New Zealand Dollar outperformed across the board today after a much stronger-than-expected manufacturing survey reinforced confidence that the economy is gaining momentum following the Reserve Bank of New Zealand’s rate hike. At the other end of the spectrum, Canadian Dollar is the weakest major currency despite another sharp rebound in oil prices, underscoring that structural concerns over Canada’s economic outlook continue to outweigh support from higher crude prices. Meanwhile, Dollar softened modestly as traders awaited fresh developments on the fragile US-Iran ceasefire, with Brent failing to sustain an early move above the key $80 level.

Kiwi’s rally was underpinned by June’s impressive BusinessNZ Performance of Manufacturing Index, which surged to 59.7, its highest reading since mid-2021. The improvement was broad-based, with new orders, production, employment and deliveries all strengthening sharply, suggesting the recovery is becoming increasingly self-sustaining. Even BNZ Head of Research Stephen Toplis said he was “staggered” by the magnitude of the rebound, noting that excluding the post-pandemic reopening surge, the latest reading was the strongest since May 2017.

The data also provide strong ex-post validation for the RBNZ’s decision to raise the Official Cash Rate to 2.50% yesterday. While policymakers stopped short of signalling another imminent move, the report strengthens the case that policy normalization still has further to run should improving momentum spread beyond manufacturing into the broader economy. Some economists, including Westpac, continue to expect additional rate hikes later this year.

By contrast, the Canadian Dollar struggled even as Brent crude briefly traded above $80. Markets appear focused on Canada’s longer-term challenges rather than short-term support from commodity prices. The Trump administration’s decision not to automatically extend the USMCA has introduced a fresh uncertainty for investment and trade, reinforcing Bank of Canada Governor Tiff Macklem’s repeated assessment that the economy is undergoing a structural adjustment as trade relations with the United States evolve.

That backdrop also helps explain why the BoC has shown little inclination to respond to higher oil prices with a more hawkish policy stance, arguing that temporary energy shocks are unlikely to generate sustained inflation. Attention now turns to Friday’s June employment report. A softer-than-expected outcome would reinforce expectations that the BoC remains comfortably on hold and could trigger another round of Canadian Dollar selling.

Oil remains an important macro variable, but today’s price action suggests markets are not yet ready to rebuild a full geopolitical risk premium. Brent briefly broke above the psychological $80 mark after renewed US-Iran tensions, but quickly surrendered those gains as investors continued to bet that both sides retain strong incentives to keep the Strait of Hormuz open and negotiations alive.

A sustained move above $80, particularly if accompanied by a break through nearby technical resistance, would indicate that markets are once again pricing a more persistent disruption to global energy supplies. Until then, today’s retreat suggests geopolitical concerns remain contained rather than dominant.

GBP/CAD Hits Decade High as USMCA Shock Adds New Driver Ahead of Jobs Data

GBP/CAD has broken to a new decade high, but the story is not just about Sterling strength. Discover why the USMCA review has become a new structural headwind for the Canadian Dollar and why Canada’s jobs report could determine whether the rally accelerates further. Read More.

Gold and Silver Bears Need One More Trigger: Brent Above $80

Gold and silver have turned lower again, but bears may need one more confirmation before pressing for a full downside breakout: Brent holding above $80. A sustained oil rally would revive inflation concerns, reinforce Fed tightening risks, and increase pressure on precious metals. Read More.

ECB Minutes: Inflation Damage Already Too Broad to Ignore

The ECB’s June rate hike was never just about higher oil prices. The minutes reveal policymakers believed inflation had already spread too far across the economy, making tighter policy necessary even if Middle East tensions had eased. Discover why the Governing Council saw waiting as no longer an option. Read More.

New Zealand Manufacturing PMI Surges to Strongest Since 2021 as Orders Soar

The BusinessNZ PMI surged to a near four-year high in June, surprising even BNZ economists. Find out what fueled the sharp turnaround and why stronger order books could signal a sustained manufacturing recovery. Read More.

China Inflation Cools Further as Consumer Prices Ease, Producer Inflation Hits Three-Year High

China’s latest inflation data told two very different stories. Consumer inflation softened again as lower energy prices eased household costs, while producer inflation climbed to its highest level since 2022 on resilient industrial demand. Read More.

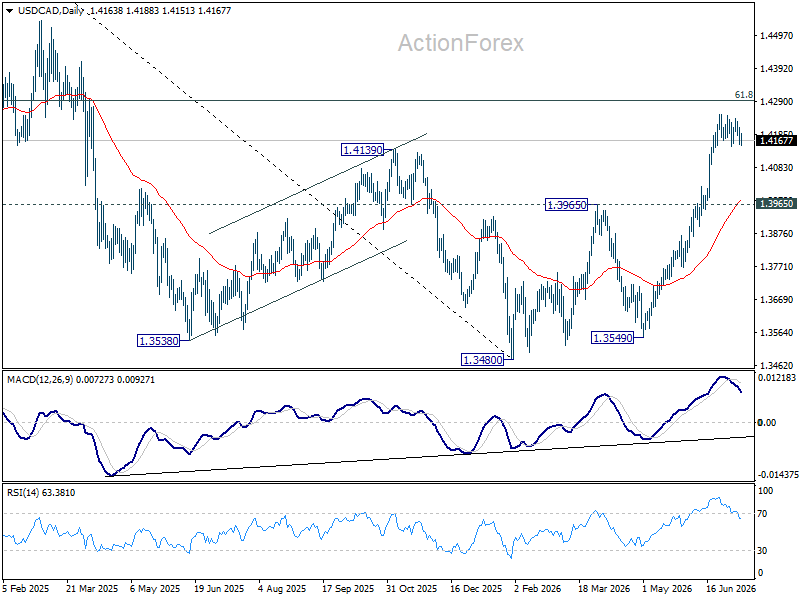

USD/CAD Daily Outlook

Consolidation continues below 1.4247 and intraday bias remains neutral in USD/CAD. Deeper pullback cannot be ruled out. But downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It’s still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.