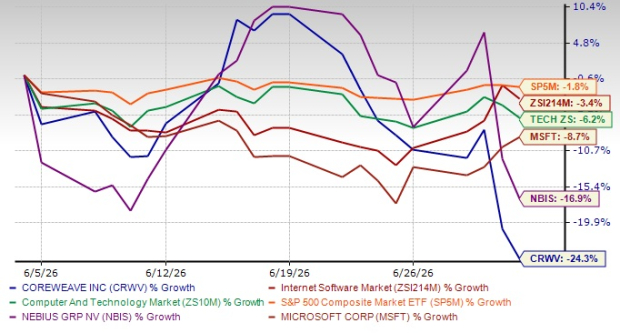

Despite being one of the market’s biggest AI winners, CoreWeave, Inc. CRWV stock has plunged roughly 24% over the past month as investors reassessed lofty valuations and growing competitive risks in the AI infrastructure space. Shares have underperformed the Zacks Internet-Software Market’s fall of 3.4% as well as the Zacks Computer & Technology sector and the S&P 500 Composite decline of 6.2% and 1.8%, respectively, in the same period.

Image Source: Zacks Investment Research

CRWV stock is lagging behind tech heavyweights like Microsoft MSFT, which has plunged 8.7% over the same period, and its direct competitor, Nebius Group N.V. NBIS, another emerging AI infrastructure play, whose shares declined 16.9%. Microsoft develops PCs, tablets, gaming systems and other smart devices, while Azure provides cloud software, services and infrastructure. Like CRWV, Nebius focuses on GPU-powered AI cloud computing and infrastructure solutions for enterprises and developers, making it a key player in the growing AI infrastructure market.

The decline begs an important question now: Is this correction creating a buying opportunity, or is it a warning that more downside could lie ahead?

The answer depends on whether investors believe CoreWeave can maintain its extraordinary growth while navigating an increasingly competitive AI cloud market.

Why Investors are Selling CRWV Stock

Several factors have pressured the stock. The latest sell-off accelerated after reports that Meta Platforms META is exploring ways to commercialize its excess AI computing capacity. Such a move would transform Meta from a major AI customer into a potential competitor for companies like CoreWeave. The news also pressured fellow AI cloud provider Nebius, highlighting investor worries about intensifying competition in the “neocloud” market. Competition from hyperscalers such as Meta, Amazon, Microsoft and Alphabet, which possess enormous financial resources and existing cloud infrastructure, is a major overhang.

CoreWeave’s business requires enormous ongoing investments in GPUs, networking equipment and data centers. These investments require substantial financing, increasing leverage and interest expenses, while delaying the generation of free cash flow. As of March 31, 2026, the company’s long-term debt totaled $25.4 million. Interest expenses are expected to increase in the second quarter to as much as $730 million as debt levels rise to fund deployments. CRWV also raised its full-year capital expenditure outlook to $31-$35 billion, citing higher component costs and substantial spending needed to bring new capacity online.

Image Source: Zacks Investment Research

Although CoreWeave has expanded its customer base, a significant portion of revenue still comes from a handful of large AI companies. Any slowdown in spending by these customers could materially affect financial results. Moreover, profitability remains limited. For the first quarter, CoreWeave reported an adjusted net loss of roughly $589 million, wider than the prior-year quarter’s loss of $150 million. Adjusted operating income fell to $21 million from $163 million a year earlier, while operating margin dropped to just 1%.

The Bull Case: Why Investors are Still Optimistic About CRWV

Despite recent weaknesses, the long-term investment outlook remains strong. The company reported first-quarter 2026 revenue growth of more than 100% year over year, driven by strong demand for AI infrastructure. Its contracted revenue backlog continues to grow, offering multi-year visibility into future earnings. CoreWeave has also deepened its relationships with leading AI firms, including OpenAI, Meta and Anthropic, while continuing to deploy the latest NVIDIA NVDA GPU architectures across its cloud platform. It became the first AI cloud provider to complete system-level validation of NVDA Vera Rubin NVL72, reaffirming its leadership in next-generation AI infrastructure.

In January, NVIDIA increased its investment in CoreWeave to $2 billion. CRWV is expanding its infrastructure footprint, surpassing GW of active power and securing more than 3.5 GW of contracted power, aiming to reach 8 GW by 2030. It added more than 40 MW of contracted power in the first quarter, with most capacity expected to come online by 2027. To support this growth, CoreWeave is investing in a mix of long-term leased and self-constructed data centers, with its first self-built facility scheduled to become operational later in 2026. Its network now includes nearly 50 data centers, while maintaining efficient deployment timelines. The company is “virtually sold out” for 2026, with most infrastructure components already secured.

Image Source: Zacks Investment Research

CoreWeave is benefiting from accelerating demand for AI compute, particularly as AI workloads shift from training to inference, increasing demand for high-performance GPUs such as the A100, H100, H200 and L40. This trend has driven higher GPU pricing and improved capacity utilization, supporting the company’s expectation of expanding margins as additional capacity comes online. For 2026, CRWV projects revenue of $12-$13 billion and operating income of $900 million-$1.1 billion. It expects second-quarter revenue of $2.45-$2.6 billion, with further margin expansion. The company targets more than $30 billion in revenue by 2027, with approximately 75% of that revenue already under contract.

CRWV Faces Unfavorable Estimate Revision Trend

The Zacks Consensus Estimate for CoreWeave’s earnings for 2026 has been revised south 8.3% over the past 60 days.

Image Source: Zacks Investment Research

CRWV Valuation Looks More Reasonable But Not Cheap

The recent pullback has eased some valuation concerns. Although the stock is cheaper than it was a month ago, expectations remain extremely high. Its Value Style Score of D suggests a stretched valuation at this moment. In terms of Price/Book, CRWV’s shares are trading at 7.61X, higher than the Internet Software industry’s 4.61X.

Image Source: Zacks Investment Research

In comparison, NBIS and MSFT are trading at multiples of 7.53X and 7X, respectively.

Investment Verdict

CoreWeave remains one of the most compelling pure-play AI infrastructure companies in the public market. It benefits from explosive AI demand, a massive contracted backlog and strategic relationships with industry leaders, all of which support a favorable long-term growth outlook. However, rich valuation, heavy capital spending requirements, customer concentration and rising competition from hyperscalers could continue driving sharp price swings.

For aggressive growth investors with a long investment horizon, the recent 24% decline may represent an opportunity to gradually build a position. More conservative investors, however, may prefer to stay on the sidelines until CoreWeave demonstrates stronger profitability and greater resilience against emerging competitive threats.

With a Zacks Rank #3 (Hold), CRWV appears to be treading in the middle of the road, and new investors could be better off if they trade with caution. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI’s Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren’t likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

CoreWeave Inc. (CRWV) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report

Nebius Group N.V. (NBIS) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.