Hongkong and Shanghai Hotels (SEHK:45) has drawn fresh attention after reporting unaudited first quarter 2026 operating figures, with revenue per available room (RevPAR) for The Peninsula Hotels higher across Greater China, Europe, the USA and Asia.

See our latest analysis for Hongkong and Shanghai Hotels.

Despite the positive RevPAR update and recent board changes, the share price at HK$5.99 has a 90 day share price return that declined 12.43%, while the 1 year total shareholder return of 11.13% points to improving but uneven momentum.

If hotel stocks have your attention, you might also want to broaden your search and check out 101 top founder-led companies

With RevPAR figures rising across all regions but the share price still down over the past 90 days, investors now face a key question: is Hongkong and Shanghai Hotels undervalued, or is the stock already pricing in future growth?

Price-to-Earnings of 31.2x: Is it justified?

On a P/E of 31.2x at a share price of HK$5.99, Hongkong and Shanghai Hotels trades at a premium compared to both peers and the wider Hong Kong hospitality sector.

The P/E ratio compares the current share price to earnings per share and, for hotel operators like Hongkong and Shanghai Hotels, often reflects how the market views the stability of profits and the quality of assets. A higher P/E can indicate that investors are comfortable paying more for each dollar of earnings when a company has valuable brands, prime real estate or a record of returning to profitability.

Here, the premium P/E sits alongside a recent return to profit, a large one off gain of HK$287.0m in the last 12 months to 31 December 2025 and a low Return on Equity of 0.9%. That mix suggests the market is paying up for earnings that are partly supported by non recurring items rather than purely by ongoing hotel and property operations.

Compared to the peer average P/E of 17.5x and the Hong Kong hospitality industry average of 15.8x, Hongkong and Shanghai Hotels is priced at a materially higher level. This gap indicates the stock is valued more richly than many local competitors, and the premium would typically require ongoing earnings quality to support it over time.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 31.2x (OVERVALUED)

However, there are still clear risks, including the stock’s 3 year and 5 year total returns lagging and earnings that include a large one off gain.

Find out about the key risks to this Hongkong and Shanghai Hotels narrative.

Another view using cash flows

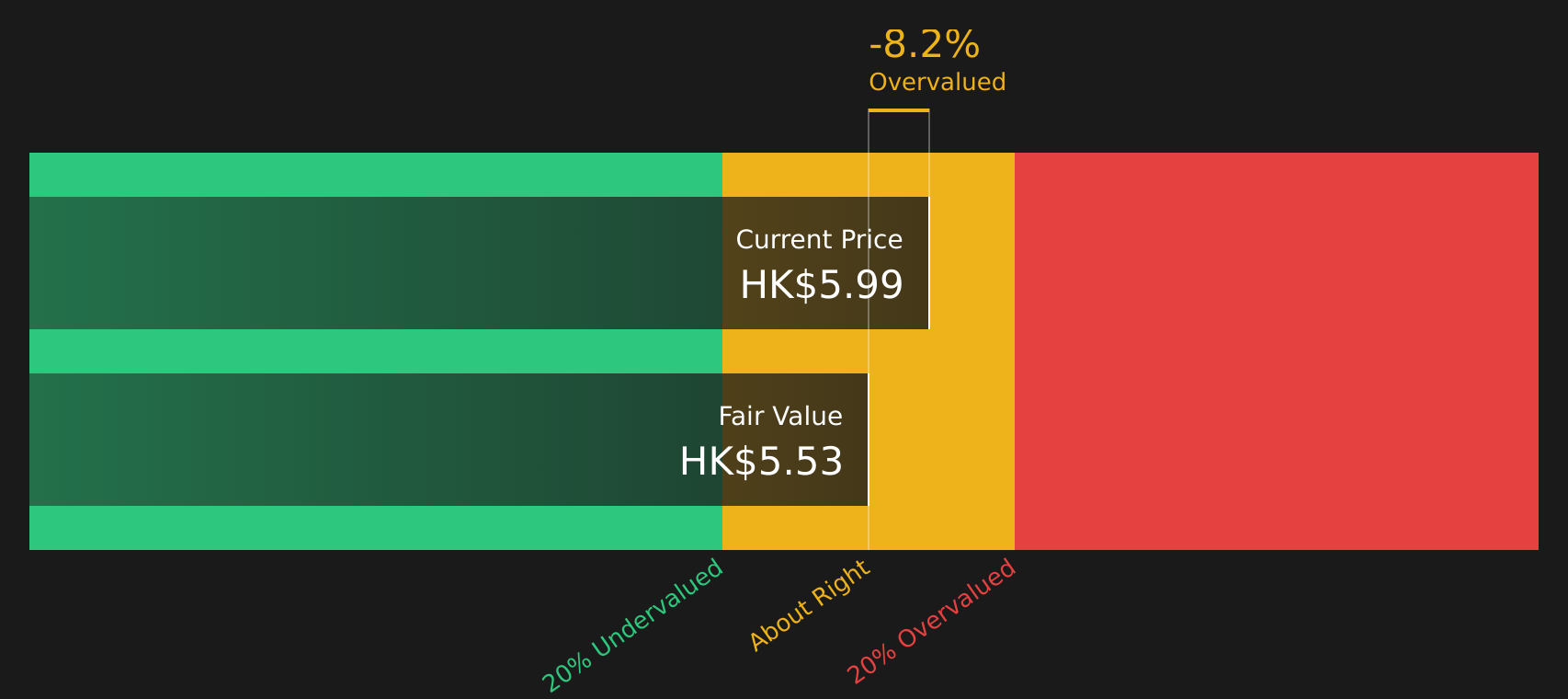

The SWS DCF model points in the same direction as the high 31.2x P/E. At HK$5.99, Hongkong and Shanghai Hotels trades above the model’s estimate of future cash flow value at HK$5.53, suggesting limited margin of safety if cash generation does not build as expected.

For a closer look at how this cash flow view is built and how sensitive it is to the inputs, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hongkong and Shanghai Hotels for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 216 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

Given the mixed signals around value and sentiment, it makes sense to look under the hood yourself and move while the information is fresh. To see both sides of the story in one place, review the 1 key reward and 1 important warning sign

Looking for more investment ideas?

If you stop here, you only see one piece of the puzzle. Use the screener to quickly surface fresh candidates that might suit your style and risk comfort.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hongkong and Shanghai Hotels might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com