Key Points

Tesla (NASDAQ: TSLA) investors received some good news recently, as Goldman Sachs raised its estimate for Tesla’s second-quarter electric vehicle (EV) deliveries to 420,000 from 405,000, noting particular strength in Europe. It’s a positive sign, with many implications for future growth. Still, it’s not the only thing investors should be focused on in 2026.

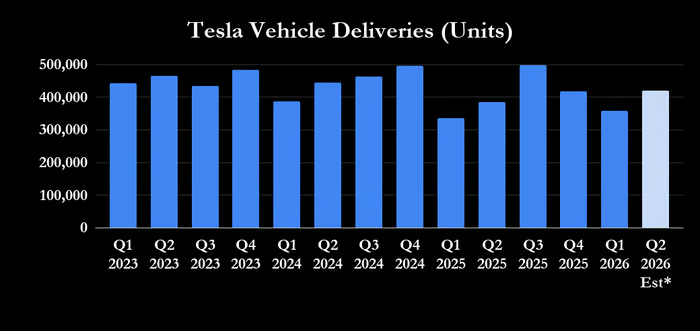

Goldman Sachs raises Tesla EV delivery estimates

Tesla sells directly to consumers, so, unlike most other automakers, its EV delivery data is, in fact, its EV sales volume. As such, if the upgrade is accurate, it represents a significant upgrade in sales expectations. In addition, it would represent a 9.3% year-over-year increase, even as Tesla ceased production of the Model S and Model X in the quarter.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

The 420,000 figure also represents a 17.3% sequential increase in first-quarter deliveries. Moreover, it would put Tesla on about 778,000 deliveries in the first half of the year, an increase of 7.9% on the first half of 2025.

Whichever way you look at it, Tesla looks on track to grow EV deliveries in 2026, as argued previously.

Data source: Tesla presentations. *Goldman Sachs estimate. Chart by author.

Two key conclusions

First, much ink was spilled last year by many arguing that there was some sort of brand damage resulting from CEO Elon Musk’s political involvement, including trying to reduce the U.S. debt burden. It was always a weak argument, given that Model 3 sales consistently performed well in 2025 in the U.S., while Model Y suffered.

Unless you think that consumers ascribe political opinions to the Model Y rather than the Model 3, then it makes no sense. Moreover, the particular strength in Europe in 2026 further confirms the point that there is only minimal brand damage from Musk’s political involvement.

Second, a more plausible explanation for the bounce-back in 2026 is that the Model Y refresh significantly slowed sales in the first half of 2025, and now Model Y sales (probably the best-selling car in the world) are “normalizing.”

Optimus and robotaxis are what really matter

Just as it was important not to overreact and panic last year when Tesla’s EV deliveries were declining, it makes sense not to be overexuberant about a significant increase in deliveries in 2026. As Tesla bulls have long argued, Tesla is not just a car company; the real long-term growth catalysts will come from its robotaxi service and, as Musk never ceases to tell investors, Optimus.

![]()

Image source: Tesla.

It follows that developments in those two initiatives require close monitoring in 2026 as management positions the company for a year of foundational growth.

On the lastearnings call Musk said he wanted to push back the unveiling of the latest version of Optimus (v3) to when production begins, “somewhere around the late July, August time frame.” It’s now June, so investors should look out for an announcement on it in the coming months.

As for robotaxi, the rollout pace is frustrating many Tesla investors, as it appears to have stalled. However, it’s important to listen to what Tesla’s management has to say on the matter. On the lastearnings call Musk said that Tesla wouldn’t deploy “unsupervised FSD Robotaxi large scale” until it had new improvements to its full self-driving (FSD) software that needed to be written, validated, and released.

Image source: The Motley Fool.

These improvements will likely come with v15 FSD, which is due in late 2026 or early 2027. As such, anyone thinking that a few robotaxis here or there will drive the share price in 2026 is mistaken, and the large-scale ramp-up many are hoping for is highly unlikely until 2027.

What investors should consider

The potential recovery in EV sales is good news and will help the investment case. Still, the key catalysts are robotaxis and Optimus, and their ongoing development is the real swing factor in deciding the company’s stock price. A balanced viewpoint is necessary.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $531,453!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $56,406!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $415,040!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of June 18, 2026.

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.