As the world’s largest manufacturer of heavy construction and mining equipment, Caterpillar (CAT) has long been seen as a bellwether for the global economy. Happily for long-term shareholders, CAT’s returns have greatly outpaced the global economy – and U.S. stock market – for decades.

Caterpillar’s outperformance in the 21st century was never a foregone conclusion. If anything, a company founded a century ago to supply tractors for delta farmers and New Deal works projects should be about as old-economy as they come.

It’s not. Caterpillar has spent the past two decades navigating massive cyclical changes to the global economy very much to shareholders’ benefit. For example, few firms gained more from the China-led commodities supercycle of the early 2000s.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

On the other hand, CAT could have had better timing when it acquired mining equipment giant Bucyrus International near the top of the cycle in 2011. The hangover from the end of the boom was a headwind for shares for a good 10 years.

However, it also forced CAT to double down on finding operational efficiencies, like expanding its parts and maintenance business. Services carry higher profit margins than sales of earthmoving equipment and diesel-electric locomotives.

The biggest driver of recent returns – and expanding multiples – is Caterpillar’s emergence as a huge bet on the build-out of artificial intelligence. Indeed, CAT isn’t a tractor company anymore; it’s a very 21st-century critical infrastructure and energy play.

The AI era has created massive demand for the construction of data centers and the energy needed to power them. Rising prices for commodities, especially copper and lithium, have led mining companies to upgrade their equipment with Caterpillar’s latest offerings.

And in another techy twist, Caterpillar even has a recurring revenue stream. Thanks to the Internet of Things (IoT), Caterpillar can make sure its legions of customers buy parts and services only from its own dealer network.

That said, stocks never go up in a straight line, and that’s certainly been true of this Buy-rated Dow Jones stock.

The bottom line on Caterpillar stock

Long-time CAT shareholders are used to the cyclical nature of this bluest of blue-chip industrial stocks. Besides, periods of underwhelming performance always came with a reliable and rising dividend. As a member of the S&P 500 Dividend Aristocrats, Caterpillar is one of the best dividend stocks for dependable dividend growth.

At any rate, buy-and-hold patience has really paid off. The AI era has been a boon for CAT.

Over its entire life as a publicly traded company, CAT generated an annualized total return (price change plus dividends) of 16.3%. That beats the broader market by about 6 percentage points.

CAT also beats the S&P 500 by wide margins over the past one-, three-, five-, 10- and 15-year periods.

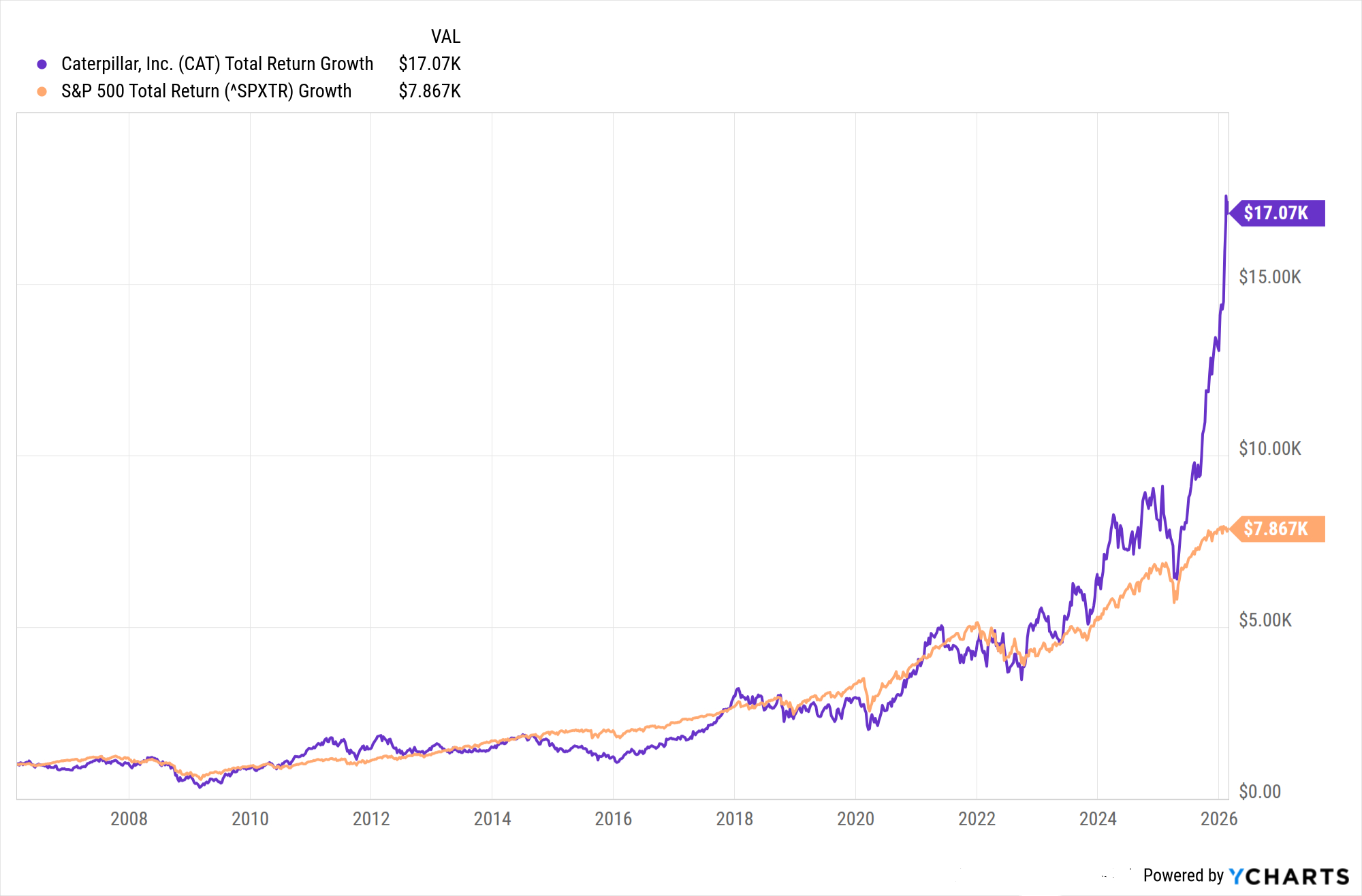

Which brings us to what $1,000 invested in Caterpillar stock would be worth today. Have a look at the above chart and you’ll see that if you put $1,000 into CAT stock 20 years ago, it would be worth $17,000 today. The same amount invested in an S&P 500 index fund would be worth about $7,800.

Even better, Wall Street sees more outperformance ahead. Of the 29 analysts covering CAT stock surveyed by S&P Global Market Intelligence, 14 call it a Strong Buy, one says Buy, 12 have it at Hold and two call it a Strong Sell. That works out to a rare consensus recommendation of Buy with solid conviction.

Speaking for the bulls, Oppenheimer analyst Kristen Owen likes the company’s exposure to both the world of electrons and the world of atoms.

“CAT is underappreciated as a play on AI for the physical world,” writes Owen, who rates shares at Outperform (the equivalent of Buy). “We believe its strength and diversity of backlog growth, the durability afforded by 40% of sales stemming from services, and a continued willingness to consistently buy back shares as structural underpinning for CAT’s next phase of growth.”