Find winning stocks in any market cycle. Join 7 million investors using Simply Wall St’s investing ideas for FREE.

Centurium Capital, the controlling shareholder of Luckin Coffee (OTCPK:LKNC.Y), has agreed to acquire Blue Bottle Coffee from Nestle.

The deal brings a premium, globally recognized specialty coffee brand under the same investment umbrella as Luckin Coffee.

Centurium has indicated it does not plan to integrate Luckin and Blue Bottle, pointing to a multi brand approach.

For you as an investor, this sits at the intersection of China’s fast growing coffee market and the premium specialty segment that Blue Bottle targets. Luckin Coffee operates a large tech enabled retail coffee network in China, while Blue Bottle is known for its higher end cafes and packaged coffee in markets such as the US and parts of Asia. Keeping the brands separate gives Centurium flexibility to address different consumer segments without forcing a single global format.

Looking ahead, a key consideration is how Centurium might use its ownership links, for example in sourcing, digital know how or store rollout expertise, without merging the brands. Any moves to expand Blue Bottle in Asia or bring Luckin concepts closer to global premium standards could influence how investors evaluate OTCPK:LKNC.Y’s long term addressable market and its competitive position relative to global chains such as Starbucks.

Stay updated on the most important news stories for Luckin Coffee by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Luckin Coffee.

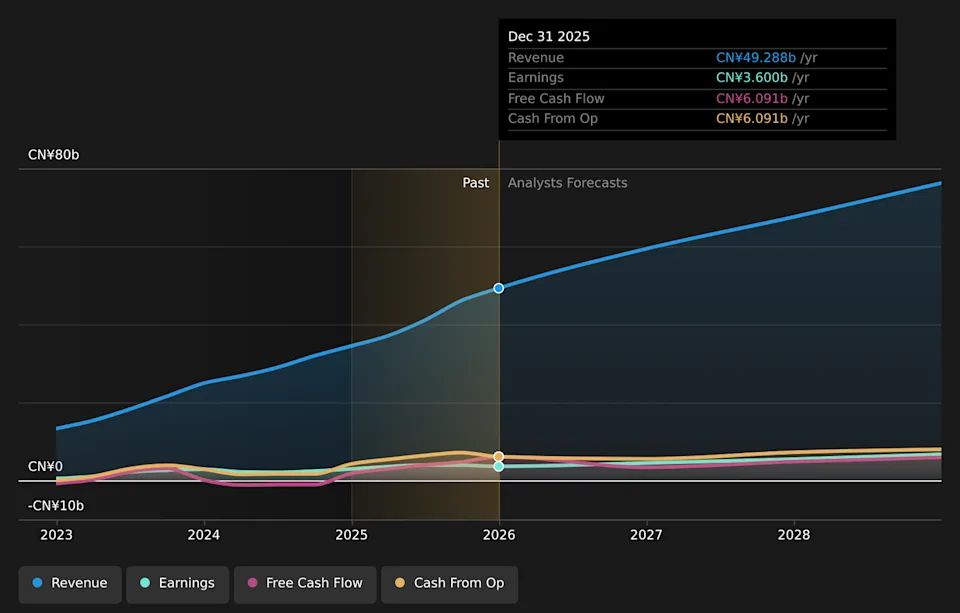

OTCPK:LKNC.Y Earnings & Revenue Growth as at Mar 2026

This move by Centurium effectively puts a mass-market, app-first China operator and a premium, cafe-centric U.S. brand under the same capital owner. For you, the question is less about immediate financial impact and more about optionality. Luckin has just reported full year 2025 revenue of CNY 49,288.1m and net income of CNY 3,600.38m, so any cross-brand projects would be building on a sizable existing operation. Access to Blue Bottle’s know-how in higher priced specialty coffee and overseas retail formats could, over time, inform how Luckin refines its Origin Flagship concept, menu mix, and store design in China and abroad. At the same time, Centurium has stated it does not plan to integrate the two, so you may want to think of this as a portfolio move rather than a direct expansion of Luckin’s financial footprint. Competitive context also matters, since global rivals such as Starbucks and Tim Hortons already operate across price tiers and regions. How Centurium balances investment between a fast growing, tech enabled China network and a smaller premium chain will influence how you weigh Luckin’s long term role in the global coffee industry.

The acquisition lines up with the narrative around Luckin’s focus on professionalism, quality, and origin focused concepts, because Blue Bottle’s specialty credentials could support Luckin’s higher end store formats over time.

There is a potential tension with the narrative that highlights margin improvement from operational efficiencies, since any push toward more premium, experience heavy formats could carry higher per store costs.

The original narrative concentrates on China focused store expansion and digital growth, while Centurium’s ownership of Blue Bottle introduces an additional lever in international specialty coffee that is not fully covered.

⚠️ Centurium may need to allocate capital and management attention between Luckin and Blue Bottle, which could slow execution on Luckin’s fast store rollout if resources become stretched.

⚠️ Expanding influence beyond China brings Luckin closer to heavyweight competitors like Starbucks and Tim Hortons, raising the bar for brand, quality, and compliance in unfamiliar markets.

🎁 Having access to a premium, globally recognized specialty brand gives Centurium and, indirectly, Luckin more ways to learn from higher end customer preferences and product development.

🎁 If Centurium identifies operational learnings or sourcing efficiencies across the two businesses, Luckin could benefit from better product offerings or more efficient supply chains over time.

From here, you may want to watch for any reference by Luckin management to collaboration with Blue Bottle, even if the brands stay separate. That includes changes in Luckin’s premium product lineup, store concepts, or sourcing that echo Blue Bottle’s specialty approach. Updates on overseas store counts, especially in the U.S. and broader Asia, can also help you assess whether Luckin is quietly building a more global footprint. Finally, keep an eye on profitability metrics after a year in which Luckin reported CNY 3,600.38m of net income on CNY 49,288.1m of revenue, to see whether the company continues to balance growth investments with earnings as Centurium’s coffee portfolio evolves.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Luckin Coffee, head to the community page for Luckin Coffee to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LKNCY.