Hong Kong IPO activity surged in 2025, with the HKEX ranking first globally for funds raised and new listings driven overwhelmingly by Mainland Chinese companies in technology and biotech sectors. Companies considering a primary or secondary listing should factor in cross-border structuring, dual compliance requirements, and ongoing corporate governance obligations from the outset.

The Hong Kong Stock Exchange (HKEX) roared back to life in 2025, breaking its previous record for market turnover set in 2021 and reaching an all-time high number of listed companies.

Following a protracted post-pandemic slump, the HKEX has resurged to rank first among global stock exchanges for IPO funds raised, which soared 233 percent year-on-year to reach US$37.4 billion in 2025.

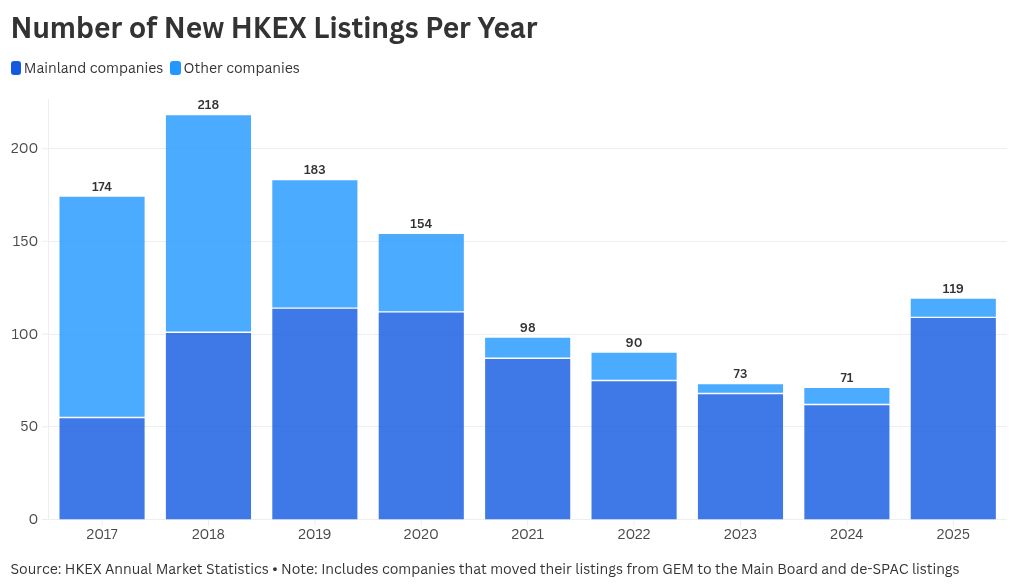

The number of new listings on the HKEX GEM and the Main Board reversed a year-on-year decline dating back to 2018, with a total of 119 companies going public in 2025, up from just 71 the previous year.

New Mainland listings were the main driver of this rise. While Mainland companies (including H-share and non-H-share companies) represented 58 percent of all listed companies on the HKEX, they accounted for 92 percent of all new listings in 2025.

Looking at broad industry categories, pharmaceuticals and biotechnology were the largest sector categories for new listings in 2025, with a total of 22 companies – 13 in biotech companies and eight in pharmaceuticals. The number of digital solution services and industrial engineering companies was also substantial, including several companies in battery storage, electronic equipment, and heavy industrial machinery.

Is your company considering a Hong Kong listing?

Ascentium provides cross-border structuring, dual compliance, and end-to-end corporate services to support high-growth tech and biotech companies with listing readiness and scaling.

What is driving the IPO boom?

A combination of market factors, external pressures, and an explicit endorsement from Beijing have made the HKEX a compelling choice for Mainland companies, in particular those in technology sectors seeking access to international capital.

One of the allures is the huge influx of capital from Mainland investors through the Southbound Stock Connect, which is becoming an increasingly important stream of capital for the market. In 2025, the average daily turnover of the Southbound Stock Connect more than doubled from 2024 to reach HKD 121.1 billion (US$15.46 billion), with activity concentrated in technology and digital sectors.

In addition, an increasingly hostile environment for Chinese companies on American stock exchanges is leading many to think twice about a US-based listing. Threats of delistings of Chinese stocks from under the Holding Foreign Companies Accountable Act (HFCAA) are leading some US-listed Chinese companies to seek a dual listing in Hong Kong while driving others to choose the HKEX over the NASDAQ or NYSE.

Companies pursuing a dual listing face a distinct set of requirements beyond a standard IPO. Structuring must account for the rules of both the HKEX and the home exchange, and companies must meet ongoing compliance obligations, including disclosure, audit, and reporting mandates. Coordinating between Mainland operations and a Hong Kong listing vehicle also adds operational complexity that companies should factor in early in the process. – Leonard Ler, Executive Director of Group Commercial at Ascentium

Beijing has also given its blessing to Chinese companies to list on the HKEX. In April 2024, the China Securities Regulatory Commission (CSRC) approved five new measures to enhance capital market cooperation between the Chinese Mainland and Hong Kong, which, among other things, called for supporting “leading Mainland companies to list in Hong Kong”. While this is not a specific policy initiative, the political support conveyed by this statement will provide additional incentive to Mainland companies to consider the HKEX over other possible exchanges.

A bright outlook for Mainland tech in Hong Kong

While the number of new listings in 2025 remained considerably below the record of 218 set in 2018, there are strong indicators that the trajectory will continue upward. As of April 30, 2026, there were a total of 475 equity listing applications under processing for HKEX GEM and the Main Board. A further 50 had already been listed as of May, and 20 had been approved pending listing.

Find Business Support

Moreover, the number of Mainland Chinese companies that listed in 2025 was only five fewer than in 2018.

The DeepSeek-driven AI rally and strong investor appetite for tech stocks among both Chinese and international investors is likely to continue generating significant funding opportunities for Chinese tech companies considering a primary or secondary listing in Hong Kong. Companies across both upstream segments – infrastructure and development support – as well as downstream consumer and enterprise-facing applications, will be a strong draw for investors in the near term.

The makeup of the 50 companies that have already listed in 2026 supports this view. Nine semiconductor companies have already listed this year, as well as a further nine software and digital solutions services companies. There have also been several listings in the consumer telecom and electronic components space.

The striking of the gong is only the start of a company’s HKEX journey. Listed companies must meet periodic disclosure requirements, manage connected and notifiable transactions, and maintain their corporate structure on an ongoing basis, all of which require continuous legal and corporate advisory support. Shareholder communication and corporate action management add to operational demands, particularly for companies with a large number of Southbound investors. As the business scales, compliance burdens will continue to grow. – Leonard Ler, Executive Director of Group Commercial at Ascentium

It is evident from both the 2025 and 2026 listings that the HKEX is becoming an increasingly attractive funding stream for Chinese technology companies.

For Mainland Chinese companies considering a primary or secondary Hong Kong listing, the process will start with the question of structuring. Mainland-incorporated companies face a different set of structural considerations than those with offshore incorporation, while companies conducting a secondary listing are required to comply with dual listing rules, which can create additional complications.

Once listed, companies will also need to comply with ongoing reporting and audit requirements, including periodic disclosure requirements, connected and notifiable transaction advice, and the ongoing maintenance of the corporate structure, all of which require sustained legal and corporate advisory support.

Considering a listing on the HKEX? Understand the full picture before you start.

Structuring decisions for Mainland and offshore listing vehicles require careful cross-border legal and corporate advisory. Secondary listings add a further layer of complexity, requiring compliance with both HKEX rules and home-market obligations. Once listed, companies face ongoing challenges from disclosure obligations, connected transaction governance, and managing shareholder records, all while continuing to scale.

Ascentium provides integrated support across every stage of the process, covering incorporation and cross-border structuring for both Mainland and offshore companies, GRC and audit services for dual-listed firms, company secretarial and compliance monitoring, professional share registry and investor communication, and technology-driven corporate services and HR/payroll solutions built for listed companies operating across APAC.

Our Business Advisory service supports companies in establishing and growing their presence in Hong Kong, Asia’s leading international business and financial hub. We provide advice on corporate structuring, company formation, due diligence, commercial and employment contracts, intellectual property protection, and M&A transactions, helping businesses navigate Hong Kong’s regulatory environment and leverage its role as a gateway to the Chinese Mainland and the wider Asia?Pacific region.

Manager

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.