Alphabet GOOGL is set to report second-quarter 2026 results on July 22.

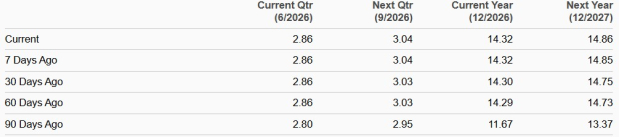

For second-quarter 2026, the Zacks Consensus Estimate for earnings is pegged at $2.86 per share, unchanged over the past 30 days, and indicating 23.81% year-over-year growth.

The consensus mark for second-quarter revenues is pegged at $101.22 billion, implying growth of 23.86% from the year-ago quarter’s reported figure.

Alphabet has an impressive earnings surprise history. Its earnings outpaced the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 34.43%.

Consensus Estimate Trend

Image Source: Zacks Investment Research

Let’s see how things have shaped up for the upcoming announcement:

Alphabet Inc. Price and EPS Surprise

Alphabet Inc. price-eps-surprise | Alphabet Inc. Quote

Growing AI Usage in Search & Cloud to Aid GOOGL’s Q2 Results

Alphabet’s second-quarter results are expected to have benefited from sustained momentum in Google Search. AI Overviews and AI Mode have been increasing user engagement and pushing search queries to record levels, while Gemini is improving Google’s understanding of longer and more complex queries. This should have supported paid-click growth, ad relevance and advertiser returns. The continued adoption of AI Max and Performance Max could also have lifted advertising demand as businesses use generative AI for targeting, creative development and bidding. Search revenues increased 19% in the first quarter of 2026, supported by retail and financial-services advertisers. The trend is expected to have continued in the second quarter of 2026.

Google Cloud is likely to have remained the fastest-growing part of Alphabet’s business. First-quarter Cloud revenues surged 63% year over year to $20 billion as enterprise AI solutions became the segment’s largest growth contributor. Demand remains strong for Gemini models, AI infrastructure, cybersecurity, data analytics and Workspace. Cloud’s backlog reached roughly $462 billion, with slightly more than half expected to convert into revenues over the next 24 months. A fuller quarterly revenue contribution from Wiz after the acquisition closed in March is expected to have benefited top-line growth.

YouTube should have provided another growth catalyst, supported by direct-response advertising, connected-TV viewing, Shorts monetization and improving brand demand. U.S. users are watching more than 200 million hours of YouTube content on television screens each day, while Gemini-powered recommendations and creator-advertiser matching should have improved engagement and advertising effectiveness. Subscription revenues are expected to have benefited from YouTube Music, Premium and Premium Lite, which were scheduled to enter more than a dozen additional countries during the second quarter. Google One’s AI plans and the Gemini app should further strengthen subscriptions, platforms and devices revenues after Alphabet reached 350 million paid subscriptions in the first quarter of 2026.

However, Alphabet’s aggressive AI infrastructure expansion could weigh on second-quarter profitability and free cash flow. The company raised its 2026 capital-expenditure outlook to $180-$190 billion, with most spending aimed at servers, data centers and networking infrastructure. These investments are expected to have increased depreciation, energy, equipment and data-center operating costs. GOOGL’s plan to continue hiring in AI and Cloud and spending on marketing for Gemini and Search is expected to have raised operating expenses in the to-be-reported quarter.

The dilutive effect of the Wiz acquisition, as well as weakness in Google Network advertising, has been a headwind. Network revenues declined 4% year over year in the first quarter, reflecting lower AdSense revenues and a 9% decline in impressions. The trend is expected to have continued in the second quarter of 2026.

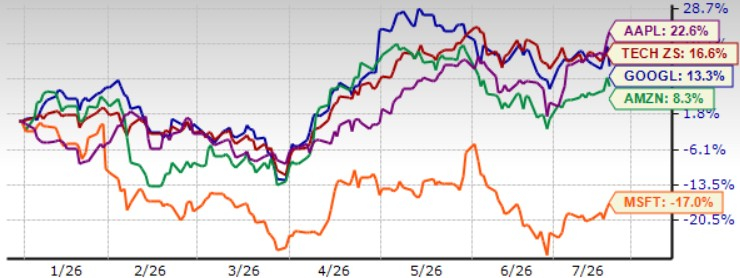

GOOGL Shares Lag Sector, Trade at a Premium

Alphabet’s shares have climbed 13.3% year to date (YTD), underperforming the broader Zacks Computer & Technology sector’s return of 16.6%. Alphabet shares have underperformed Apple AAPL but outperformed Amazon AMZN and Microsoft MSFT over the same timeframe. While Apple and Amazon shares have jumped 22.6% and 8.3% YTD, respectively, Microsoft has dropped 17%.

GOOGL Stock’s Price Performance

Image Source: Zacks Investment Research

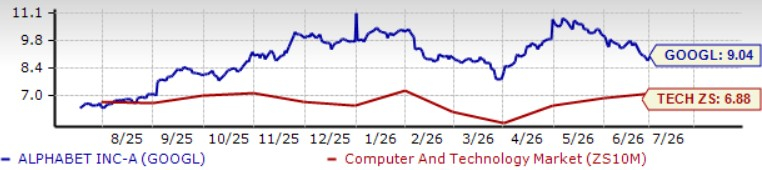

GOOGL shares are overvalued, as suggested by Value Score D.

Currently, GOOGL is trading at a premium, with a forward 12-month price/sales of 9.04X compared with the broader sector’s 6.88X, Apple’s 9.6X, Microsoft’s 7.75X and Amazon’s 3.04X.

GOOGL Shares Trade at a Premium

Image Source: Zacks Investment Research

GOOGL Benefits From AI Push & Cloud

Alphabet’s most significant long-term opportunity is the integration of Gemini across its global product portfolio. Gemini already powers products serving billions of users, including Search, YouTube, Maps, Chrome and Workspace. AI Mode, personalized search, agentic features and the Gemini app can increase engagement while creating new advertising, subscription and transaction opportunities. Alphabet has also reduced the cost of core AI responses by more than 30%, suggesting that improving model and infrastructure efficiency could support profitable AI monetization over time.

Google Cloud has substantial long-term growth visibility. Approximately 75% of Cloud customers are using Alphabet’s AI products, while new customer acquisition and the number of deals worth between $100 million and $1 billion doubled year over year in the first quarter of 2026. The accelerating Cloud backlog ($462 billion at the end of Q1), growing Gemini Enterprise adoption and demand for Vertex AI, BigQuery, Workspace and Wiz provide a multiyear revenue pipeline. Direct sales of TPUs for customer-owned data centers also expand Alphabet beyond hosted cloud services into a new infrastructure market.

GOOGL’s vertically integrated AI stack is a structural advantage. The company controls models, software, data-center infrastructure and custom processors such as TPUs and Axion CPUs while also offering NVIDIA GPUs. This breadth allows Alphabet to optimize performance and costs across Search, Cloud and consumer applications.

Buy GOOGL Ahead of Q2

While elevated AI infrastructure investments and higher operating expenses may weigh on near-term margins, robust AI adoption across Search, Cloud and YouTube are strengthening GOOGL’s competitive position in fast-growing AI and cloud markets. With Gemini driving engagement across its ecosystem, a rapidly expanding Cloud business and a differentiated full-stack AI strategy, Alphabet remains well positioned to capitalize on the long-term AI opportunity. Investors should continue to benefit from the company’s strong innovation pipeline and diversified growth.

Alphabet currently sports a Zacks Rank #1 (Strong Buy), suggesting that it may be wise to buy the stock ahead of second-quarter earnings. You can see the complete list of today’s Zacks #1 Rank stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.