The US markets are holding near record highs, not because conviction in de-escalation is strong, but because traders are unwilling to fade the possibility of last-minute progress or extension in US–Iran negotiations. The price action reflects hesitation rather than optimism, with risk assets supported but not advancing.

S&P 500 and NASDAQ hovered close to their peaks overnight, yet the lack of follow-through buying is telling. If markets were fully pricing a peaceful outcome, equities would be breaking decisively higher. Instead, they are consolidating gains, signaling a reluctance to commit.

This creates a distinct dynamic: not a risk-on rally, but a refusal to sell. Traders are effectively caught between rising geopolitical tension and a well-established pattern of brinkmanship followed by de-escalation. The result is positioning that is defensive rather than directional.

The credibility of deadlines has also eroded. The ceasefire, initially expected to expire on Tuesday, has effectively been extended into Wednesday following comments from US President Donald Trump. With multiple extensions already seen since mid-April, markets are increasingly treating deadlines as flexible rather than binding.

Two key assumptions underpin current resilience. First, negotiations could still take place. The reported departure of JD Vance, Jared Kushner, and Steve Witkoff for Islamabad suggests that talks remain a live possibility. This “high-level” deployment is what’s keeping the peace trade alive—markets assume Vance wouldn’t fly 14 hours if a “no-show” from Tehran was 100% certain.

Second, the possibility of another extension remains firmly in play. The pattern of repeated deadline shifts has conditioned markets to anticipate delay rather than escalation. This expectation is now embedded in positioning.

In the currency markets, Kiwi is currently the strongest one for the day so far, as boosted by increased RBNZ hike bet after Q1 CPI data. But outside of that, currencies are mixed. Loonie is the second strongest and then Dollar. Aussie is currently the worst, followed by Sterling, and then Euro.

In Asia, at the time of writing, Nikkei is up 1.04%. Hong Kong HSI is up 0.58%. China Shanghai SSE is up 0.08%. Singapore Strait Times is up 0.19%. Japan 10-year JGB yield is down -0.014 at 2.385. Overnight, DOW fell -0.01%. S&P 500 fell -0.24%. NASDAQ fell -0.26%. 10-year yield rose 0.004 to 4.250.

NZD/JPY to Resume Up Trend to 96.50 as Inflation Boosts RBNZ Rate Hike Bets

NZD/JPY is breaking higher as inflation pressures remain firm. With non-tradable prices holding up, markets are strengthening bets on an RBNZ rate hike later this year. The cross now looks ready to resume the medium term up trend towards 96.50 target. Read More.

NZ Inflation Holds at 3.1% as Non-Tradables Stay Firm, Energy Pressures Build

New Zealand inflation isn’t easing as expected. With CPI holding at 3.1% and non-tradable prices still firm, the data points to persistent domestic pressure—keeping RBNZ rate hike expectations alive. Read More.

New Zealand Business Confidence Slumps as Conflict Weighs, Inflation Pressures Rise, RBNZ July Hike Expected

New Zealand business confidence has dropped sharply as geopolitical tensions weigh on outlook—but pricing pressures are rising. With firms still lifting prices, NZIER sees the RBNZ moving toward a July rate hike. Read More.

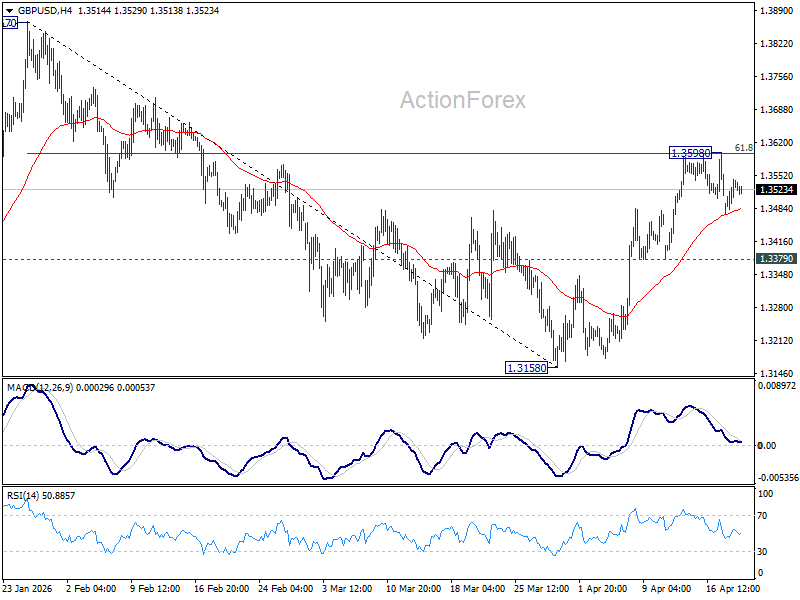

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3492; (P) 1.3519; (R1) 1.3562; More…

Range trading continues in GBP/USD and intraday bias stays neutral. Further rise is in favor as long as 1.3379 support holds. Sustained break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, firm break of 1.3379 will bring deeper fall back to 1.3158 low instead.

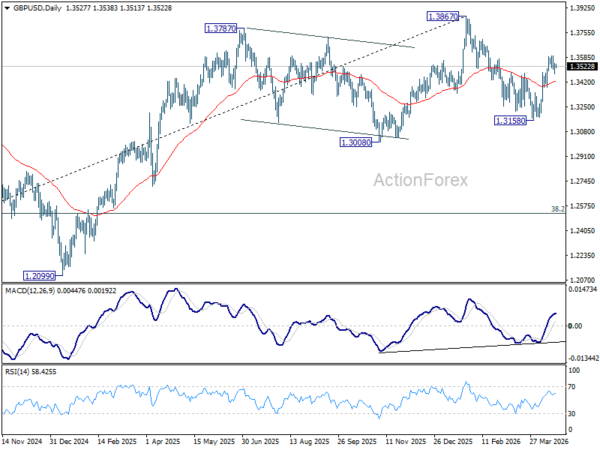

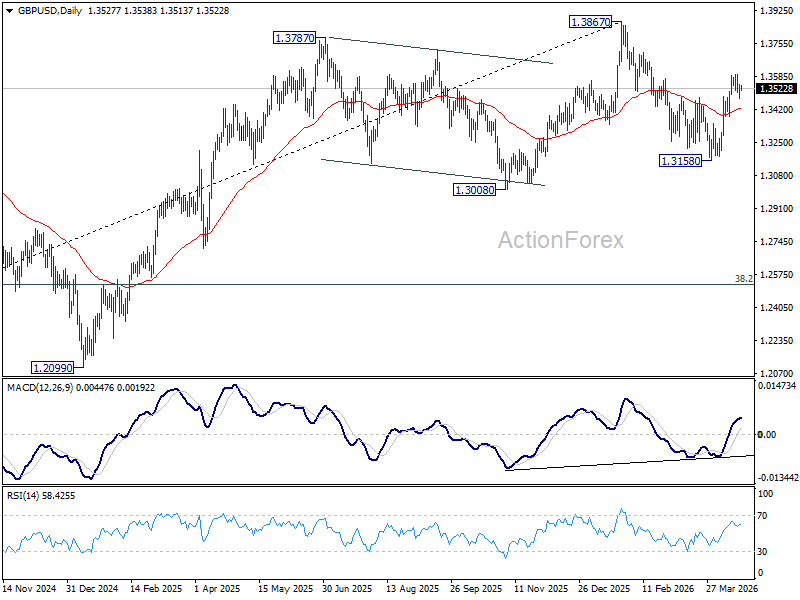

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).