other Plans.

Uncategorized

Wall Street Expected a Slowdown in Q2. Corporate America Had Other Plans.

012 mins

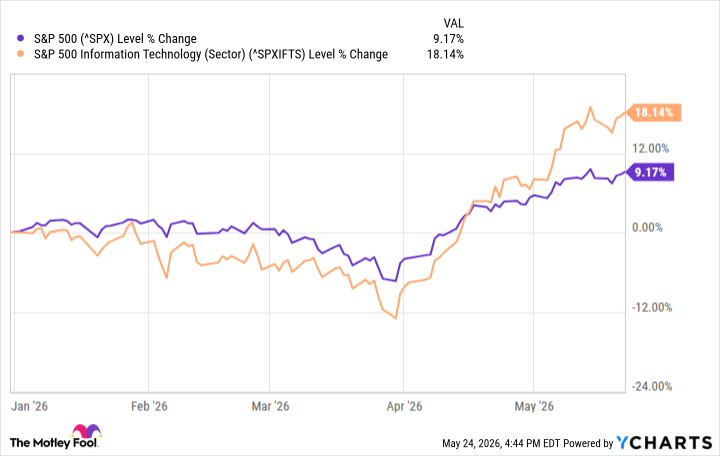

Stocks might have finished the first quarter (Q1) on a low note thanks to the military conflict with Iran. Anyone counting on that weakness to persist into Q2, however, was sorely mistaken. Down 5% for the year as of the end of March, the S&P 500(SNPINDEX: ^GSPC) is now up more than 9% since the end of 2025.

Earnings did a great deal of the work, of course. Numbers from FactSet indicate 84% of the S&P 500’s constituents topped Q1 analyst earnings estimates. In fact, Q1’s earnings growth of more than 28% is the fastest year-over-year growth since the final quarter of 2021 when comparisons were made to the worst part of the COVID-19 pandemic.

Will AI create the world’s first trillionaire? Our team just released a report on a little-known company, called an “Indispensable Monopoly,” providing the critical technology Nvidia and Intel both need.

Thank technology companies like Meta and Alphabet(NASDAQ: GOOG)(NASDAQ: GOOGL), which made the biggest contribution to the improvement. That said, energy companies and their stocks have benefited from oil’s soaring prices as well.

The question is, can this bullishness last? For that matter, does it deserve to? Maybe. However, investors would be wise to exercise a bit of caution here.

Not the best way of doing things

Don’t misread the message. The stock market isn’t doomed. There’s more risk than there seems to be on the surface though.

But first things first.

Although Q2 and the year’s overall market gains so far are impressive, they’re also poorly balanced. Although energy stocks have technically outperformed everything else (technology names like Nvidia(NASDAQ: NVDA), Apple, Alphabet, and Microsoft(NASDAQ: MSFT) collectively account for roughly a third of the S&P 500’s total value), their 20% year-to-date gain is responsible for most of the overall market’s strength since the end of last year. For perspective, the tech-heavy “Magnificent Seven’s” average Q1 profit growth was an incredible 63% versus an average of only 17% for the S&P 500’s other 493 stocks.

It’s not necessarily a recipe for disaster. As poorly balanced as the broad market’s performance may be, the overall numbers are still… the overall numbers. Largely driven by technology stocks’ predicted growth, analysts expect earnings gains of 23% from the S&P 500 for all of 2026 followed by 15% growth in 2027; the index’s forward-looking (2027) price-to-earnings (P/E) ratio is reasonable at just a little less than 20.

There is one arguable potential pitfall to these bullish metrics. That is, most of the technology sector’s future growth depends on other technology companies’ expected growth. If one link in the chain fails, it could reduce revenue and earnings expectations across the board.

Unhealthy codependency

It’s called “circular spending,” a term that started last year when several technology giants began spending heavily to add capacity to meet the AI-driven demand from other technology companies.

The industry’s circular spending web is intricate to be sure. For example, last September, AI platform OpenAI agreed to purchase millions of Nvidia-made processors to put to work in its next-generation AI data centers. But Nvidia is also a major stakeholder in OpenAI, agreeing to invest as much as $100 billion in the privately held company, just as it’s a major shareholder in data-center operator CoreWeave(NASDAQ: CRWV), which also utilizes Nvidia’s tech. So does Oracle(NYSE: ORCL), which has also agreed to sell $300 billion worth of AI cloud services to OpenAI. That’s the same OpenAI that’s also purchasing processing chips from Nvidia rival Advanced Micro Devices(NASDAQ: AMD) — a deal that makes OpenAI a major AMD shareholder. It is also a major shareholder of CoreWeave — alongside Nvidia — in exchange for supplying OpenAI with nearly $12 billion worth of infrastructure services.

And there’s more. Software giant Microsoft owns a huge piece of OpenAI, which serves Microsoft, which in turn serves CoreWeave, while also collaborating with Nvidia, which even made a $5 billion equity investment in rival chipmaker Intel as part of an agreement to co-develop AI data-center solutions.

Image source: Getty Images.

Such intra-industry dealmaking isn’t unheard of. This complexity, however, is unusual, not to mention a little dangerous. Not only are partners and investors ultimately serving those partners’ and investors’ competitors, but much of this AI investment is based on the assumption that demand for these underlying companies’ goods and services is as strong as is being implied. If one of these outfits has overestimated future demand, it could potentially undermine every one of these direct and indirect relationships.

In other words, almost every major company within the technology sector is ultimately betting on every other major tech companies’ continued, robust success. And this is happening at a time when corporate users of AI are starting to question its value. It’s a risk to all investors simply because the overall market’s strong earnings outlook for the year ahead, which is what’s been driving stocks to record highs this quarter, is largely rooted in the assumption that this dealmaking will lead to serious revenue growth. Some deals will. Some might not.

Just keep your expectations realistic

Don’t panic. Although things rarely pan out quite as well as the highest hopes suggest they will, they also rarely turn into the outright disasters that some fear. Outcomes are typically somewhere in the middle of the extreme possibilities.

Still, Q2’s bullishness reflects a future that probably won’t be quite as impressive as the recent past. That’s the less direct way of saying the S&P 500’s 18% rally since its late-March low isn’t likely to repeat itself from its current level, particularly now that we’re in a traditionally slow time of year for stocks.

And that’s even more so the case given rising inflation and abysmal consumer sentiment. Even the corporate and institutional business that’s been fueling the AI industry’s gains lately still ultimately needs strong consumer demand to drive sustained growth.

A more serious economic slowdown or full-blown recession, of course, is apt to crimp AI spending plans first and foremost just because this would be the easiest areas of investment to dial back in a hurry.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $477,813!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,320,088!*

Now, it’s worth noting Stock Advisor’s total average return is 986% — a market-crushing outperformance compared to 208% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Apple, Intel, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool has a disclosure policy.