By the time the Bank of Canada announces its policy decision today, the Canadian Dollar has already built a powerful foundation for further gains. USD/CAD has fallen to its lowest level in nearly a month, supported not by a single catalyst but by three reinforcing forces: a broad retreat in the US Dollar after softer inflation data, higher oil prices that strengthen Canada’s export outlook, and growing expectations that the Bank of Canada may sound more hawkish than markets anticipated only a week ago.

The first two drivers have already reshaped the currency outlook. June’s weaker-than-expected US CPI prompted investors to scale back Federal Reserve tightening expectations, weighing on the Dollar across major currency pairs. At the same time, Brent crude has surged above $86 as renewed US-Iran hostilities threaten energy supplies through the Strait of Hormuz. For Canada, rising oil prices are more than just a global inflation story—they improve the country’s terms of trade and typically provide direct support for the Canadian Dollar, helping explain why the Loonie has outperformed most of its peers following the inflation data.

The Bank of Canada now has an opportunity either to reinforce or challenge that momentum. Economists overwhelmingly expect a sixth consecutive hold at 2.25%, making the decision itself unlikely to surprise. The more important question is whether Governor Tiff Macklem adjusts his message in response to oil’s renewed surge. His previous characterization of policy as balancing weaker growth against energy-driven inflation was formed before Brent’s latest rally, meaning the Monetary Policy Report may already understate current inflation risks. Markets will therefore pay closer attention to Macklem’s live assessment than to the published projections.

That leaves the accompanying statement and Macklem’s press conference as the key market events. Investors will focus on whether the Governor continues to describe policy as a balanced dilemma or acknowledges that the renewed energy shock has tilted inflation risks higher. Any discussion of the ongoing CUSMA trade review will also be closely watched, as it remains an important downside risk to Canada’s growth outlook. Even without signaling an imminent rate increase, a modestly more hawkish tone could encourage markets to further increase expectations of tightening in early 2027, where pricing is already becoming increasingly balanced.

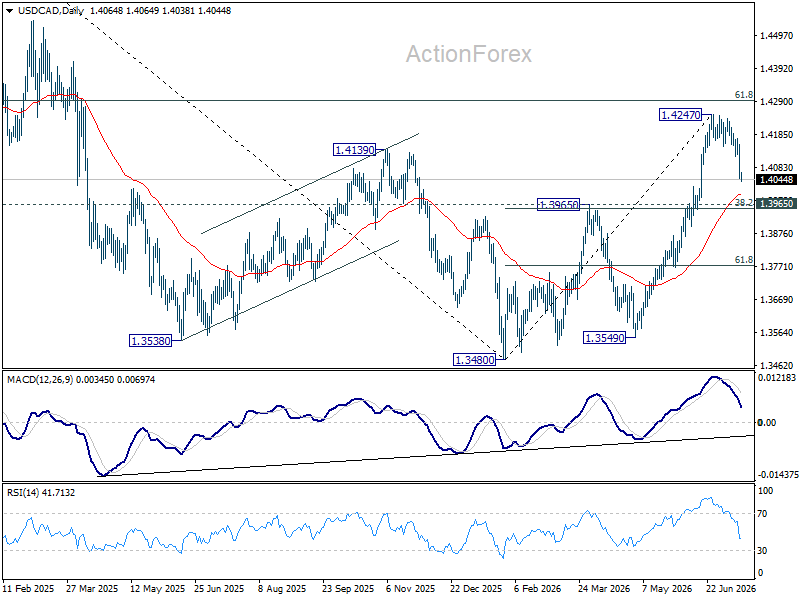

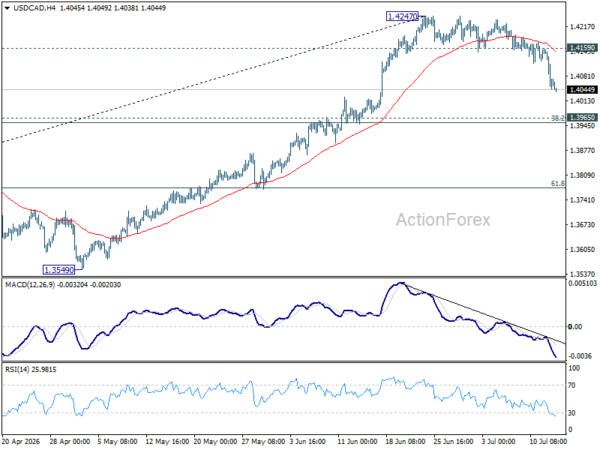

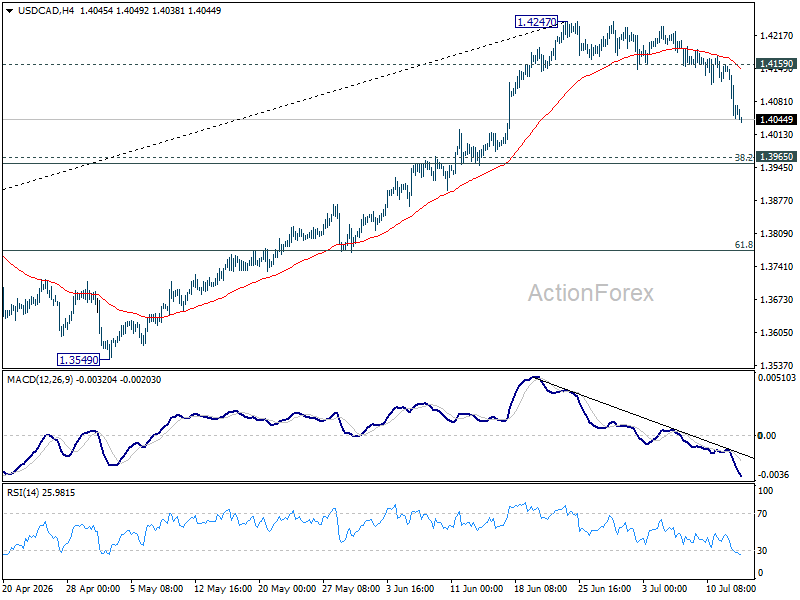

Technically, USD/CAD is approaching an important inflection point. While the decline from 1.4247 has accelerated, it is still viewed as a correction within the broader uptrend from 1.3480. Strong support is expected between former resistance at 1.3965 and 38.2% retracement of 1.3480 to 1.4247 at 1.3954. Break of 1.4159 minor resistance will indicae that the correction has completed.

However, a decisive break below 1.3954/65 would suggest the advance from 1.3480 has completed as a three-wave corrective rebound after failing near 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Such a development would shift the near-term technical outlook decisively in favour of further Canadian Dollar strength.