Shares of Bristol Myers Squibb (BMY +0.39%) are trading in a manner that evokes little confidence in the company’s future growth.

The numbers suggest otherwise. At roughly 10 times forward earnings, the drug manufacturer’s stock is the cheapest among its 11 peers in the S&P 500. The measly 8% stock returns this year so far have pushed the dividend yield above 4%, the second-highest in this cohort of pharmaceuticals, trailing only Pfizer.

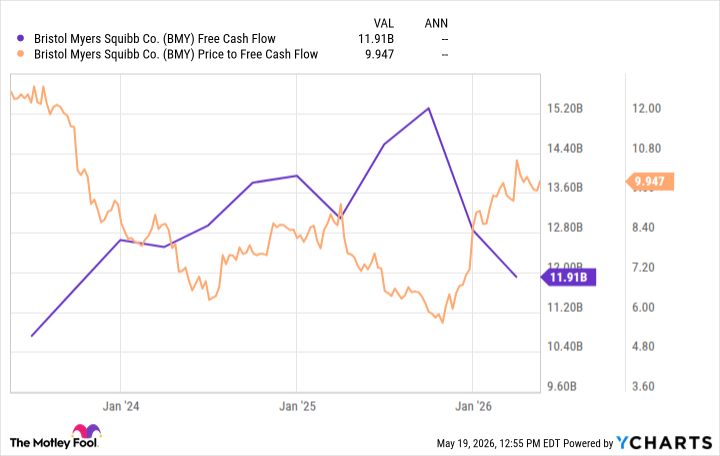

But here’s the kicker: at just 9.9 times trailing free cash flow (FCF), Bristol Myers Squibb is the third-cheapest of the 59 healthcare stocks in the S&P 500. That’s an unusually low valuation for a pharmaceutical company expected to generate roughly $46 billion to $47.5 billion in revenue this year.

Of course, it’s not the numbers that concern the market. It’s patent expirations.

A business heading toward long-term decline?

Major drugs, including Revlimid and eventually Eliquis, face increasing generic competition over the next several years. This has likely led investors to treat Bristol Myers Squibb as a business heading toward long-term revenue decline.

Image source: Getty Images.

But recent results show the company’s newer products are already starting to offset those losses, or the fear of losses.

In the first quarter of 2026, BMS generated $11.5 billion in revenue, up 3% year over year. The company’s growth portfolio increased 12% to $6.2 billion and now accounts for more than half of total revenue. Several newer drugs are growing rapidly, including Breyanzi, whose revenue jumped 56% year over year; Camzyos, which has surged 97%; and Reblozyl, which has increased 16%.

Meanwhile, Eliquis, the company’s massive blood thinner franchise developed alongside Pfizer, continues performing quite well. It generated $4.14 billion in Q1 revenue alone, up 16% year over year. BMS recently projected that Eliquis revenue could still rise another 10% to 15% during 2026, despite pricing pressure tied to Medicare negotiations.

An extra $2 billion

The company is also becoming significantly more aggressive on cost controls. Management says restructuring efforts and productivity initiatives are expected to generate roughly $2 billion in annual cost savings by 2027.

Today’s Change

(0.39%) $0.23

Current Price

$58.54

Key Data Points

Market Cap

$120B

Day’s Range

$58.11 – $59.21

52wk Range

$42.52 – $62.89

Volume

5K

Avg Vol

12M

Gross Margin

66.07%

Dividend Yield

4.27%

At the same time, Bristol Myers Squibb still has one of the deeper pipelines in large-cap pharma. It currently has multiple late-stage oncology, immunology, and cardiovascular programs moving through pivotal trials. Management highlighted several major regulatory and clinical catalysts expected throughout 2026, including iberdomide, mezigdomide, and additional expansion opportunities for Camzyos.

Still, this is not a “no-risk” pharmaceutical stock. Patent cliffs are real. Revlimid revenue continues to decline due to generic competition, and Eliquis will eventually face major exclusivity pressure later this decade.

But the valuation already reflects much of that pessimism, especially on a price-to-FCF basis, despite free cash flow itself not being too unfavorable.

BMY Free Cash Flow data by YCharts.

A company that should generate $46 billion to $47.5 billion in annual revenue, offers a dividend yield of more than 4%, and has a growing, newer drug franchise typically doesn’t trade at around 10 times forward earnings or FCF, unless the market is being short-sighted.

Right now, Bristol Myers Squibb appears to be priced for stagnation. But if management can continue growing its newer portfolio while stabilizing legacy declines, today’s valuation could eventually look far too low.