Japan’s stock market is making another comeback. This time, it may finally be shedding its reputation as a value trap.

After four decades of stagnation and false dawns, the Nikkei 225 is hovering near record highs as AI enthusiasm lifts semiconductor and industrial stocks. SoftBank’s bets on OpenAI, Arm, and AI infrastructure have also made it one of Japan’s highest-profile AI plays.

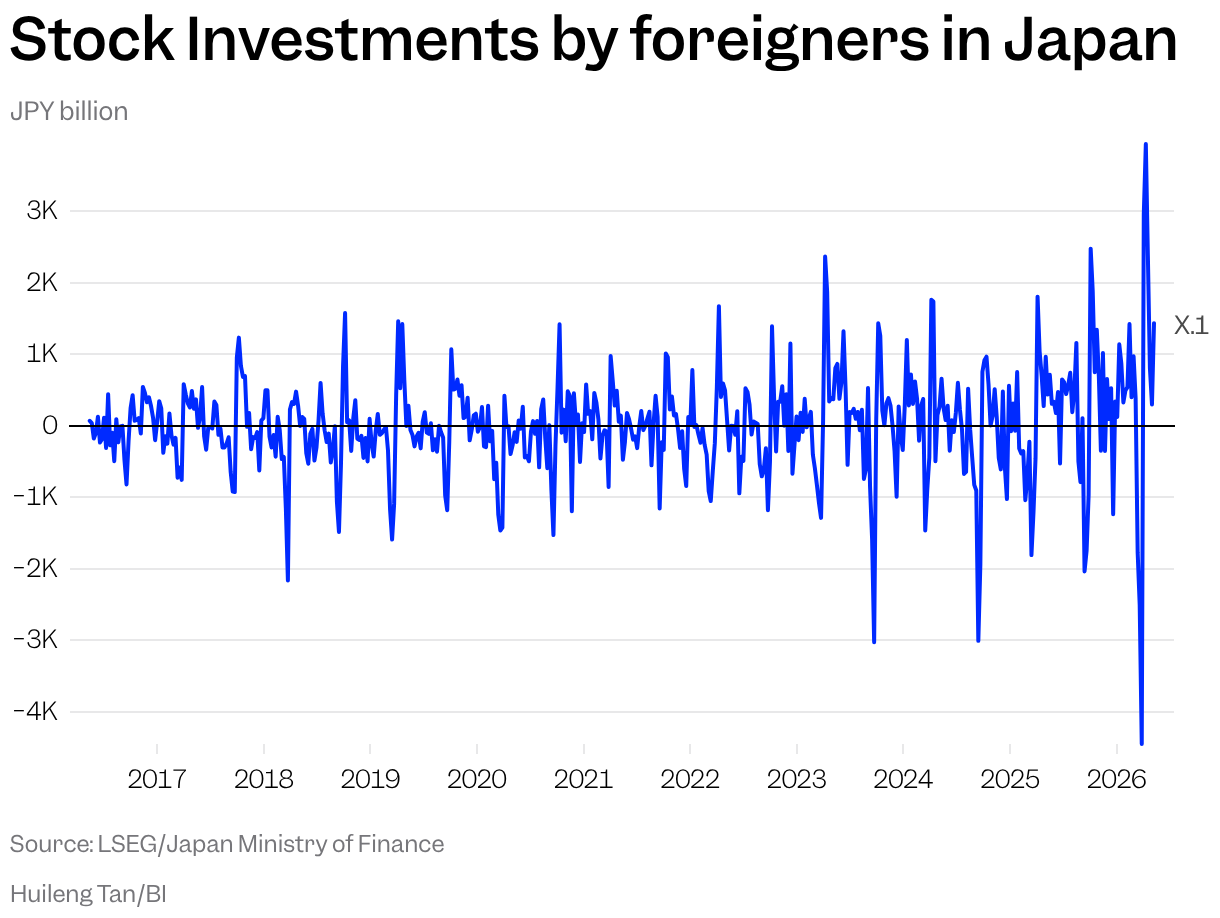

Meanwhile, Warren Buffett’s Berkshire Hathaway is doubling down on Japanese trading houses, while foreign investors are pouring billions into a market many had long written off.

On Monday, Japan’s benchmark Nikkei 225 hit the 67,000 level for the first time. The index is up about 30% this year.

The improving sentiment is increasingly being backed by the economy itself. Japan’s real GDP grew at an annualized rate of 2.1% in the first quarter, beating expectations and accelerating from the previous quarter. Inflation has stayed near or above the Bank of Japan’s 2% target for much of the past two years.

“As the economy exits decades of deflation and we get positive real interest rates filtering through into the economy, and private consumption picking up as a result of higher wages, that should bode well for the overall economy,” Kei Okamura, a portfolio manager on the Japanese equities team at Neuberger Berman, told Business Insider.

Foreign investors are pouring in. Ministry of Finance data show overseas investors have sharply increased trading in Japanese equities since 2024, as excitement builds around the country’s reflation story, corporate reforms, and AI-driven industrial revival.

The rally has not been smooth. After surging to fresh highs in early 2024, the Nikkei suffered a sharp selloff that summer as investors unwound crowded yen-funded trades.

But the market rebounded as investors returned to Japan’s improving profits, stronger wage growth, and AI-linked industrial story.

Bank of America strategists have also raised their year-end forecasts for Japanese equities, citing the AI boom and Japan’s role in supplying semiconductor equipment, materials, and components to the global AI supply chain. The firm expects the Topix to reach 4,200 and the Nikkei 225 to hit 67,000 by year-end.

BofA said profit growth was especially strong in electronics, machinery, banks, construction, and real estate — sectors tied to AI infrastructure, automation, higher rates, and Japan’s broader economic revival.

“Japanese equities have multilayered catalysts,” wrote the bank’s equity strategists in a May note.

AI is reviving Japan’s industrial economy

Like in the US and South Korea, AI-linked stocks have been among the biggest drivers of Japan’s market rally.

The new Japan story is not just about AI-linked chip stocks.

Shares of semiconductor-equipment and chip-testing firms such as Tokyo Electron, Advantest, Disco, and Screen Holdings have surged alongside growing demand for data centers, computing infrastructure, and factory automation.

Even unlikely names in traditional industries — from toilet maker Toto to seasoning giant Ajinomoto — have benefited as investors search for second-order winners from the AI boom and Japan’s broader economic revival.

Okamura argues investors are still underestimating the broader industrial ripple effects of AI.

“Japan’s edge in generative AI is going to be the physical AI part,” he said. “How do we integrate AI into manufacturing, into the value-creation process? That’s where Japan’s strengths are.”

That includes companies tied to wiring, optics, electrical grids, robotics, and construction.

Toyota’s push into robotics and Sony’s partnership with TSMC on imaging sensors are examples of how Japanese firms are positioning themselves for the next phase of AI, he said.

Financial companies are also part of the story because regional banks and insurers could benefit as the Bank of Japan gradually normalizes policy after years of ultra-low rates, Okamura said.

That reflects Neuberger’s view that Japan’s opportunity extends beyond obvious AI winners into the broader industrial backbone supporting the technology boom.

“We’re talking about companies taking that excess capital and reinvesting it for growth over the med to long term,” Okamura said.

Why investors think this time is different

In recent years, the bullish case for Japan has centered on corporate-governance reforms and improving shareholder returns.

A weak yen has also fueled the rally by boosting exporters’ overseas earnings and making Japanese assets cheaper for foreign investors.

Now, investors increasingly believe something bigger is happening: Japan is finally emerging from decades of deflation.

Rising share prices may also be feeding into the real economy, according to Goldman Sachs.

In a recent May report, the bank estimated that a 10% rise in equity prices boosts Japan’s consumption growth by about 0.3 percentage points, with the biggest effects in higher-value goods and services such as travel, dining, clothing, and beauty spending.

That matters because Japan’s stock market is no longer sitting outside the economy. Rising share prices may now be helping support spending, investment, and corporate confidence.

Asset Management One International, a Mizuho subsidiary, estimates the expected return on equity for Japanese companies will rise to 10.5% this year, well above the 15-year average of just over 8%.

The firm said governance reforms, stronger pricing power, and higher interest rates — which help banks and financial companies — suggest Japan may be entering a longer-term structural shift rather than another short-lived rally.

Even after the run-up, Japanese stocks still trade at significantly lower valuations than US equities, suggesting there could still be room for further gains if profitability continues improving.

“This process should help to close the still significant valuation gap between Japanese stocks and the US and European markets,” said Oleg Kapinos, head of global distribution strategy at Asset Management One International, in a May note.