Hong Kong has adopted the BEPS 2.0 Pillar Two global minimum tax rules effective from January 1, 2025. This article examines the latest transfer pricing trends in Hong Kong, including documentation requirements, IRD audit priorities, and practical steps for MNE groups.

Transfer pricing is an unavoidable subject for multinational enterprises (MNE) operating in Hong Kong. The Inland Revenue Department (IRD) has been paying much closer attention to cross‑border related‑party transactions in recent years. The OECD’s BEPS 2.0 framework – especially the Pillar Two global minimum tax – now directly affects Hong Kong.

This article covers three main areas: the current state of BEPS 2.0 in Hong Kong, what the IRD expects from transfer pricing documentation, and the key trends in tax audits and Advance Pricing Arrangements (APAs). It also gives practical advice for MNE groups to stay on the right side of the rules.

Start exploring

BEPS 2.0 in Hong Kong: Pillar Two implementation

Find Business Support

Hong Kong began implementing the OECD’s Pillar Two global minimum tax rules for fiscal years starting on or after January 1, 2025. The rules apply to MNE groups that have consolidated revenue of EUR 750 million or more in at least two of the last four financial years. For these groups, Hong Kong now imposes a top‑up tax if their effective tax rate in the city falls below 15 percent. The Hong Kong Minimum Top‑up Tax (HKMTT) ensures that Hong Kong – not another jurisdiction – collects any top‑up tax that is due.

This protects the city’s taxing rights and aligns with international expectations.

Affected groups must file a top‑up tax notification and later a full Pillar Two return. The HKMTT filing requirements are also applicable. The deadlines are tight and missing them can lead to penalties. Many MNE groups are still getting used to these new obligations, but early preparation makes a significant difference.

Read also:

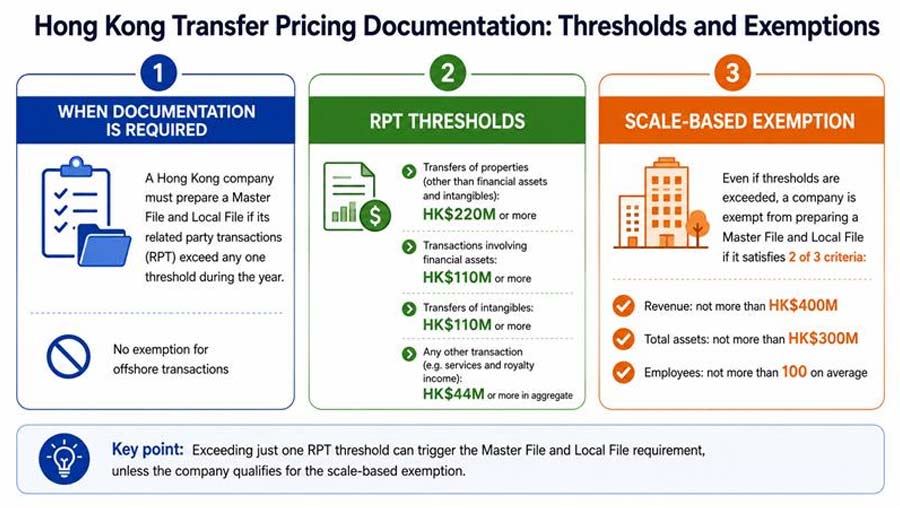

Transfer pricing documentation requirements

Hong Kong follows the OECD’s three‑tiered documentation model.

Country‑by‑Country (CbC) report. This is required for groups with consolidated revenue of EUR 750 million or more. It gives tax authorities a high‑level view of where profits, taxes, and economic activity are reported globally.

Master file and local file. These apply to entities, depending on the size and nature of their related‑party transactions. The IRD has issued detailed guidance (DIPN 58) on what information each file should contain.

Deadline: All documentation must be prepared on a contemporaneous basis. Files should be prepared within nine months after the end of the relevant accounting period and retained for seven years.

Deadline: All documentation must be prepared on a contemporaneous basis. Files should be prepared within nine months after the end of the relevant accounting period and retained for seven years.

The IRD also expects documentation to include proper functional analysis, a benchmarking study, and a clear explanation of why the chosen transfer pricing method is appropriate. Missing any of these elements can easily trigger follow‑up questions.

IRD’s audit trends and focus areas

Over the past few years, the IRD has noticeably stepped up its transfer pricing audits. Based on the IRD’s published guidance and enforcement practice, some common audit triggers stand out.

First, persistent losses or unusually low profitability attract attention. If a Hong Kong company reports losses year after year while its foreign parent or affiliated companies are profitable, the IRD will want to know why. Second, high payments to related parties – such as royalties, service fees, or interest – are closely examined. Third, large intercompany loans with interest rates that do not reflect market conditions are a red flag.

In terms of focus areas, the IRD pays special attention to:

- Intercompany financing (loans, guarantees, cash pooling)

- Transfers of intangible assets (trademarks, technology, know‑how)

- Management and service fees charged between group companies

- Cost sharing arrangements

IRD may review related-party pricing using benchmarking studies and other external data to assess whether the pricing follows the arm’s length principle. If IRD considers that the reported price is not arm’s length, it may adjust the taxable profits or losses for tax purposes, which can result in additional tax payable. In practice, the tax consequences may also include penalties or interest depending on the facts and the applicable provisions, so taxpayers should maintain robust transfer pricing documentation and support for their pricing positions.

Advance Pricing Arrangements (APAs) as a risk management tool

An Advance Pricing Arrangement (APA) is a formal agreement with the IRD that sets out an acceptable transfer pricing method for future transactions. Hong Kong offers three types of APAs: unilateral (only Hong Kong), bilateral, and multilateral. Bilateral and multilateral APAs involve tax authorities from other jurisdictions under Hong Kong’s tax treaties.

Find Business Support

The benefits of an APA are clear. It provides tax certainty for a fixed period, typically three to five years. It also greatly reduces the risk of a costly audit later. The application process can take six to twelve months, but the protection is well worth the effort. Once an APA is approved, the IRD will not challenge the covered transactions unless there is a material change in the facts.

Practical steps for MNE groups

Here are six practical steps that every MNE group with Hong Kong operations should consider.

1. Assess whether your group falls under Pillar Two. Look at your consolidated revenue for the last four years. If you meet the EUR 750 million threshold in at least two years, you must comply with the global minimum tax rules.

2. Review your existing intercompany agreements and pricing policies. Make sure your contracts reflect the actual business activities. Check that prices – such as royalty rates, and service fees – are set at arm’s length. Keep clear records of how you determined each price.

3. Prepare contemporaneous transfer pricing documentation. Do this before you file your Profits Tax Return. Use the threshold of DIPN 58 as your checklist. Include a functional analysis, a benchmark study, and a clear explanation of your chosen pricing method.

4. Consider applying for an APA for high‑risk transactions. If you have large or complex related‑party dealings, for example, intercompany loans or intangible asset transfers, an APA can save you from future disputes.

5. Consult a tax advisor regarding transfer pricing planning arrangements. Transfer pricing rules are detailed and technical. We can provide professional solutions that can help ensure the relevant related party transactions in consistency with the arm’s length principle, reducing audit exposure.

6. Keep an eye on changes in tax law and IRD guidance. Given the ever-changing trends in global international taxation. The rules may evolve, and the IRD may issue further guidance. Staying informed helps you stay ahead.

Conclusion

With the implementation of Pillar Two in Hong Kong, transfer pricing compliance has become increasingly prevalent in the region and drawn growing scrutiny from the IRD of Hong Kong in recent years.

Prevention is the ultimate risk defense. To begin with, we need to formulate a transfer pricing policy in full compliance with tax regulations. Complete all compliance filings as required, covering three tiers of transfer pricing documentation: Country-by-Country Report (CbCR), CbCR notification, Master File and Local File. Always keep your intercompany prices at arm’s length and take a regular review(annual/quarterly/monthly). For high‑risk transactions, consider the comprehensive advance risk analysis, as well as APA as a tax remedy measure.

How Dezan Shira & Associates can help

Dezan Shira & Associates supports MNE groups in navigating Hong Kong’s evolving transfer pricing and BEPS 2.0 landscape. Our tax specialists assist with Pillar Two impact assessments and HKMTT compliance, the preparation of contemporaneous transfer pricing documentation — including master files, local files, and CbC reporting under DIPN 58 — as well as benchmarking studies, intercompany agreement reviews, and APA applications. We also represent clients in IRD audits and transfer pricing disputes, helping ensure related-party transactions remain consistent with the arm’s length principle.

For assistance with transfer pricing compliance in Hong Kong, please contact us at hongkong@dezshira.com or visit www.dezshira.com.

Tax planning and compliance in Hong Kong require careful navigation of evolving local and international tax rules. Our experienced advisors support businesses with corporate tax, indirect tax, individual tax, international tax, and transfer pricing, helping them remain compliant while optimizing their tax position in Hong Kong and the wider Asia?Pacific region.

Partner

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.