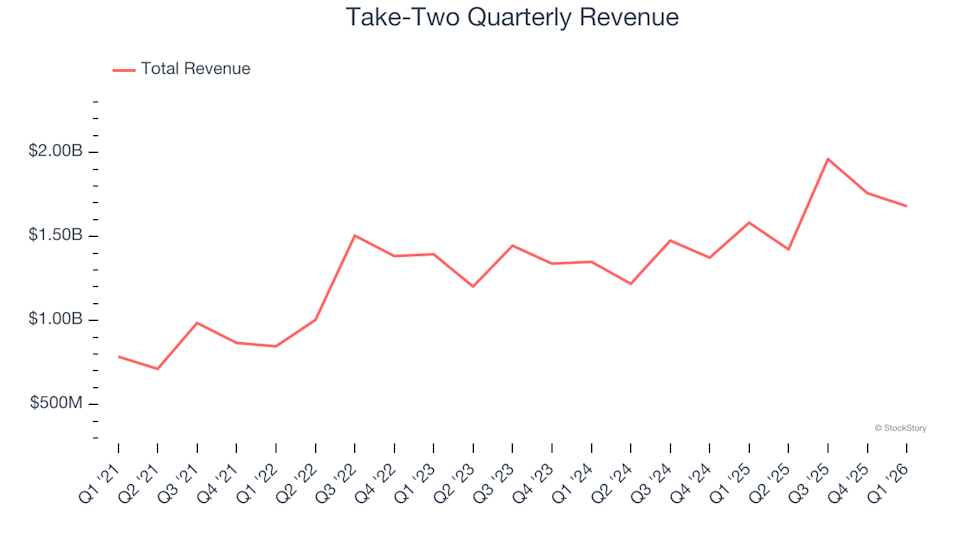

Video game publisher Take Two (NASDAQ:TTWO) reported Q1 CY2026 results topping the market’s revenue expectations , with sales up 6.2% year on year to $1.68 billion. On the other hand, next quarter’s revenue guidance of $1.48 billion was less impressive, coming in 4.1% below analysts’ estimates. Its GAAP loss of $0.32 per share was 38.2% above analysts’ consensus estimates.

Is now the time to buy Take-Two? Find out in our full research report.

Take-Two (TTWO) Q1 CY2026 Highlights:

-

Revenue: $1.68 billion vs analyst estimates of $1.56 billion (6.2% year-on-year growth, 7.9% beat)

-

EPS (GAAP): -$0.32 vs analyst estimates of -$0.52 (38.2% beat)

-

Adjusted EBITDA: $243.7 million vs analyst estimates of $189.3 million (14.5% margin, 28.7% beat)

-

Revenue Guidance for Q2 CY2026 is $1.48 billion at the midpoint, below analyst estimates of $1.54 billion

-

EPS (GAAP) guidance for the upcoming financial year 2027 is $0.65 at the midpoint, missing analyst estimates by 82.7%

-

EBITDA guidance for the upcoming financial year 2027 is $1.04 billion at the midpoint, below analyst estimates of $1.95 billion

-

Operating Margin: 0.6%, up from -239% in the same quarter last year

-

Free Cash Flow Margin: 11.8%, down from 13.4% in the previous quarter

-

Market Capitalization: $43.82 billion

Company Overview

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ:TTWO) is one of the world’s largest video game publishers.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Take-Two grew its sales at a mediocre 8.9% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Take-Two.

This quarter, Take-Two reported year-on-year revenue growth of 6.2%, and its $1.68 billion of revenue exceeded Wall Street’s estimates by 7.9%. Company management is currently guiding for a 3.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 36.5% over the next 12 months, an acceleration versus the last three years. This projection is eye-popping and suggests its newer products and services will fuel better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.