Contents

Importance of the Space Industry and the United States’ Role. 2

How Innovative Is China’s Space Industry? 5

Government Policies Supporting China’s Space Industry 17

The space industry uses rockets to place spacecraft into orbit around the Earth. These spacecraft, such as satellites and crewed space stations, provide services and capabilities in space and back on Earth. There are communications satellites for television, radio broadcasting, and broadband Internet service. Other satellites are used for observing Earth and navigation services.

Space stations, such as the International Space Station (ISS), are used to conduct science experiments in a microgravity environment. Many spacecraft provide capabilities for both civilian and military purposes.

Countries with the most innovative capabilities can project both hard power through the threat of space-based offensive and defensive military technology and soft power through opportunities for collaborative space operations. The space industry also generates “spinoff” technologies that advance other industries such as communications and healthcare.[1]

The International Space Station (ISS)[2]

Two space races define the history of the global space economy: one between the United States and Russia in the second half of the 20th century, and the other between the United States and China today. The first space race began in 1956 when both the United States and Russia announced plans to launch satellites into space. Russia took an early advantage in the race when it launched the Sputnik I satellite in 1957. But Russia lost in the late 1960s when Apollo 11 took National Aeronautics and Space Administration (NASA) astronauts around the moon.[3]

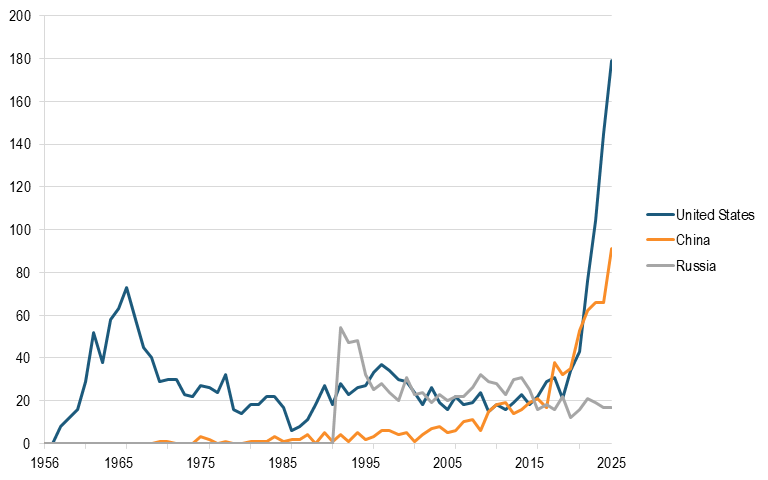

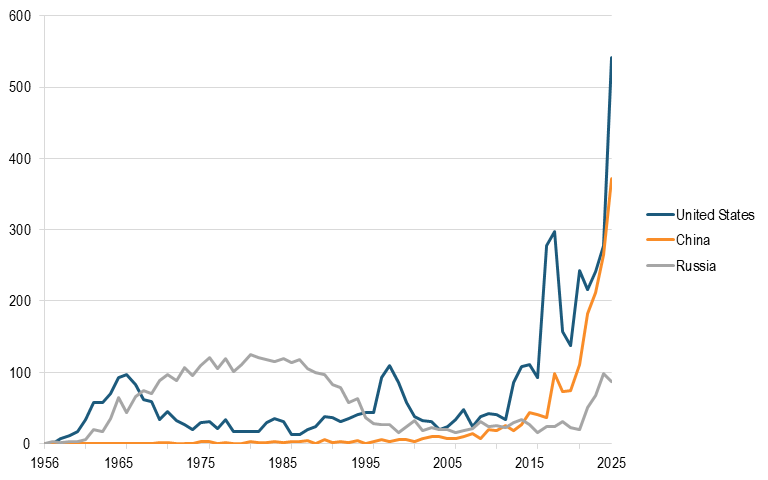

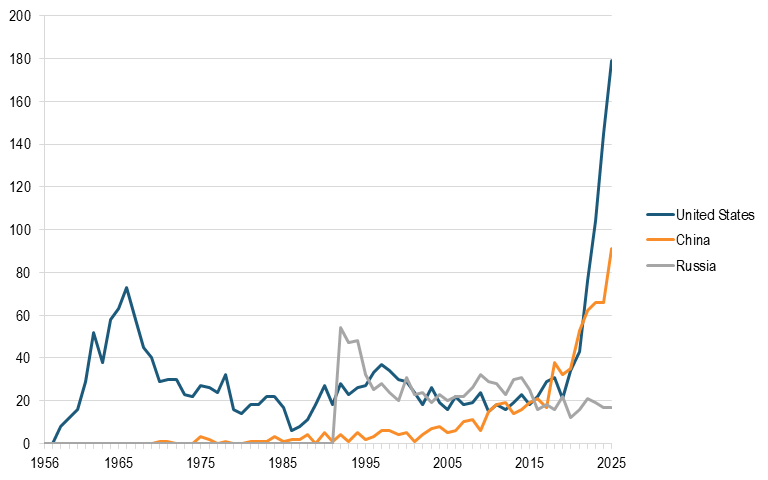

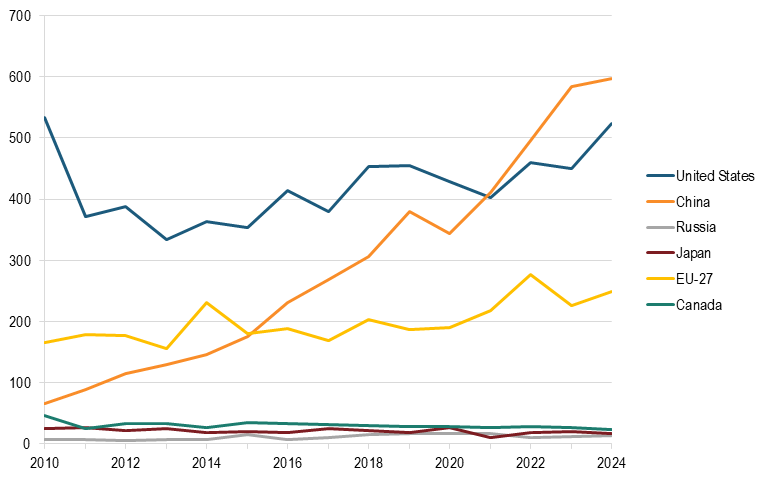

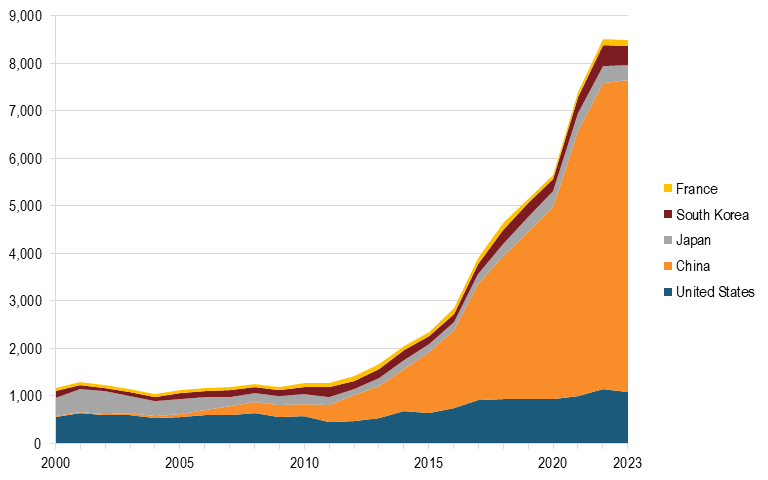

The United States has been the uncontested leader of the global space economy since the end of that first space race. However, China has surpassed Russia in the number of annual launches, total annual tonnage launched, and number of satellites placed into orbit. Figure 1, figure 2, and figure 3 show these metrics for the United States, China, and Russia from the beginning of the first space race through the end of 2025.[4] In 2025 alone, there were 4,409 satellites launched across all orbits, weighing a total of 3,194 tons, on 321 total launches across the entire global space industry.[5]

Figure 1: Annual launches, 1956–2025

Figure 2: Annual number of satellites placed into orbit, 1956–2025

Figure 3: Annual payload tonnage, 1956–2025

Today, the global space industry is on a significant growth trajectory. The space consulting firm Novaspace projects that the industry will expand from $626.4 billion in 2025 to $1.01 trillion by 2034.[6] The primary drivers of this growth are increasing demand for satellite services, higher launch frequency (launch cadence), and the greater carrying capacity of modern rockets.

The global space market features many governments and companies that have satellites they want to deploy, but far fewer launch providers to do so.[7] The result of this imbalance is a seller’s market in which having the most advanced launch capabilities is a key factor for leadership in the global space economy.

Aside from launch capacity, there is also growing global demand for satellite services, especially satellite Internet. Starlink, the world’s leading Low-Earth Orbit (LEO) broadband provider, gained more than 4.6 million new subscribers in 2025.[8] Plus, there are cutting-edge satellite technologies, including orbital data centers, that are still in the early stages of development.[9]

The United States is the global leader in space innovation because it is the only country with operational reusable rockets, it has the most advanced LEO broadband satellite constellations, and it is the lead partner of the ISS. SpaceX’s Falcon 9 is the most advanced orbital-class reusable rocket and can get payloads into space at a fraction of the cost of traditional, single-use rockets.[10] Blue Origin’s New Shepard suborbital rocket is also reusable and has flown several suborbital tourism flights.[11] The United States is also home to two of the most advanced LEO broadband constellations: SpaceX’s Starlink and Amazon’s Leo.[12]

Despite lacking several key technologies that maintain America’s advantage, the Chinese Communist Party (CCP) is pouring vast resources into building a commercial space industry it believes will surpass the United States in space capabilities by 2030. This report analyzes the innovation capacity of Chinese space companies and displays how U.S. complacency could allow China to become the most innovative spacefaring nation.

Mao Zedong first conceived of China’s space industry in 1958 with his “Two Bombs, One Satellite” program, which set an official goal for China to build an atomic bomb, a hydrogen bomb, and a satellite.[13] China’s space industry initially grew quite slowly, only launching a handful of satellites before the turn of the century.[14] However, China joined the ranks of the United States and Russia in 2003 when it successfully launched a crew into orbit, and has since significantly expanded its space industry.[15]

The development of China’s space capabilities has primarily been led by state-owned enterprises (SOEs), but in 2014, the CCP invited commercial companies and private investment to participate in the sector for the first time. This change is driving the rapid growth of China’s space sector, which now has more than 500 private companies.[16] The CCP’s oversight of all major economic, technical, and academic organizations allows China to leverage the whole of society, rather than just the whole of government or private sector alone, to develop the industry and achieve its space ambitions.[17]

In addition to the whole-of-society approach, China’s military, the People’s Liberation Army (PLA), benefits from a policy of Military-Civil Fusion (MCF). Space capabilities are dual-use, meaning they have both military and civilian applications. But, for Chinese space innovation, MCF goes beyond the traditional understanding of a dual-use technology. MCF dictates that the PLA can nationalize commercial technologies and capabilities without the acquisition processes that constrain U.S. military access to commercial space innovation.[18]

Today, China has a robust space industry that is closing the innovation gap with the United States. The large SOEs that remain the foundation of China’s industry have splintered into various private entities. Together, these companies comprise a vertically integrated manufacturing base that continues to scale up production of satellites and rockets. Simultaneously, the CCP spurs growth by creating a regulatory environment that prioritizes the rapid development of space innovation.

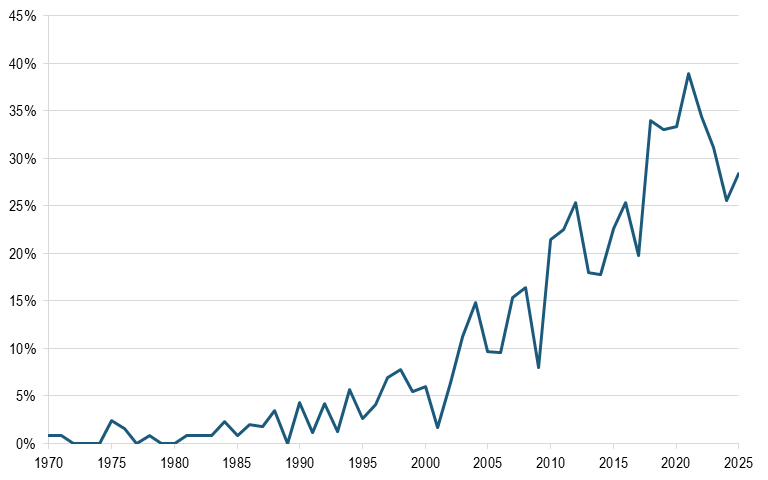

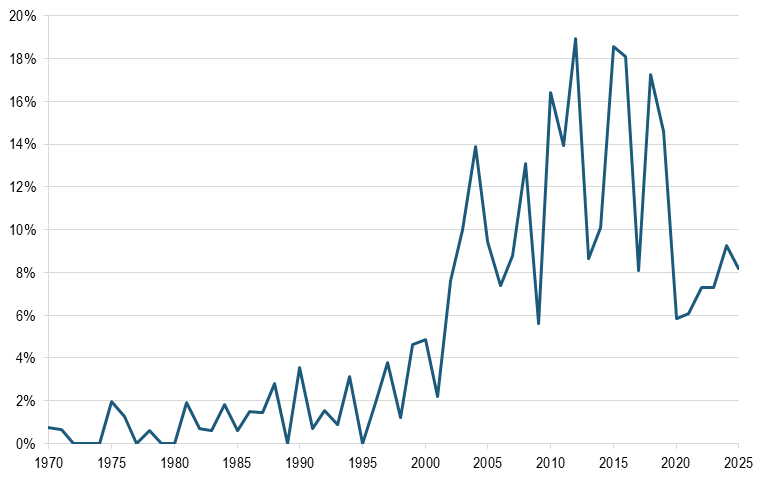

China’s annual share of total rocket launches has grown, albeit inconsistently, since its first launch in 1970. However, China’s share declined in 2025, accounting for only 28 percent of launches, as shown in figure 4.[19] China’s share of all satellites launched annually has remained around 10 percent, and it accounted for just 8 percent of all satellites in 2025, as shown in figure 5.[20] These statistics reflect the increasing launch cadence and capacity of other nations, including the United States, as well as emerging space powers such as Europe and India.[21]

Figure 4: China’s annual share of all rocket launches reaching orbit, 1970–2025

Figure 5: China’s annual share of all satellites placed into orbit, 1970–2025

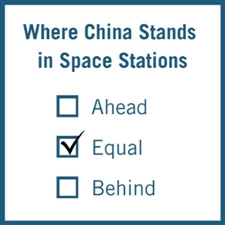

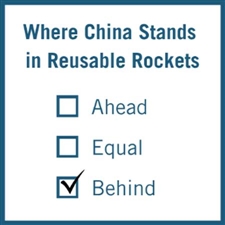

While China lacks advanced LEO broadband satellite constellations and fully operational reusable rockets, China does have numerous innovative satellite systems, its own space station, and counter-space military capabilities.

To better understand China’s industry, this section examines space industry subsectors and assesses whether China is leading the United States, is equal, or is behind in each.

Table 1: Assessments of U.S. and Chinese competitive positions in space industry subsectors

|

Subsector |

Who Is Leading? |

|

Low-Earth Orbit Broadband |

● United States |

|

Positioning, Navigation, and Timing |

● China |

|

Remote Sensing and Satellite Imaging |

● China |

|

Space Stations |

● Equal |

|

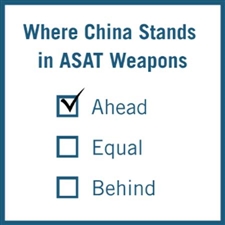

Antisatellite Capabilities |

● China |

|

Reusable Rockets |

● United States |

Low-Earth Orbit Broadband

LEO satellite broadband connectivity is expanding home and mobile broadband Internet coverage by connecting remote areas.[22] This expansion includes partnerships with commercial airlines to provide in-flight Wi-Fi, as well as direct-to-device service that connects smartphones directly to satellite Internet rather than relying on terrestrial mobile networks.[23] Furthermore, satellite Internet will play an increasingly important role in reaching previously unconnected countries in the Global South.[24]

LEO satellite broadband connectivity is expanding home and mobile broadband Internet coverage by connecting remote areas.[22] This expansion includes partnerships with commercial airlines to provide in-flight Wi-Fi, as well as direct-to-device service that connects smartphones directly to satellite Internet rather than relying on terrestrial mobile networks.[23] Furthermore, satellite Internet will play an increasingly important role in reaching previously unconnected countries in the Global South.[24]

China is less innovative than the United States in LEO broadband satellites, but has ambitious plans to deploy two satellite constellations, Qianfan and Guowang, totaling around 28,000 satellites by 2030.[25] However, it is unlikely that China will achieve this goal due to launch constraints inherent in single-use rockets. In addition, early launches of both constellations saw multiple satellites fail to reach their intended orbits.[26] Until China achieves a reusable rocket, LEO broadband constellations will continue to trail American competitors.

Positioning, Navigation, and Timing

Position, Navigation, and Timing (PNT) satellites are critical for industries such as maritime navigation, supply chain management, and global finance.[27] A 2019 study from RTI, on behalf of the National Institute of Standards and Technology, shows that America’s PNT satellite constellation, the Global Positioning System (GPS), had produced $1.4 trillion in U.S. economic benefits since its establishment in 1980 through 2017.[28] PNT satellites are also vital for coordinating military operations, making PNT one of the most important dual-use space technologies today.[29]

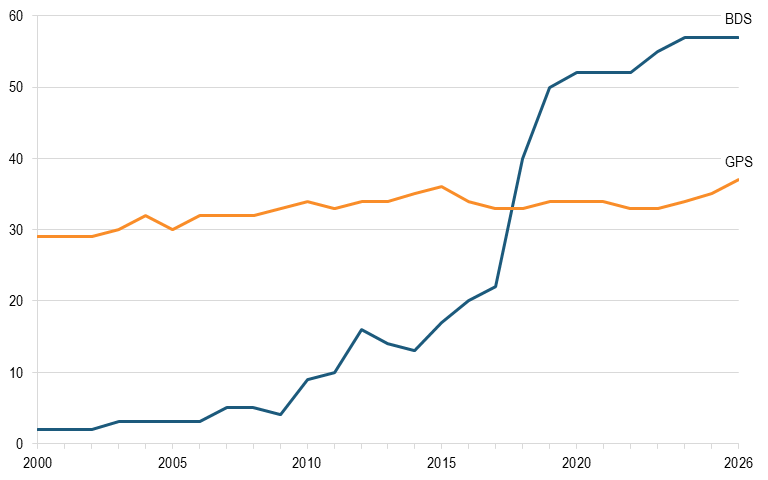

China’s BeiDou Navigation Satellite System (BDS) is a PNT system whose growth from 2000 through 2026 is charted in figure 6. BDS is more innovative than other PNT systems, such as Europe’s Galileo, Russia’s GLONASS, and GPS, in several ways.[30]

China’s BeiDou Navigation Satellite System (BDS) is a PNT system whose growth from 2000 through 2026 is charted in figure 6. BDS is more innovative than other PNT systems, such as Europe’s Galileo, Russia’s GLONASS, and GPS, in several ways.[30]

First, BDS has 50 active satellites in orbit in a multi-orbit system with satellites in Medium-Earth Orbit (MEO), Geosynchronous Orbit (GEO), and inclined geosynchronous orbit. Additionally, BDS uses intersatellite links to improve management of the constellation and individual satellites. Both factors provide BDS with more PNT data, which improves accuracy, especially in regions underserved by GPS, such as Africa and Asia.[31] GPS has only 37 satellites, all operating in MEO, and relies entirely on ground-to-space communications, which is slower and less accurate.[32]

Figure 6: Number of operational BDS and GPS satellites, 2000–2026

Remote Sensing and Satellite Imaging

Earth Observation (EO) satellites provide critical data for military operations and serve civilian purposes such as precision agriculture and disaster prevention. High-quality pictures and videos of large areas of Earth allow farmers to more easily track crop yields and help first responders map the path of natural disasters to plan evacuations.[33] Militaries use EO for both intelligence gathering and coordinating battlefield operations.[34]

Earth Observation (EO) satellites provide critical data for military operations and serve civilian purposes such as precision agriculture and disaster prevention. High-quality pictures and videos of large areas of Earth allow farmers to more easily track crop yields and help first responders map the path of natural disasters to plan evacuations.[33] Militaries use EO for both intelligence gathering and coordinating battlefield operations.[34]

The United States was the leader in EO for a long time but is now behind China in several aspects including visible, radar, and hyperspectral imaging. Visible imaging uses light that is visible to the human eye, whereas radar imaging uses microwaves, and hyperspectral imaging uses the entire electromagnetic spectrum.[35] China is ahead in EO because it places a greater priority on ubiquitous observation, and it has more technologically advanced EO satellites.[36]

China has two EO systems: a government system and a private system. Subsidiaries of China’s largest space SOE, the China Aerospace Science and Technology Corporation (CASC), including the Shanghai Academy of Spaceflight Technology and the China Academy of Space Technology, have developed and operate the Yaogan satellite system for the PLA.[37] Meanwhile, the commercial firm Chang Guang Satellite Technology owns and operates the Jilin-1 constellation.[38] These two systems gather data that provides China with one of the most comprehensive intelligence, surveillance, and reconnaissance operations in the world.[39] China uses EO primarily to conduct near-real-time monitoring of the Pacific and Indian Oceans as well as Taiwan and mainland China.[40]

The Yaogan satellites are unlike other EO satellites because they are placed in peculiar orbits. Most EO satellites operate in LEO because closer proximity to Earth improves image quality and sensing capabilities. However, the Yaogan-41 satellite operates in GEO, and two Yaogan-50 satellites launched in early 2026 both operate in a “retrograde orbit,” meaning they move in the opposite direction of the Earth’s rotation.[41]

China likely put Yaogan-41 into GEO to provide continuous monitoring of a single large area, whereas LEO satellites only offer fleeting coverage.[42] The reason for placing the Yaogan-50 satellites in retrograde orbit is unclear, but additional data on the satellites’ relative positioning should provide more insight.[43] The PLA uses multiple sensor types on these satellites for military reconnaissance. The satellites can track objects as small as a car moving through the Indo-Pacific region.[44]

Chang Guang Satellite Technology is an offshoot of the Chinese Academy of Sciences and began operating the Jilin-1 system in 2015.[45] While the company maintains that the satellites serve civilian EO needs, MCF means that the government can access Jilin-1 data. The number of operational Jilin-1 satellites, as shown in figure 7, spiked sharply in 2022, driven by China’s push to expand its EO capabilities in response to concerns about private satellite companies capturing images of Russian troops during the invasion of Ukraine.[46]

Figure 7: Number of operational Jilin-1 satellites, 2015–2026

Space Stations

The U.S. role as the lead partner of the ISS makes it the most sought-after collaborator for space-based science and technology projects, which enhances diplomacy. The ISS is a research facility that has been orbiting Earth since 2000 and is designed, built, and operated by the United States alongside Russia, Canada, Japan, and the European Union. The station hosts a U.S. National Laboratory, which continues to make significant scientific contributions across numerous fields. Researchers on the ISS have produced about 4,000 research papers and contributed to treatments for cancer, Alzheimer’s, and heart disease.[47] Navigation, communication, and space suit technologies developed on the ISS will feature on crewed missions to the Moon and Mars.[48]

The U.S. role as the lead partner of the ISS makes it the most sought-after collaborator for space-based science and technology projects, which enhances diplomacy. The ISS is a research facility that has been orbiting Earth since 2000 and is designed, built, and operated by the United States alongside Russia, Canada, Japan, and the European Union. The station hosts a U.S. National Laboratory, which continues to make significant scientific contributions across numerous fields. Researchers on the ISS have produced about 4,000 research papers and contributed to treatments for cancer, Alzheimer’s, and heart disease.[47] Navigation, communication, and space suit technologies developed on the ISS will feature on crewed missions to the Moon and Mars.[48]

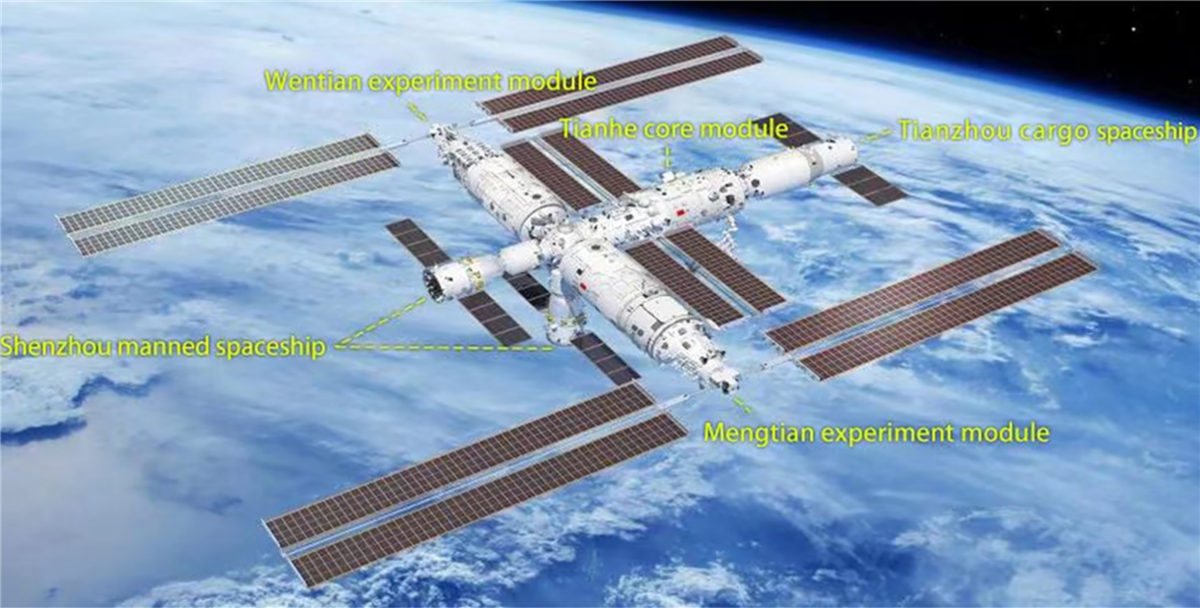

In 2011, Congress included an amendment to the annual appropriations bill, known as the Wolf Amendment, that forbade U.S. space agencies from collaborating with China on programs such as the ISS due to concerns about China’s Space Agency’s connections with the PLA.[49] In response, China began development of its own space station, named Tiangong (“Heavenly Place”), which began operations in 2022.[50] The three-module station now continuously hosts taikonauts (Chinese astronauts) and is also home to two scientific laboratories for experimentation in microgravity.

Figure 8: Rendering of the Tiangong Space Station by China’s Space Agency[51]

China developed Tiangong at a remarkable speed, indicating that China can manufacture space technology quickly and at scale. China benefits from building on existing U.S. and international technologies, reducing the need to develop capabilities entirely from scratch. But, even so, as China continues to develop its own version of foreign space technologies, it will also improve domestic innovation capabilities.

Antisatellite Capabilities

U.S. military intelligence suggests that the PLA aims to use counterspace operations to deter foreign military action and has been developing antisatellite (ASAT) ground and space weapons.[52] ASAT ground technologies include missiles that can shoot down spacecraft in LEO, as well as weapons that can jam, spoof, or dazzle satellites. Jamming uses radio frequency signals to interfere with satellite communications.[53] Spoofing is when an attacker sends false data to a satellite, and dazzling involves beaming a high-powered laser into a satellite’s optical center, damaging critical components and disrupting functionality.[54]

U.S. military intelligence suggests that the PLA aims to use counterspace operations to deter foreign military action and has been developing antisatellite (ASAT) ground and space weapons.[52] ASAT ground technologies include missiles that can shoot down spacecraft in LEO, as well as weapons that can jam, spoof, or dazzle satellites. Jamming uses radio frequency signals to interfere with satellite communications.[53] Spoofing is when an attacker sends false data to a satellite, and dazzling involves beaming a high-powered laser into a satellite’s optical center, damaging critical components and disrupting functionality.[54]

China is also developing satellites capable of rendezvous and proximity operations that could enable kinetic conflict in orbit.[55] Space Force refers to these maneuvers as “dogfighting in space,” and, combined with robotic arms that China is developing on Tiangong, it appears that China is testing the ability to have a satellite grab another one and damage it or drag it out of orbit.[56] Space Force claims that it will soon begin the development of similar technologies for warfighting in space.[57]

Reusable Rockets

Reusable rockets are those that launch, deliver their payload to space, and perform a controlled landing so that the boosters can be used again for subsequent launches.[58] Reusable rockets have a profound impact on the space industry because they massively cut launch costs.[59]

China’s most significant challenge in space innovation is the lack of an operational reusable rocket. There are numerous launch companies in China, many of which are working on building a reusable rocket.[60] Some of these companies have made progress on specific rocket components, but none have completed a flawless test of the fully integrated system.[61]

China’s most significant challenge in space innovation is the lack of an operational reusable rocket. There are numerous launch companies in China, many of which are working on building a reusable rocket.[60] Some of these companies have made progress on specific rocket components, but none have completed a flawless test of the fully integrated system.[61]

Since China’s commercial space industry was established in 2014, the launch subsector has typically had the most funding, but it was overtaken by satellite operators and manufacturers in 2024.[62] Launch companies raised more in 2024 than in 2023, but their proportion of all space sector funding went from 45 to 26 percent due to an even larger increase in funding for satellite operators and manufacturers.[63] This change suggests that, while reusable rockets remain a core focus of the CCP, priorities for China’s commercial space sector are shifting.

As part of this analysis, ITIF examined scientific publications on space technologies and aerospace engineering, and also space technology patents. The data shows that China has significantly increased its research and development (R&D) efforts over the last 10 years, though some experts question the validity of China’s patents.

Scientific Publications

Data from the Australian Strategic Policy Institute (ASPI) shows that China has a high rating for technology monopoly risk (TMR) in several technologies categorized as “defense, space, robotics, and transportation.”[64] This designation means that China is publishing “more than three times as much high-impact research as its nearest competitor” and is “home to eight or more of the top 10 institutions” in space technology.[65] The designation also means that other countries will have a difficult time closing the R&D gap in those five technologies.[66]

China’s leadership in EO and PNT is reflected in scientific publication data. ASPI data from 2023 shows that China had the highest percentage of papers in the top 10 percent of highly cited papers across three space technologies.[67] This leadership includes 49 percent on EO satellites and 36 percent on PNT satellites.[68] China also has a high TMR rating for PNT, which means it publishes far more high-impact research on PNT technology than does any other nation.[69]

Furthermore, data from the Organization for Economic Cooperation and Development (OECD) on the most-cited aerospace engineering publications (see figure 9) also displays China’s leadership in space R&D.[70] China has maintained consistent growth in the number of annual top-cited publications since 2020 and surpassed the United States in 2022. China produced 597 aerospace engineering publications in 2024.[71]

Figure 9: Number of aerospace engineering publications in the top 10 percent of most-cited publications

Patents

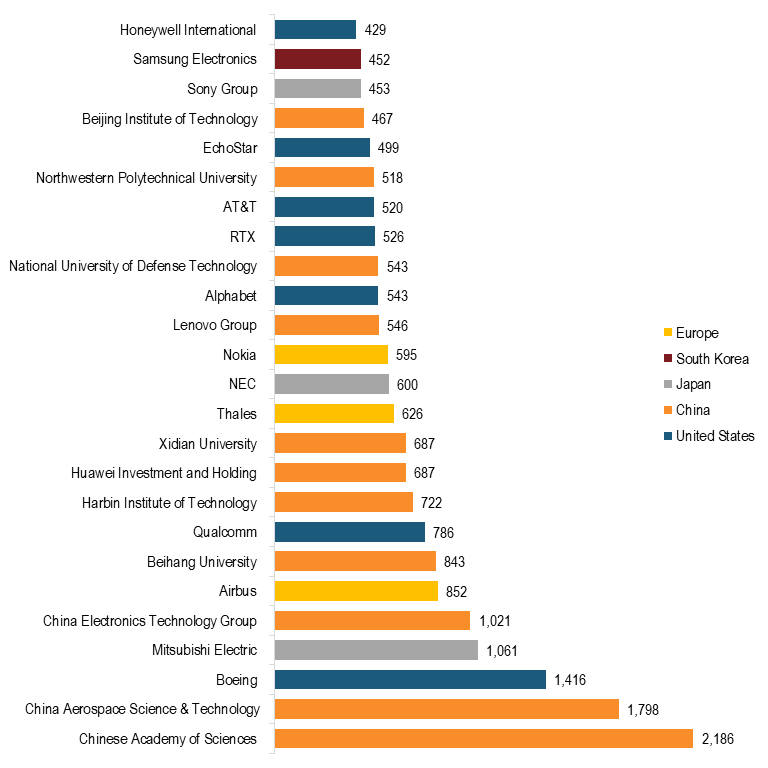

Patents are indicative of a country’s or company’s innovation. China has significantly more space technology patents than the rest of the world does. According to the World IP Organization (WIPO), from 2000 through 2023, China increased its annual number of patent family publications related to space from 15 to about 6,600.[72] Among the top five countries with the most space patents, China has more patent family publications than do the other countries combined, as figure 10 illustrates.[73]

WIPO data also shows that 11 of the top 25 space technology patent owners are from China, as shown in figure 11.[74] Both of the top two patent holders, the Chinese Academy of Sciences and CASC, are SOEs, indicating that government-led space innovation still dominates in China, despite the rapid growth of the commercial sector.

Although China leads in patent volume, most of its patents are of questionable value. Around 95 percent of the space patents China filed from 2000 through 2023 were only submitted domestically, meaning that most of China’s space patents lack any global influence.[75] China’s high patent volume does not necessarily indicate global innovation leadership, especially if many of the patents are of lower quality than those filed elsewhere.[76]

Figure 10: Countries with the top five most space technology patent publications

Figure 11: Companies with the most space technology patents

Taken together, the growth in the number of its scientific publications and patents in space technologies suggests that China is rapidly enhancing its R&D and innovation capabilities in space. The United States must recognize that it cannot maintain its current levels of innovation and expect to remain the global leader in space.

This section highlights three leading Chinese space companies and their contributions to China’s space innovation.

CALT was established on November 16, 1957, as part of CASC, and has since been made its subsidiary.[77] CALT is China’s largest research and production base for missiles and launch vehicles, and it plays a vital role in China’s commercial space industry.[78] CALT develops and operates the Long March rocket series, which the CCP uses for most of its space missions.[79]

CALT has a large footprint in the industry. As of 2023, CALT had 11 “centrally administered public institutions,” 3 SOEs, 5 wholly owned subsidiaries, and 9 holding companies.[80] It employed 31,000 people, had total assets of approximately ¥147.3 billion ($21 billion), and occupied 800 hectares of property.[81] CALT primarily operates in Beijing with support from additional locations in Hebei, Tianjin, Shanxi, Shandong, Hunan, and Hainan.[82]

CALT is continuously improving its Long March rockets. The company successfully recovered the first stage and crew module during a February 2026 low-altitude test of the abort system on a Long March 10 rocket, which will be used in China’s mission to land on the moon.[83] This achievement advances China’s lunar mission and progress toward successfully developing its first mission-ready reusable rocket.

LandSpace

LandSpace was established in 2015 and is one of the earliest private commercial rocket companies in China.[84] It is leading Chinese innovation in reusable rocket technology with its Zhuque rocket series, which aims to rival SpaceX’s Falcon 9.[85] The company is also working on developing a heavy-lift launch engine for future missions, which has made it a favored launch partner for both the government and commercial firms.[86]

LandSpace’s headquarters are in Beijing, and the company had a workforce of 700 to 1,000 employees as of early 2026. A Q3 2025 audit shows the company’s total assets are ¥6.9 billion ($969 million).[87] Following a recent Series D+ funding round, LandSpace’s post-money valuation was ¥19 billion ($2.67 billion), giving it Unicorn status (meaning it’s valued at over $1 billion) ahead of its IPO on the Shanghai Stock Exchange.[88] This information shows that LandSpace is a valuable company and one of China’s most innovative rocket developers, with high potential for continual growth after going public.

However, LandSpace has not yet successfully demonstrated reusability of its Zhuque-3 rocket. The most recent test, and China’s first attempt at landing an orbital booster, took place in December 2025.[89] The second stage of the rocket successfully entered its planned orbit and completed a re-ignition test, but the rocket’s first stage did not land where intended and cannot be reused. LandSpace plans to test Zhuque-3 again in Q2 2026, but the recent failure shows that it is still behind American companies in reusable rocket development.

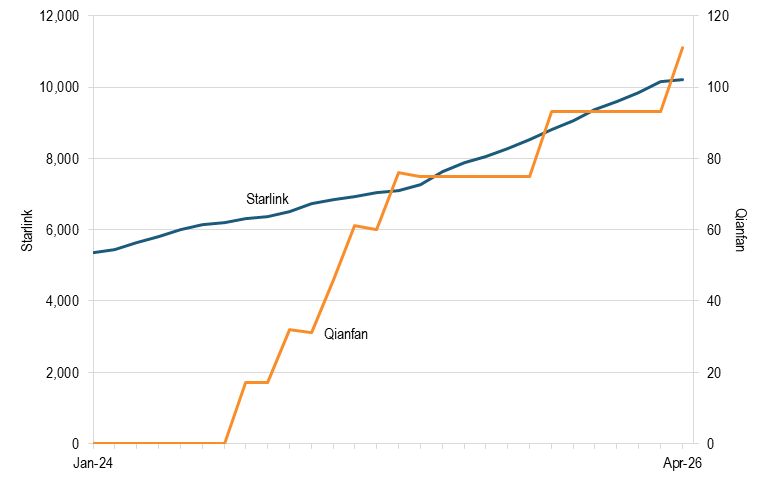

SSST is in the process of deploying China’s largest LEO broadband constellation named Qianfan (Thousand Sails) or Spacesail.[90] Qianfan is China’s answer to Starlink and central to China’s aims to expand operations to countries in the Global South.[91] SSST is negotiating with about 30 countries to establish commercial arrangements for satellite connectivity.[92]

SSST was founded in 2018 and is backed by Shanghai’s municipal government.[93] Today, it is one of the most well-funded private satellite companies in China. In 2024, SSST completed a ¥6.7 billion ($918 million) Series A financing round, the largest single-round financing amount for a Chinese satellite company.[94] Despite strong initial investment, SSST faces significant hurdles to becoming a global competitor to other LEO broadband companies.

Figure 12: Number of Operational Qianfan and Starlink Satellites, January 2024–April 2026

The main hindrance to SSST’s growth is China’s lack of launch capacity. The low launch cadence for Chinese satellite companies makes it hard to scale constellations, limiting the reach and quality of broadband service. The data in figure 12 shows the slow, and sometimes stagnant, growth of the Qianfan constellation, which is similar to the growth trajectories of other Chinese satellite companies, as seen in figure 6 and figure 7.[95] The comparatively consistent growth of Starlink’s constellation from 2024 through early 2026 shows the impact of SpaceX launching Starlink satellites on its Falcon 9 reusable rocket, which has a much higher launch cadence than the single-use rockets Chinese companies such as SSST use.

The CCP first conceptualized a commercial space industry in a policy directive known as “Document 60” in 2014.[96] This directive opened the space sector to private companies and investment for commercial remote sensing-data satellites, launch infrastructure, satellite navigation ground infrastructure, and government procurement capabilities.[97]

The next key document was a 10-year civilian space infrastructure development plan published in 2015.[98] The ongoing plan lays out specific milestones for building the infrastructure to enable greater use of “remote sensing, communications, broadcasting, navigation, positioning, and other products and services.”[99] The plan analyzes the most innovative satellite operations globally and lays out a clear path to develop the necessary space and ground infrastructure to achieve those capabilities.

Every five years since 2000, China’s State Council has released a white paper on the country’s space activities, and the 2022 white paper highlights another notable shift for China’s space sector.[100] A former director of the National Space Science Center of the Chinese Academy of Sciences has said that the white paper highlights expanding commercial access to “major scientific research facilities and equipment” and greater collaboration on R&D of major engineering projects.[101] This change is notable because most major government space projects to that point had been carried out using government-developed Long March rockets.[102]

The white paper also outlines China’s goal of expanding the space industry to include space tourism and space biopharmaceuticals, enabled by the Tiangong space station, which became fully operational the same year this white paper was released.

The second most significant policy for China’s space industry is the National Space and Science Medium- and Long-Term Development Plan (25-Year Plan), released in 2024.[103] The plan establishes goals for China’s space industry from 2024 through 2050, broken out into three phases:

1. The first phase focuses on several projects already in development, including a first crewed lunar mission by 2030, new operations on the Tiangong space station, and deployment of a Hubble-class telescope.[104] This phase also features more ambitious scientific projects such as placing a satellite in the Sun’s orbit, detecting dark matter particles, and performing long-term search missions for habitable exoplanets.[105]

2. The second phase runs from 2028 to 2035 and includes several large-scale missions. The most notable of these is the establishment of the International Lunar Research Station (ILRS) on the surface of the Moon.[106] The ILRS is “a scalable and maintainable comprehensive scientific experiment facility” that will serve as the off-planet hub for “long-term exploration and development of the universe.”[107] China is looking to have at least 50 other countries join the mission and contribute to the construction of ILRS, and 11, including Russia, have already signed on.[108]

3. The third and final phase, from 2036 to 2050, currently has fewer details on specific projects, but the goal is for China to be the premier spacefaring nation by then.[109]

Finally, China’s space administration published a policy notice entitled “Action Plan of the China National Space Administration for Promoting High-Quality and Safe Development of Commercial Space (2025-2027)” at the end of 2025.[110] The notice establishes China’s goal to have a “coordinated commercial space ecosystem, stronger innovation, efficient resource use, and tighter governance” for its commercial space industry by 2027.[111] The overall message of the notice is that China wants to commercialize critical parts of the space sector, including national technological development, standards setting, and enhanced space innovation capabilities.

Some of these policies are more about setting ambitious goals than actual regulatory change, but they still have an impact on the commercial space industry. These long-term plans will increasingly rely on participation from commercial companies, as has been the trend since 2014. Therefore, these plans guide the industry in terms of resource allocation. If a company can be the first to invent the technology that will enable long-term missions, it will receive greater investment and favoritism from the government; hence, policy directives shape innovation trends across the sector.

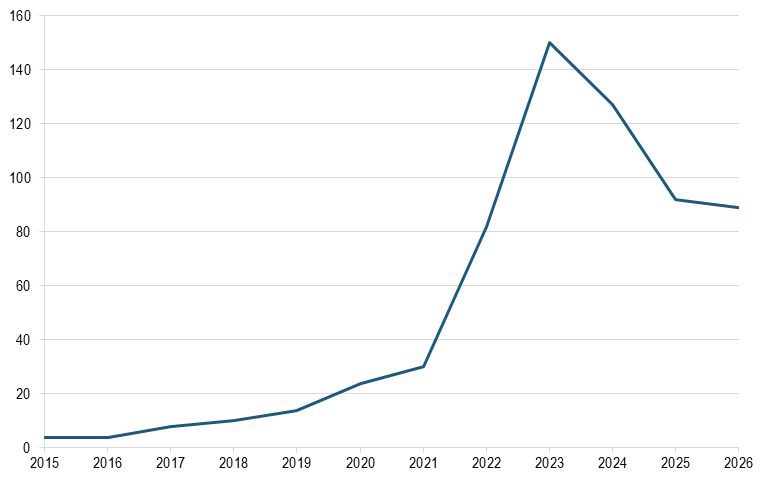

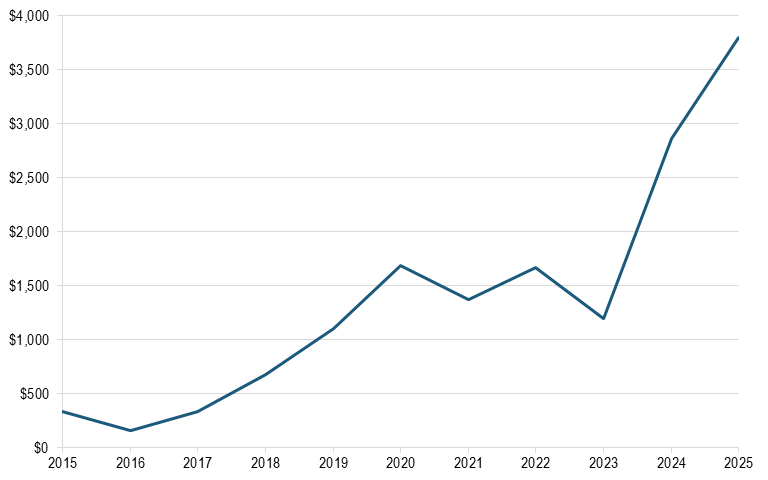

Document 60 opened the space sector to private investment, which, in conjunction with funding from the CCP and local governments, has helped China’s space industry grow steadily over the last 12 years.[112] From 2015 to 2025, investment in China’s space industry saw periods of growth and stagnation, peaking in 2025 at ¥26.6 billion ($3.8 billion), about 0.02 percent of China’s total gross domestic product (GDP) that year.[113] Annual investment from private, central, and provincial governments from 2015 through 2025 is displayed in figure 13.[114]

Figure 13: Annual capital investment in China’s space industry, 2015–2025 (millions)

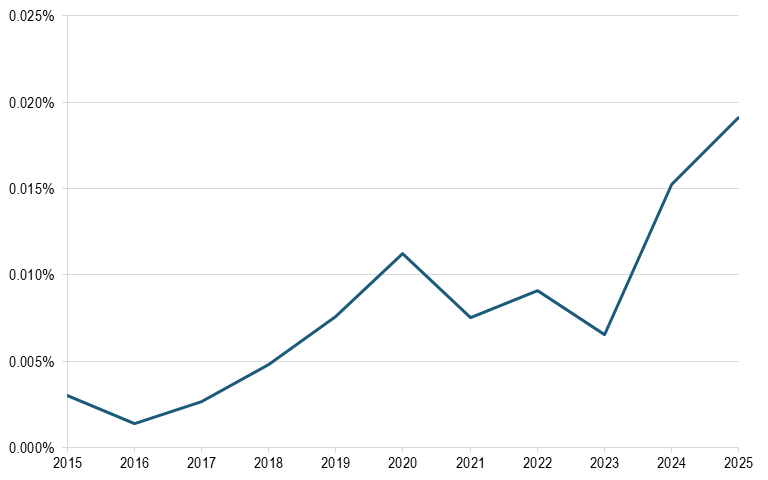

China’s investment intensity also grew over the last decade plus, with a slight dip during the COVID-19 pandemic. Investment intensity is space-sector funding as a percentage of annual nominal GDP. Figure 14 displays China’s annual R&D intensity from 2015 through 2025.[115] While investment intensity is just a fraction of a percent, the growth in intensity shows that China is increasingly prioritizing the space industry.

Figure 14: China’s annual space industry investment intensity, 2015–2025

China’s investment intensity was 0.05 percent less than that of the United States in 2025, as shown in figure 15. This difference means that the United States is currently spending more on space, as a fraction of total GDP, than China is.

Figure 15: Comparison of China and U.S. space industry investment intensity, 2025

The number of funding rounds for Chinese space companies increased significantly from 67 in 2024 to 137 in 2025.[116] The industry saw numerous new entrants raising early rounds, with 64 percent of the 137 rounds being Seed, Angel, or A rounds.[117] Simultaneously, there were 10 D rounds in 2025, compared with only 5 in total between 2014 and 2024. This increase in early and later funding rounds represents a growing number of space start-ups looking to enter the market and an increase in the number of Chinese companies reaching maturity.[118]

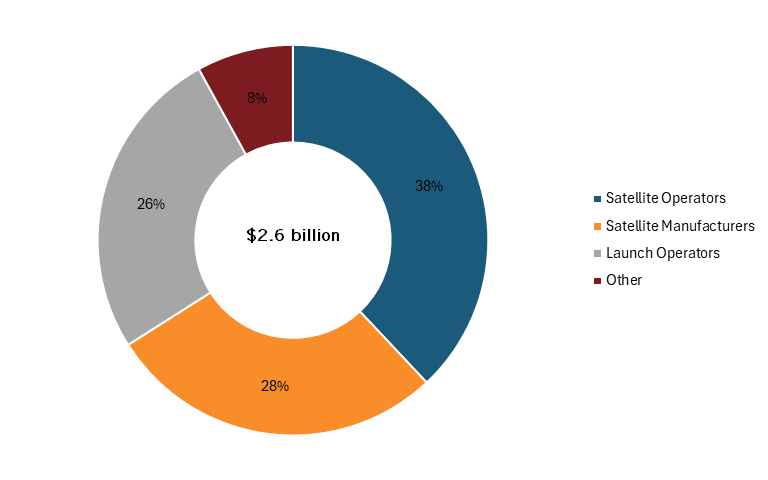

The breakdown of which space companies raised the most funds in 2024 is noteworthy. The biggest winners were satellite Internet operators and manufacturers, which collectively raised ¥13.6 billion ($1.9 billion), which was 0.01 percent of China’s 2024 GDP.[119] Launch operators raised more money in 2024 than in 2023, but the proportion of overall space industry funding decreased from 45 to 26 percent.[120] Other verticals, such as EO, struggled to raise funds, continuing a steep decline in funding since 2020. Figure 16 displays funding data for China’s space sector in 2024 from the European Space Policy Institute and Orbital Gateway Consulting.[121]

Figure 16: Chinese commercial space funding by vertical, 2024

Despite growing investment in China’s space sector over the last decade or so, CCP policies to expand the space industry don’t always get a strong return on investment. Blaine Curcio, founder of the space research firm Orbital Gateway Consulting, explained in an interview with ITIF that less-innovative companies often receive funding from provincial governments that want to align with national priorities and participate in the space industry.[122] The result is that politically driven investment drives up total investment numbers but does not necessarily indicate innovation to the same extent as market-driven investment through private capital or initial public offerings (IPOs).

One example is the launch company iSpace. Despite having had four failed launches in seven attempts since it first reached orbit in 2019, it is able to secure large funding rounds, securing a D++ funding round of ¥5 billion ($724.6 million) in February 2026.[123] This funding approach, wherein provincial governments are instructed to expand the space sector but lack clear, top-down funding mechanisms, dilutes the market by propping up inefficient operators and makes it difficult for commercial champions to secure a strong foothold in the market.

China’s space manufacturing base is a network of clusters called “agglomeration zones.”[124] Agglomeration zones are an ecosystem of companies in the same industry that cluster in and around a specific urban area.[125] In China, one or more space SOEs act as the anchor for each zone, and provincial and city governments create regulatory environments that encourage the development of an agglomeration zone in their region.[126] CASC is often the anchor for these zones, especially for space launch company clusters.[127]

The development of China’s space launch agglomeration zones provides a useful example of how China builds its manufacturing base, and why this system is so successful at rapidly scaling. In 2014, when Document 60 opened the space sector to private companies, members of CASC and other SOEs launched subsidiaries, or their own private companies, in large urban areas throughout the country. These new companies grow by purchasing their supply chain manufacturers, which become branch organizations that help each company achieve vertical integration across the entire supply chain.[128]

The agglomeration zone system enables innovation by streamlining the assembly process, which concentrates production and shortens development schedules for each company. Producing space technologies at scale allows for more frequent testing and iteration, which in turn leads to greater innovation. Plus, as companies buy up their supply chain, they can cut costs and allocate more resources toward production.

Despite manufacturing enhancements, this system can also harm competition in the commercial space market when provincial governments fund inefficient launch companies to make their region an agglomeration zone.[129] Companies never have a shortage of bidders when looking to expand to a new area, as regional governments try to appease the CCP and bring manufacturing to their city or province.[130] Like with capital investment, this system results in less-innovative companies receiving funding when they would not otherwise survive in a competitive market.

The United States is the most innovative country overall in space technology, but China now poses a legitimate threat to U.S. leadership and has surpassed the United States in certain sectors. Maintaining the top spot requires unleashing the innovative capacity of U.S. space companies by removing regulatory constraints, establishing permanent space stations in LEO, and engaging with global partners in international forums to promote American-led standards.

Regulatory reform should prioritize expansion of American launch capacity and the development of a robust orbital ecosystem. The United States has some of the most advanced rockets and satellites in the world, but overly burdensome regulations and outdated spaceport infrastructure limit innovation. Regulatory reforms to unleash U.S. space capabilities should include the following:

1. Regulatory agencies that manage radio frequency spectrum should allocate sufficient spectrum and improve sharing for launch operations, satellite connectivity, and non-communications spacecraft so that the space economy is not constrained by outdated rules that limit spectrum access.[131] As the space industry grows, there will be numerous types of novel spacecraft in orbit, all with different spectrum needs.[132] Ensuring that spectrum is readily available and flexible enough to support novel use cases is essential for maintaining American leadership.

2. Regulators should streamline licensing and environmental reviews for rockets and spaceports, enabling innovators to advance critical space technologies more quickly.[133] The application review process for rocket licenses in the United States lacks sufficient clarity and strict timelines, resulting in space companies waiting months and even years for approvals.[134] Environmental regulations, especially National Environmental Policy Act reviews for both rocket and spaceport licenses, also lead to significant delays that slow the pace of American space innovation. Streamlining licensing and environmental reviews would allow more frequent testing and iteration of new rockets and more expedient access to launch infrastructure, both of which would enhance American space innovation.

3. Finally, Congress should allocate additional resources to expand the size, scale, and operational capacity of U.S. spaceports to alleviate launch-schedule bottlenecks.[135] U.S. spaceport infrastructure has not been updated since the first space race with Russia, and most launches today take place at just two different spaceports owned by Space Force and NASA.[136] As the U.S. space sector continues to grow, there will be more launches of increasingly heavier rockets, which current spaceport infrastructure and operations will not be able to support. Enabling space innovation means building new public and privately-owned spaceports in addition to modernizing existing spaceport infrastructure.

The ISS is rapidly approaching the end of its service life. NASA should accelerate the Commercial Low Earth Orbit Destinations (CLD) program to ensure that new space stations replace the ISS before it’s deorbited in 2030.[137] The need to replace the ISS is now at the point where bureaucratic delay could become a diplomatic disaster. The CLD program must get moving again because it is a prerequisite for a continuous, crewed presence in LEO, which is essential to U.S. diplomacy with allies and maintaining a competitive advantage against China.

For two decades, the ISS was the only station to which countries could send their astronauts, but if China’s Tiangong station becomes the only option, other countries will not hesitate to use it. The United States must provide the best space stations because doing so would bolster its competitive stance versus China and improve diplomacy, as more countries would likely choose to partner with the United States over adversaries. NASA must successfully execute its plan to establish a robust CLD economy so the United States can maintain its competitive edge and continue to lead the frontiers of science, engineering, and space exploration.

Space is inherently global, and if the United States does not proactively engage with other nations on space policy priorities, then China will fill that void and try to derail U.S. space leadership. The World Radio Communications Conference in 2027 (WRC 27) comes at a defining moment for the future of international standards setting.[138] First, U.S. space companies are facing discriminatory regulations from foreign governments such as the EU Space Act, which will make it harder for American satellite companies to access the European market.[139] Even more troublesome is the fact that WRC 27 is being held in China, which the CCP will leverage to try to promote policy positions that benefit Chinese companies.[140] U.S. lawmakers should develop a unified set of policy positions for WRC 27 to effectively navigate this disadvantageous situation.

One such policy position is to encourage the International Telecommunication Union (ITU) to update its spectrum-sharing rules for satellites operating in LEO and GEO.[141] There are many more satellites in LEO than in GEO today, but ITU rules governing how each group uses spectrum were established when there were very few LEO satellites. These outdated rules limit the service offerings LEO satellites can provide. To remedy this issue, the Federal Communications Commission recently updated its rules for satellite spectrum sharing, enabling LEO satellite operators to provide better service to more consumers.[142] U.S. lawmakers should encourage ITU to update its rules at WRC 27 because doing so would help U.S. satellite companies be more competitive in the global market.

If the United States does not take decisive action soon, China will claim the top spot in the global space economy. China’s demonstrated strengths underscore that the window for the United States to consolidate its lead is narrowing, making regulatory reform and coordinated international engagement at forums such as WRC 27 not merely prudent but also strategically urgent. If China surpasses the United States in space, American economic competitiveness and national security will suffer.

About the Author

Ellis Scherer is a policy analyst at ITIF covering broadband, spectrum, and space policy. He previously interned with NTIA and worked as a cybersecurity consultant. He holds a master’s degree in terrorism and homeland security policy from American University and a bachelor’s degree in politics and history from the University of California, Santa Cruz.

About ITIF

The Information Technology and Innovation Foundation (ITIF) is an independent 501(c)(3) nonprofit, nonpartisan research and educational institute that has been recognized repeatedly as the world’s leading think tank for science and technology policy. Its mission is to formulate, evaluate, and promote policy solutions that accelerate innovation and boost productivity to spur growth, opportunity, and progress. For more information, visit itif.org/about.

[19]. “Satellite Statistics,” Planet4589.org.

[31]. Zhao Lei, “China to upgrade BeiDou Satellite System to boost accuracy, services,” China Daily, March, 13, 2026, https://www.chinadaily.com.cn/a/202603/13/WS69b3738ca310d6866eb3da6f.html; Sarah Sewall, Tyler Vandenberg, and Kaj Malden, “China’s BeiDou: New Dimensions, of Great Power Competition” (Belfer Center, February 2023), https://www.belfercenter.org/sites/default/files/pantheon_files/files/publication/Chinas-BeiDou_V10.pdf.

[35]. Bernadette Stadler and Meyer Thalheimer, “Hyperspectral Imaging,” CSI, July 19, 2019, https://ontheradar.csis.org/issue-briefs/hyperspectral-imaging-a-technology-primer/; Robert L. Morrison, “Radar Imaging,” NATO, January 20, 2026, https://www.sto.nato.int/document/radar-imaging/.

[40]. Swope, “No Place to Hide: A Look into China’s Geosynchronous Surveillance Capabilities.”

[42]. Swope, “No Place to Hide: A Look into China’s Geosynchronous Surveillance Capabilities.”

[43]. Jones, “China launches new highly retrograde Yaogan satellite, KZ-11 rideshare deploys 8 satellites.”

[44]. Swope, “No Place to Hide: A Look into China’s Geosynchronous Surveillance Capabilities.”

[45]. Jones, “Chinese commercial remote sensing satellite firm to double size of constellation.”

[47]. Destiny Doran, “Science in Orbit: Results Published on Space Station Research in 2024,” NASA, February 25, 2025, https://www.nasa.gov/missions/station/iss-research/science-in-orbit-results-published-on-space-station-research-in-2024; Paul Reichert et al., “Pembrolizumab microgravity crystallization experimentation,” NPJ Microgravity 5, December 2, 2019, https://www.nature.com/articles/s41526-019-0090-3.

[52]. “Space Threat Fact Sheet,” United States Space Force.

[70]. OECD Data Explorer, Bibliometric indicators, by field (Fractional counts of scientific publications among the world’s 10% top-cited scientific publications, Aerospace Engineering, 2010, 2024), https://data-explorer.oecd.org/.

[80]. “Overview of the Institute,” China Academy of Launch Vehicle Technology.

[84]. “LandSpace Technology Co., Ltd.,” Shanghai Stock Exchange.

[87]. “LandSpace Technology Co., Ltd.,” Shanghai Stock Exchange.

[103]. Andrew Jones, “Beijing government releases commercial space action plan,” Space News, February 9, 2024, https://spacenews.com/beijing-government-releases-commercial-space-action-plan/; Andrew Jones, “Venus atmosphere sample return noted in China’s long-term space science roadmap,” Space News, October 22, 2024, https://spacenews.com/venus-atmosphere-sample-return-noted-in-chinas-long-term-space-science-roadmap/.

[104]. Jones, “Venus atmosphere sample return noted in China’s long-term space science roadmap.”

[112]. Boyd, Green, and Nouwens, “China’s commercial space sector.”

[116]. Curcio, “#SpaceWatchGL Insights: 2025 Funding Recap of the Chinese Space Industry.”

[120]. “Space Venture 2024: Global Investment Dynamics,” European Space Policy Institute.

[122]. Blaine Curcio, (interview with ITIF on China’s space industry, April 28, 2026).

[131]. Ellis Scherer, “Comments to the FCC Regarding Modernizing Spectrum Sharing for Satellite Broadband” (ITIF, July 2025), https://.org/publications/2025/07/28/comments-to-fcc-regarding-modernizing-spectrum-sharing-for-satellite-broadband/; Ellis Scherer, “Comments to the FCC Regarding Space Modernization for the 21st Century” (ITIF, January 2026), https://itif.org/publications/2026/01/20/comments-to-the-fcc-regarding-space-modernization-for-the-21st-century/; Ellis Scherer, “Comments to the FCC Regarding Spectrum Abundance for ‘Weird Space Stuff’” (ITIF, May 11, 2026), https://itif.org/publications/2026/05/11/comments-to-the-fcc-regarding-spectrum-abundance-for-weird-space-stuff/.

[132]. Scherer, “Comments to the FCC Regarding Spectrum Abundance for ‘Weird Space Stuff.’”

[140]. “ITU World Radiocommunication Conference 2027,” ITU.