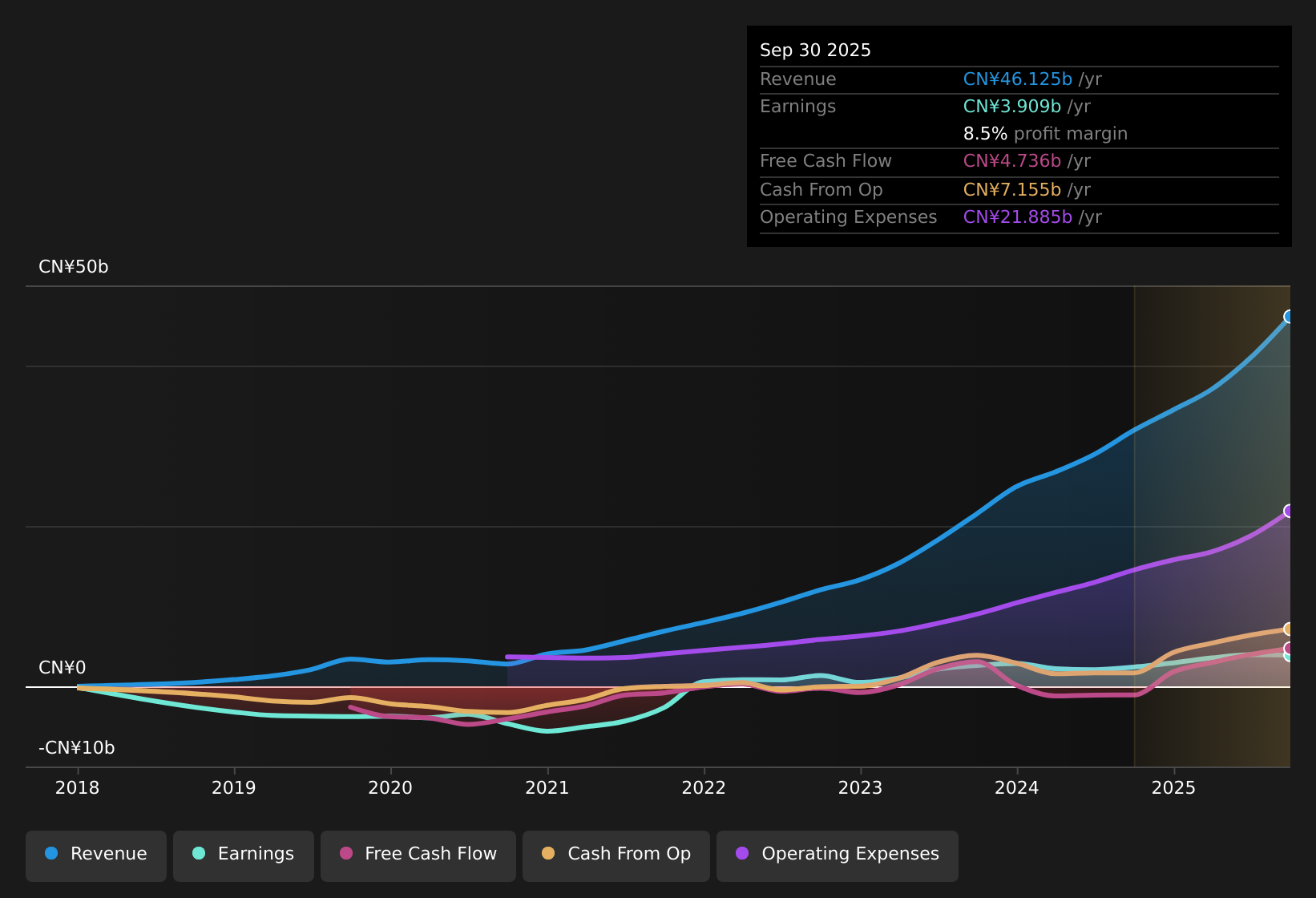

Luckin Coffee (OTCPK:LKNC.Y) has wrapped up FY 2025 with fourth quarter revenue of about C¥12.8b and basic EPS of C¥1.62, rounding out a year in which trailing twelve month revenue reached roughly C¥49.3b and EPS came in at about C¥11.23. The company has seen quarterly revenue move from roughly C¥9.6b in Q4 2024 to C¥12.8b in Q4 2025, while basic EPS shifted from C¥2.64 to C¥1.62 over the same period, setting up a mixed picture that investors will likely weigh against the reported net income of C¥518.19m this quarter and C¥3.6b over the last twelve months. Overall, the latest numbers point to solid scale with margins that investors will be watching closely as the growth story evolves.

See our full analysis for Luckin Coffee.

With the headline figures on the table, the next step is to see how these results line up with the widely shared growth and profitability narratives around Luckin Coffee, and where the numbers might be telling a different story.

See what the community is saying about Luckin Coffee

Revenue Near C¥49.3b, With Momentum And Moderation

- On a trailing twelve month basis, Luckin Coffee generated about C¥49.3b in revenue and C¥3.6b in net income, with earnings up 22.8% over the past year and revenue growth presented at roughly 13.4% a year.

- Consensus narrative points to expanding store presence and app driven engagement as key revenue engines, and the data lines up with that view by showing TTM revenue moving from C¥34.5b in 2024 Q4 to C¥49.3b in 2025 Q4. However, the 22.8% earnings growth rate is lower than the five year average of 63.2% a year, which keeps expectations for future growth in check rather than suggesting the past pace continues unchanged.

- Supporters of the bullish story highlight store expansion and digital channels as drivers of recurring sales, and the step up in TTM revenue from C¥37.1b in 2025 Q1 to C¥49.3b in 2025 Q4 is consistent with that emphasis on scale.

- At the same time, the slower 22.8% one year earnings growth compared with the much higher five year average shows the growth profile in the data is already more measured than the longer term narrative might imply.

Have a look at how other investors are framing this balance between growth and scale in the community view on Luckin Coffee: 📊 Read the what the Community is saying about Luckin Coffee.

Margins At 7.3% While Costs Stay In Focus

- Over the last 12 months, Luckin Coffee reported a net profit margin of 7.3%, compared with 8.5% in the prior year, on TTM net income of about C¥3.6b.

- Critics in the consensus narrative flag aggressive store growth, delivery dependence and rising costs as margin risks, and the data offers some support for that cautious tone, with quarterly net income at C¥518 million in 2025 Q4 versus C¥841 million in 2024 Q4 and TTM margin moving from 8.5% to 7.3%. This shows that even with higher scale, profitability has not kept pace with revenue in the same way.

- Bears often point to mounting delivery and expansion expenses, and the recent TTM net income path of C¥3.9b in 2025 Q3 to C¥3.6b in 2025 Q4 lines up with the idea that extra costs can absorb some of the benefit from higher sales.

- At the same time, the company remains profitable with C¥3.6b of TTM net income, so the numbers indicate pressure on margins rather than a break into losses, which is an important distinction for long term investors watching cost trends.

P/E Of 22x And Price Below DCF Value

- Luckin Coffee is trading at a P/E of about 22x with a share price near US$36.07, compared with a DCF fair value of roughly US$41.64 and a highlighted analyst price target of US$48.76, while the P/E also sits modestly below the US Hospitality industry average of 23.2x and well below the peer average of 76.3x.

- Supporters of the bullish case point to growth plus valuation support, and the figures here give them some material talking points, because earnings are reported to have grown 22.8% over the past year with revenue growth expectations of about 13.4% a year. Yet the current price is about 13% below the DCF fair value and well under the US$48.76 analyst target, which suggests that the multiples in the data are not stretched relative to the earnings profile being discussed.

- Consensus commentary also highlights analysts implying roughly 35.2% upside, and while investors should treat any target cautiously, the gap between the US$36.07 price and the US$48.76 target shows why some see room for re rating if growth holds near current forecasts.

- Against that, the same dataset shows net margin at 7.3% versus 8.5% last year and one year earnings growth below the five year average, so the valuation support is paired

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Luckin Coffee on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

If the mix of growth, margins and valuation here feels finely balanced, act while the details are fresh and weigh the trade offs yourself. To see what investors are currently optimistic about, take a closer look at the 5 key rewards and decide how those positives fit into your own view.

See What Else Is Out There

Luckin Coffee is showing pressure on margins and earnings growth, with net profit margin moving from 8.5% to 7.3% and yearly earnings growth below its longer term pace.

If that mix of thinning margins and uneven earnings makes you want a steadier profile, you may want to look at 80 resilient stocks with low risk scores to quickly review companies where overall risk scores screen more conservatively.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com