Intel (INTC +1.18%) has been on a stellar run in 2026, with shares of the chip giant rising 222% as of this writing. The stock’s stunning rally has been fueled by its improving financial results and growing influence in the artificial intelligence (AI) chip market.

However, rival chipmaker Advanced Micro Devices (AMD +4.09%) poses a major threat to Intel’s stock market fortunes. The latest numbers revealed by market research firm Mercury Research (via Tom’s Hardware) make it clear that Intel continues to lose ground to AMD in the lucrative server central processing unit (CPU) market.

Let’s see why AMD could derail the impressive rally in Intel stock.

Image source: Intel.

AMD’s rapidly improving market share is bad news for Intel

According to Mercury Research, Intel’s share of server CPUs fell to 66.8% in the first quarter of 2026, down from 72.8% in the year-ago period. Intel’s weakening position in this market can be attributed to the popularity of AMD’s Epyc server CPUs, which are in terrific demand from hyperscalers and enterprises.

Today’s Change

(4.09%) $18.39

Current Price

$467.98

Key Data Points

Market Cap

$733B

Day’s Range

$461.78 – $481.50

52wk Range

$107.67 – $481.50

Volume

1.5M

Avg Vol

38.8M

Gross Margin

47.09%

As noted by AMD CEO Lisa Su on the company’s recent earnings call:

In Server, we delivered our fourth consecutive quarter of record server CPU revenue. Revenue increased more than 50% year-over-year with sales to both Cloud and Enterprise customers each growing more than 50%. Share gains accelerated year-over-year, reflecting the ramp of fifth-gen EPYC Turin CPUs and continued strength of fourth-gen EPYC processors across a wide range of workloads.

Su added that cloud service providers have increased the deployment of Epyc server processors to support AI workloads. Importantly, the company is confident of gaining more market share in the server CPU space, driven by the addition of new customers “across financial services, healthcare, industrial and digital infrastructure companies.”

What’s more, AMD claims that its next-generation server CPUs could further strengthen its competitive advantage over Intel by delivering higher performance at lower cost. Another important point worth noting is that customers are willing to pay a premium for AMD’s server CPUs. The company’s revenue share of the server CPU market was 46.2% in Q1, even though its unit share was a third.

So, it appears that the performance and cost advantages AMD claims over rivals are translating into strong pricing power. At the same time, Intel is struggling to produce enough chips to meet customer demand. CEO Lip-Bu Tan made it clear on the company’s April earnings call that “demand continues to run ahead of supply for all our businesses, especially for Xeon server CPUs.”

AMD seems to be making the most of Intel’s troubles, winning both unit and revenue share in a lucrative market it expects to grow at an annual rate of 35% through 2030, generating $120 billion in revenue by the end of the decade. AMD’s share gains are also translating into stronger growth for the company. The company’s data center segment revenue shot up by 57% year over year in the first quarter of 2026 to $5.8 billion.

On the other hand, Intel’s data center and AI (DCAI) segment revenue increased by 22% year over year to $5.1 billion. If AMD indeed manages to widen the performance gap over Intel when it launches its next-generation processors, it could become a bigger player in server CPUs with a larger revenue share. That won’t be an ideal situation for Intel, as AMD seems better positioned to capitalize on the massive investments in AI data centers.

Given that Intel’s 459% rally over the past year has made the stock extremely expensive, this semiconductor stock needs to perform better and arrest its market-share losses to justify its valuation.

Intel’s valuation clearly suggests that the stock has gotten ahead of itself

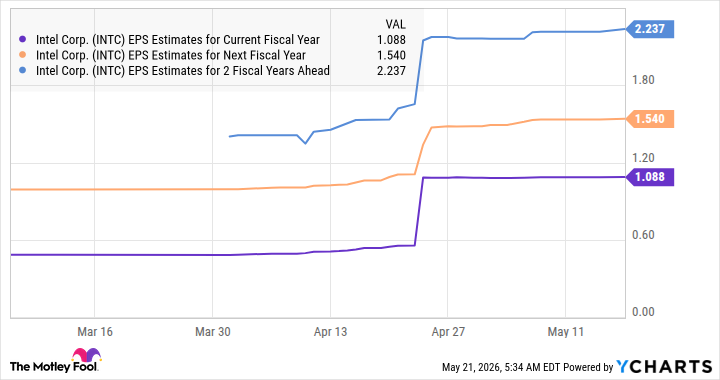

There is no denying the fact that Intel’s turnaround is translating into healthy bottom-line growth. Analysts are expecting its earnings to jump by a whopping 159% in 2026 to $1.09 per share. The good news is that Intel’s earnings growth is anticipated to accelerate over the next couple of years.

Data by YCharts

However, Intel will have to significantly exceed market expectations to deliver further gains for investors. That’s because this AI stock is now trading at a whopping 904 times earnings. The forward earnings multiple of 139, though way lower than the trailing multiple, is still quite expensive. The tech-focused Nasdaq Composite index, for comparison, has a price-to-earnings ratio of 43.

Assuming Intel commands a premium earnings multiple due to its aggressive bottom-line growth and trades at 50 times earnings after three years, its stock price could reach $112 (based on the $2.24 earnings per share estimate shown in the chart above). That represents a small downside from current levels, which is why it may be a good idea for investors to consider some underrated stocks that could surge significantly amid the AI boom.