Discover 3 Asian Growth Companies With Insider Ownership Up To 23%

Uncategorized

Discover 3 Asian Growth Companies With Insider Ownership Up To 23%

07 mins

As global markets navigate geopolitical uncertainties and economic shifts, Asia’s stock markets have shown resilience, with mainland equities maintaining stability amid strong economic data. In this context, growth companies with significant insider ownership can be particularly appealing as they often indicate confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In Asia

Below we spotlight a couple of our favorites from our exclusive screener.

Simply Wall St Growth Rating: ★★★★★★

Overview: Akeso, Inc. is a biopharmaceutical company focused on the research, development, manufacture, and commercialization of antibody drugs globally with a market cap of HK$125.09 billion.

Operations: The company’s revenue primarily comes from the research, development, production, and sale of biopharmaceutical products, amounting to CN¥3.06 billion.

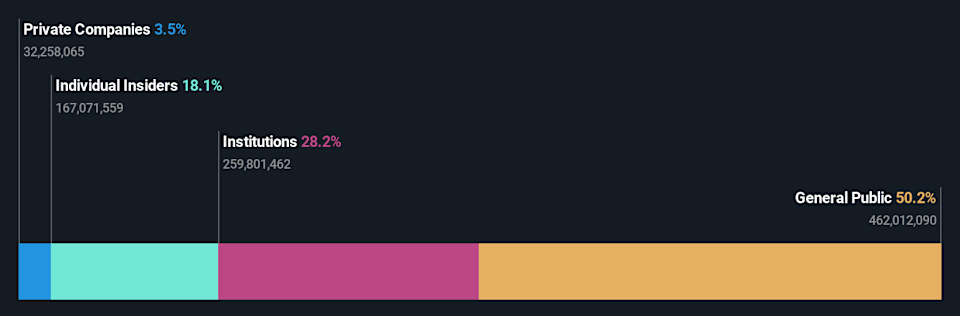

Insider Ownership: 18.1%

Akeso is poised for growth with a strong pipeline of innovative bispecific antibodies, including ivonescimab and cadonilimab, which have shown promising clinical results. The company is trading at 25.2% below estimated fair value and is expected to achieve profitability within three years. Revenue growth forecasts at 29.1% annually surpass market averages, supported by significant advancements in oncology treatments like the recent upgrades for ivonescimab in NSCLC guidelines.

SEHK:9926 Ownership Breakdown as at Apr 2026

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Daimay Automotive Interior Co., Ltd specializes in the research, development, and sale of passenger car components both in China and internationally, with a market cap of CN¥23.51 billion.

Operations: Shanghai Daimay Automotive Interior Co., Ltd generates revenue through the development and sale of passenger car components across domestic and international markets.

Insider Ownership: 23.3%

Shanghai Daimay Automotive Interior is positioned for growth, with earnings projected to rise 29.41% annually, outpacing the Chinese market’s 26.9%. Despite trading at 30.8% below its fair value estimate, recent quarterly results showed a decline in both sales (CNY 1,539.31 million) and net income (CNY 186.43 million) compared to last year. The dividend yield of 2.46% lacks earnings coverage, yet revenue growth remains robust at an annual rate of 16%.

SHSE:603730 Ownership Breakdown as at Apr 2026

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zhuzhou Huarui Precision Cutting Tools Co., Ltd. operates in the manufacturing sector, specializing in precision cutting tools, with a market cap of CN¥14.22 billion.

Operations: Revenue Segments (in millions of CN¥):

Insider Ownership: 20.1%

Zhuzhou Huarui Precision Cutting Tools Ltd. demonstrates significant growth potential, with revenue forecasted to increase by 22.6% annually, surpassing the Chinese market’s average. Recent earnings showed substantial improvement, with Q1 net income rising to CNY 175.19 million from CNY 29.22 million a year earlier. Despite high share price volatility and an unstable dividend history, its price-to-earnings ratio of 42.7x is below the market average, indicating relative value in its sector.

SHSE:688059 Earnings and Revenue Growth as at Apr 2026

Key Takeaways

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:9926 SHSE:603730 and SHSE:688059.