In the last week, the United States market has stayed flat, yet it is up 29% over the past year with earnings forecasted to grow by 16% annually. In such a climate, identifying stocks that are potentially undervalued can present opportunities for investors looking to capitalize on discrepancies between stock prices and their intrinsic values.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

|

Name |

Current Price |

Fair Value (Est) |

Discount (Est) |

|

Seagate Technology Holdings (STX) |

$673.64 |

$1330.31 |

49.4% |

|

Q2 Holdings (QTWO) |

$50.75 |

$97.97 |

48.2% |

|

First Merchants (FRME) |

$40.44 |

$77.39 |

47.7% |

|

FinWise Bancorp (FINW) |

$15.55 |

$29.71 |

47.7% |

|

FB Financial (FBK) |

$54.07 |

$103.19 |

47.6% |

|

Chemung Financial (CHMG) |

$66.41 |

$127.22 |

47.8% |

|

BillionToOne (BLLN) |

$75.05 |

$147.13 |

49% |

|

AppLovin (APP) |

$446.35 |

$858.66 |

48% |

|

Alnylam Pharmaceuticals (ALNY) |

$309.49 |

$610.25 |

49.3% |

|

Aldeyra Therapeutics (ALDX) |

$1.52 |

$3.02 |

49.6% |

Let’s uncover some gems from our specialized screener.

Overview: Extreme Networks, Inc. is a company that develops, markets, and sells network infrastructure equipment and related software globally, with a market cap of approximately $2.93 billion.

Operations: Revenue Segments (in millions of $): Extreme Networks generates its revenue through the sale of network infrastructure equipment and associated software across various regions including the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

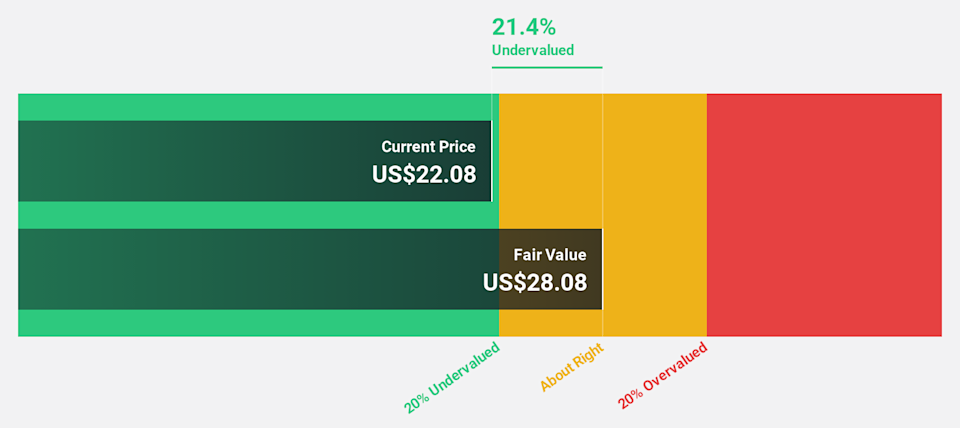

Estimated Discount To Fair Value: 35%

Extreme Networks is trading at 35% below its estimated fair value, with shares priced at US$22.09 against a future cash flow valuation of US$33.97. Recent earnings showed strong growth, with net income rising to US$10.59 million in Q3 from US$3.46 million a year ago, driven by increased revenue and strategic product innovations like Extreme Platform ONE. The company forecasts robust earnings growth of 27.1% annually over the next three years, outpacing the broader market expectations.

Overview: FTAI Aviation Ltd. owns, acquires, and sells aviation equipment for global transportation of goods and people, with a market cap of $21.86 billion.

Operations: FTAI Aviation generates revenue through the ownership, acquisition, and sale of aviation equipment used in worldwide transportation.

Estimated Discount To Fair Value: 18.7%

FTAI Aviation is trading at US$249.67, about 18.7% below its estimated fair value of US$307.22 based on discounted cash flow analysis. Despite a decline in sales to US$39.89 million, revenue surged to US$830.7 million in Q1 2026 from the previous year, boosting net income to US$137.9 million. Earnings are projected to grow significantly at 28% annually, surpassing market averages and highlighting strong future cash flow potential despite current debt challenges.