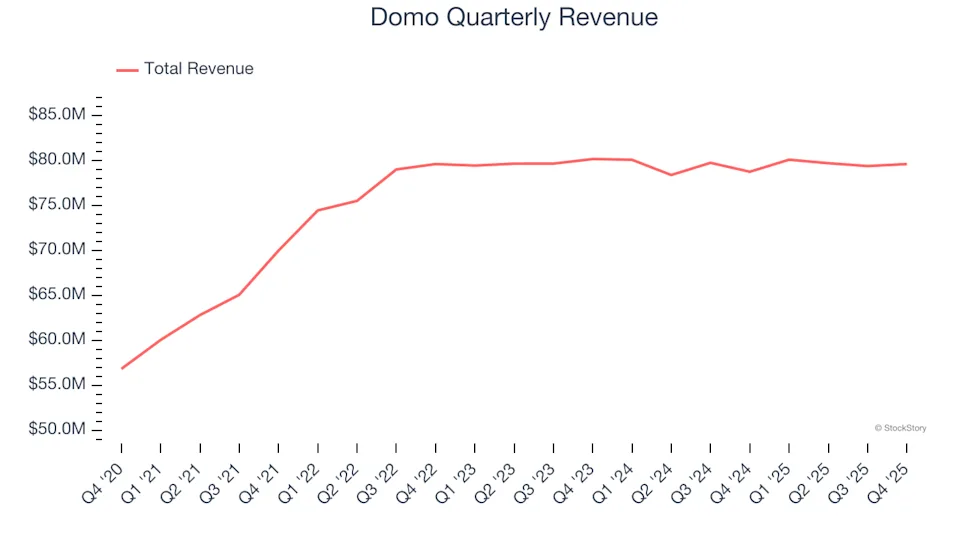

Business intelligence platform Domo (NASDAQ:DOMO) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 1.1% year on year to $79.63 million. Its non-GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Domo? Find out in our full research report.

-

Revenue: $79.63 million vs analyst estimates of $78.62 million (1.1% year-on-year growth, 1.3% beat)

-

Adjusted EPS: $0.03 vs analyst estimates of -$0.03 (significant beat)

-

Adjusted Operating Income: $8.13 million vs analyst estimates of $3.86 million (10.2% margin, significant beat)

-

Operating Margin: -13.3%, up from -15.6% in the same quarter last year

-

Free Cash Flow was -$5.34 million, down from $2.07 million in the previous quarter

-

Billings: $111.2 million at quarter end, up 8.4% year on year

-

Market Capitalization: $178.5 million

“We delivered our highest quarterly billings ever and our highest gross retention rate in over three years, reflecting strong demand from customers and the growing role Domo plays in their AI strategies,” said Josh James, founder and CEO of Domo.

Named for the Japanese word meaning “thank you very much,” Domo (NASDAQ:DOMO) provides a cloud-based business intelligence platform that connects people with real-time data and insights across organizations.

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Domo’s 8.7% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the software sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Domo’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Domo reported modest year-on-year revenue growth of 1.1% but beat Wall Street’s estimates by 1.3%.

Looking ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.