800V Silicon Carbide Inverters for EV Market Size

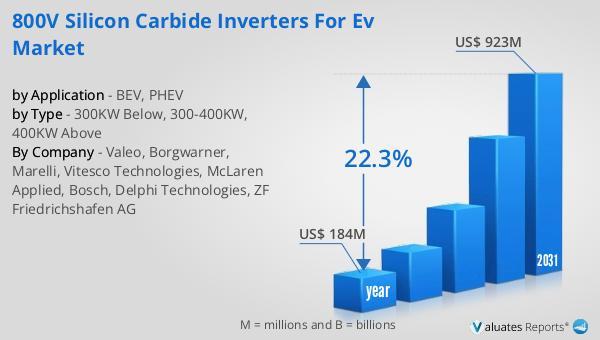

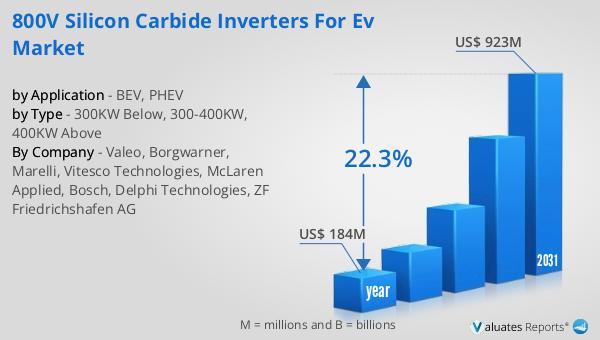

The global market for 800V Silicon Carbide Inverters for EV was valued at US$ 184 million in the year 2024 and is projected to reach a revised size of US$ 923 million by 2031, growing at a CAGR of 22.3% during the forecast period.

View sample report

https://reports.valuates.com/request/sample/QYRE-Auto-14P19290/Global_800V_Silicon_Carbide_Inverters_for_EV_Market_Research_Report_2025

The global 800V Silicon Carbide Inverters for EV market is experiencing rapid market growth as automotive manufacturers accelerate the transition toward high-voltage electric vehicle architectures designed to improve charging performance, driving efficiency, and overall powertrain capability. Silicon carbide inverters are critical components within electric vehicle propulsion systems because they convert direct current from the battery into alternating current for electric motors while enabling higher efficiency, reduced energy loss, and superior thermal performance compared to conventional silicon-based technologies. Rising demand for long-range battery electric vehicles, ultra-fast charging infrastructure, and advanced electric mobility platforms is significantly influencing market size and long-term market forecast trends. One of the most important market trends shaping the industry is the growing adoption of next-generation high-voltage vehicle platforms that support faster charging times, lighter vehicle designs, and enhanced powertrain efficiency. Automakers are increasingly integrating silicon carbide semiconductor technologies into electric vehicle architectures to reduce switching losses, improve power density, and optimize energy management systems. The expansion of premium electric vehicle production, increasing investments in high-performance mobility technologies, and growing government support for clean transportation are further strengthening market growth globally. In addition, rising emphasis on energy efficiency, battery optimization, and sustainable transportation systems is accelerating adoption of advanced silicon carbide inverter technologies across passenger and commercial electric vehicle platforms. Manufacturers are heavily investing in power electronics innovation, thermal management systems, and integrated electric drive technologies to strengthen their market share and support evolving electric mobility requirements.

Based on type segmentation, the 300KW Below segment currently holds the largest market share because this power category is widely utilized across mainstream battery electric vehicles and high-volume electric passenger vehicle platforms. Automotive manufacturers increasingly adopt silicon carbide inverters within this range because they provide an effective balance between performance, efficiency, cost optimization, and compact system integration. The growing adoption of mid-range electric vehicles and increasing demand for efficient urban mobility solutions continue driving strong market growth within this segment. Automakers are focusing on improving inverter efficiency, reducing energy losses, and enhancing thermal performance to support longer driving range and improved charging capability. At the same time, the 300-400KW segment is experiencing rapid market expansion due to rising demand for high-performance electric vehicles, premium electric SUVs, and advanced electric mobility platforms requiring enhanced acceleration and higher power output. The increasing popularity of performance-oriented electric vehicles and luxury EV platforms is significantly influencing broader market trends within this segment. The 400KW Above category is also gaining increasing attention because ultra-high-performance electric sports cars, commercial electric mobility platforms, and advanced high-speed electric transportation systems require extremely high-power silicon carbide inverter technologies capable of supporting advanced propulsion demands. Manufacturers are increasingly investing in next-generation power modules, advanced cooling systems, and integrated power electronics platforms to support these emerging applications. As electric vehicle architectures continue evolving toward higher voltage systems and greater efficiency, the overall market forecast for all major power categories remains highly favorable.

From an application perspective, the BEV segment currently accounts for the largest market share due to the rapid global expansion of battery electric vehicle adoption and increasing investments in dedicated electric mobility platforms. Battery electric vehicles rely heavily on advanced silicon carbide inverter technologies to maximize energy efficiency, optimize battery utilization, and support fast-charging capability within high-voltage electric propulsion systems. The growing demand for longer driving range, improved charging convenience, and sustainable transportation solutions is significantly contributing to market growth within this segment. Automakers are increasingly adopting 800V architectures within battery electric vehicles because these systems enable faster charging speeds, lighter wiring infrastructure, reduced thermal losses, and improved vehicle performance. The PHEV segment is also witnessing strong market growth as hybrid electric vehicle manufacturers integrate advanced power electronics technologies to improve efficiency and support smoother transitions between electric and combustion power systems. Plug-in hybrid vehicles increasingly require compact and highly efficient inverter systems capable of optimizing energy management while maintaining flexible driving performance. The growing transition toward electrified transportation and tightening global emission regulations are strengthening broader market trends across both BEV and PHEV applications. As governments continue promoting clean mobility initiatives and consumers increasingly adopt electric transportation technologies, the market forecast for silicon carbide inverter applications remains highly optimistic.

The competitive landscape of the 800V Silicon Carbide Inverters for EV market is characterized by aggressive technological innovation, strategic partnerships with automakers, and increasing investments in advanced electric powertrain technologies. Bosch remains one of the companies with the largest market share due to its strong expertise in automotive electronics, electric mobility systems, and powertrain engineering technologies supporting next-generation electric vehicle platforms. The company continues strengthening its position through development of highly efficient silicon carbide inverter systems integrated with advanced thermal management and electric drive solutions. BorgWarner also maintains a significant market presence because of its extensive electrification portfolio and advanced inverter technologies supporting high-performance battery electric vehicle applications. Valeo continues contributing strongly to market growth through integrated electric propulsion systems and power electronics solutions designed for efficient and scalable electric mobility platforms. Vitesco Technologies is increasingly recognized for its strong focus on electrified powertrain technologies, silicon carbide power modules, and advanced inverter systems supporting high-voltage electric vehicle architectures. Marelli maintains a growing market position through innovative electric drive technologies and integrated power electronics platforms developed for global automotive manufacturers. ZF Friedrichshafen AG continues expanding its market share through advanced electric axle systems, inverter technologies, and integrated e-mobility solutions supporting both passenger and commercial electric vehicles. Delphi Technologies remains an important participant because of its expertise in automotive electrification systems and advanced vehicle electronics technologies. McLaren Applied is gaining market attention through high-performance electric propulsion technologies and advanced power electronics solutions developed for premium and motorsport-inspired electric vehicle applications. Industry competition is expected to intensify further as companies focus on next-generation silicon carbide semiconductor integration, compact inverter design, advanced cooling technologies, software-defined power management systems, and high-efficiency electric propulsion architectures supporting future mobility ecosystems.

Regionally, Asia-Pacific currently dominates the 800V Silicon Carbide Inverters for EV market in terms of market share due to the region’s strong electric vehicle manufacturing ecosystem, large-scale battery production infrastructure, and aggressive investments in advanced mobility technologies across China, Japan, South Korea, and Taiwan. China remains one of the largest contributors to market growth because of its dominant electric vehicle production capacity, government incentives supporting electric mobility adoption, and rapid expansion of fast-charging infrastructure. The country’s growing investments in silicon carbide semiconductor manufacturing and high-voltage EV technologies continue driving substantial demand for advanced inverter systems. Japan and South Korea maintain strong positions within the market because of their leadership in automotive electrification, advanced semiconductor engineering, and high-performance battery technologies. Europe also represents a major market supported by strict emission regulations, rapid electric vehicle adoption, and increasing investments in premium electric mobility platforms across Germany, France, the United Kingdom, Italy, and other automotive manufacturing hubs. North America continues experiencing steady market growth due to expanding electric vehicle production, increasing charging infrastructure development, and rising consumer demand for long-range battery electric vehicles across the United States and Canada. Southeast Asia, particularly India, is emerging as a developing market because of growing government support for electric mobility, expanding automotive manufacturing infrastructure, and increasing adoption of electrified transportation systems. Latin America is also gradually increasing market participation through electric vehicle pilot programs and sustainable transportation initiatives across Mexico and Brazil. The overall market forecast for the 800V Silicon Carbide Inverters for EV market remains highly positive as automakers continue accelerating investments in electric mobility, high-voltage vehicle architectures, and advanced semiconductor technologies. Future market trends are expected to focus on ultra-fast charging compatibility, integrated electric drive platforms, advanced thermal management systems, intelligent power electronics, and expansion of silicon carbide semiconductor production capabilities that will continue driving long-term market growth globally.

by Type

• 300KW Below

• 300-400KW

• 400KW Above

by Application

• BEV

• PHEV

By Company

Valeo, Borgwarner, Marelli, Vitesco Technologies, McLaren Applied, Bosch, Delphi Technologies, ZF Friedrichshafen AG

View full report

https://reports.valuates.com/market-reports/QYRE-Auto-14P19290/global-800v-silicon-carbide-inverters-for-ev

Valuates,

4th Floor,

Balaraj’s Arcade,

Whitefield Main road,

Bangalore 560066,

Valuates offers an extensive collection of market research reports that helps companies to take intelligent strategical decisions based on current and forecasted Market trends.

This release was published on openPR.