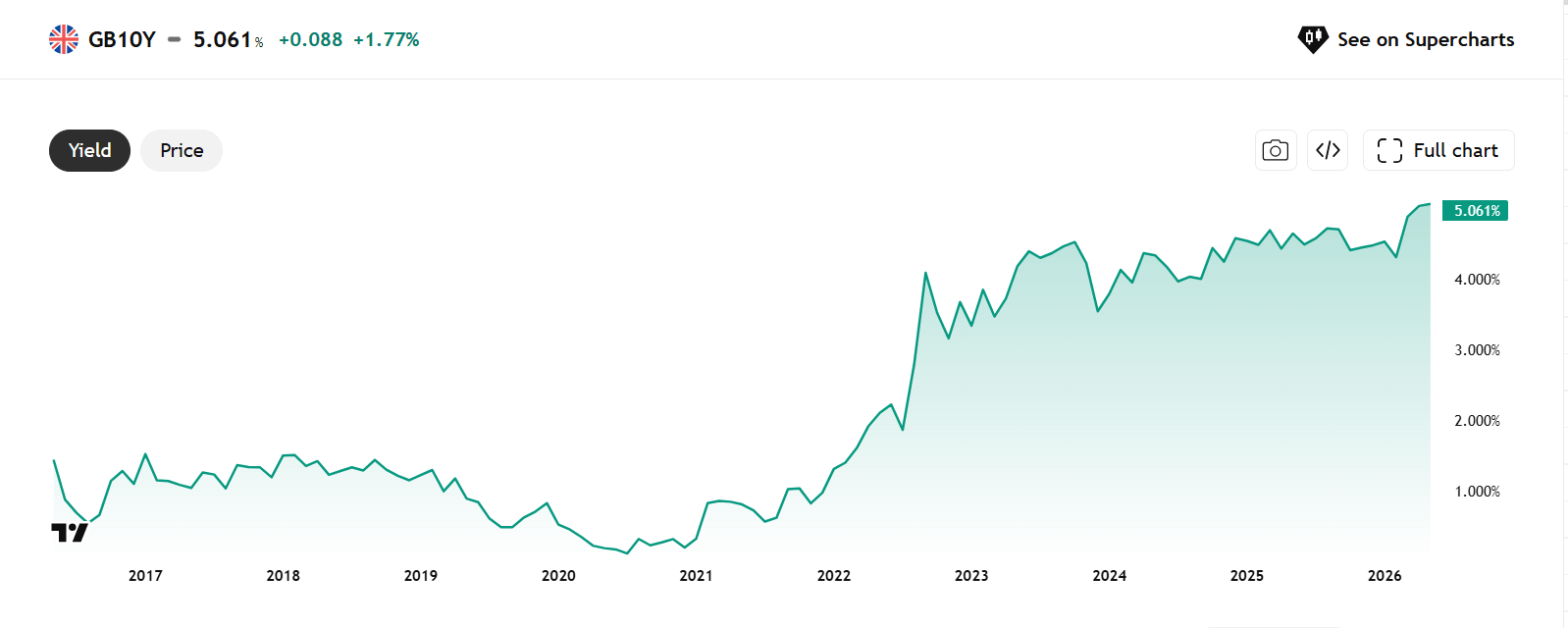

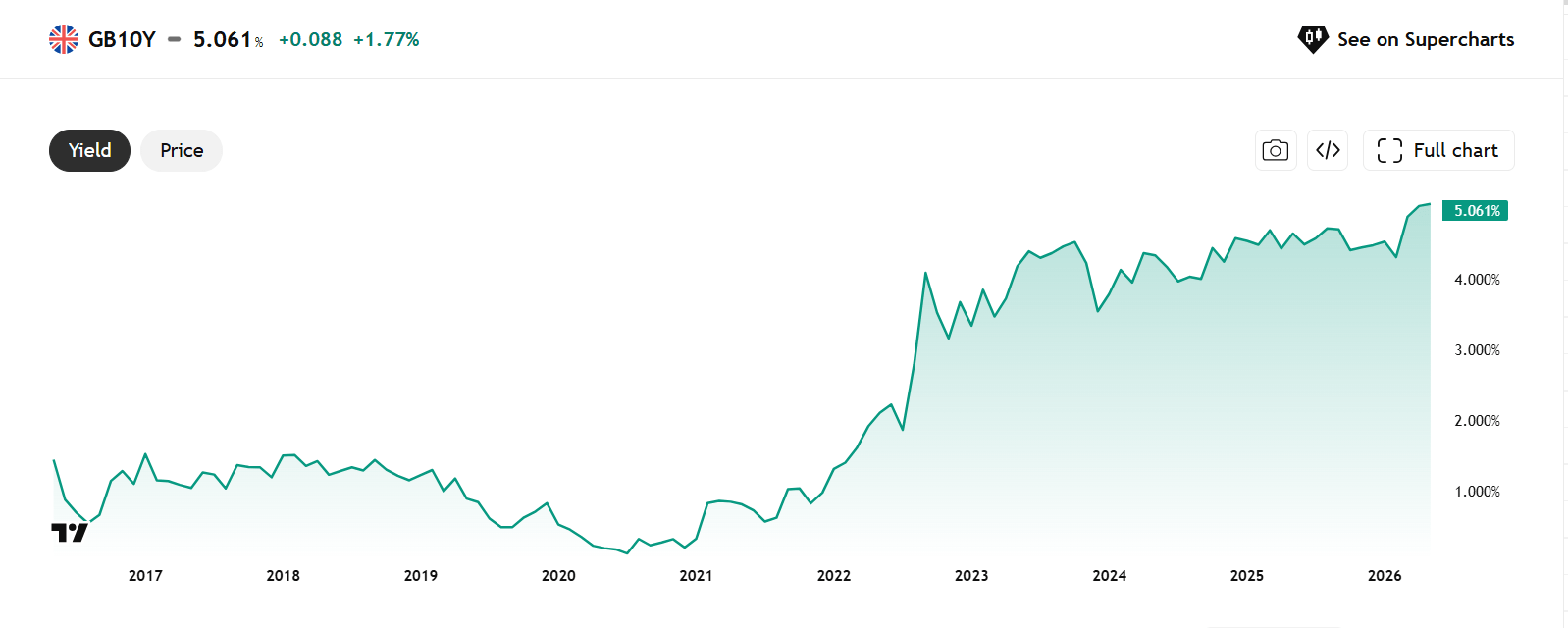

Ahead of this Thursday’s local elections across the UK, Gilt yields are rising sharply. On Tuesday, the 30-year Gilt yield rose to its highest level since 1998, at one point it was above 5.8%, before settling at 5.74%, a rise of 8bps on the day. There was a similar rise in 10-year yields, as UK bonds sold off across the curve. What made Tuesday’s sell off particularly worrying was that it happened in isolation. There was no major sell off in bond markets in the US or Europe, and UK yields also decoupled from the oil price, UK yields rose even as the price of crude oil fell.

This suggests that something else is triggering this sell off, which explains why UK yields are getting targeted more than the their peers, as you can see below. Typically, when you see bond yields decouple from their peers it is a sign of rising local risk premium, such as a credibility issue and/ or a potential funding crisis. This time, it is also a sign of a rising political risk premium getting added to UK yields.

Chart 1: UK 10-year bond yield

Source: XTB

The elections on Thursday, while they do not change the picture at Westminster, are the UK’s version of the US mid-terms, and they will be important to gauge sentiment towards the UK’s traditional two party political system. Labour and the Conservatives are expected to see big losses this week to Reform, the Liberal Democrats and the Greens. There are fears that Labour could lose two thirds of their council seats, and the Conservatives could lose half. With a debt to GDP ratio of more than 93%, a patchy economic record, soaring debt interest costs and an energy price spike to deal with, the prospect of a splintered political body and a potential hung parliament in 2029’s general election, fears could grow about how current and future governments can solve the economic and fiscal issues facing the UK.

These elections could also trigger a near-term political crisis for the UK. If Labour perform as badly as expected, then there could be growing calls for Kier Starmer to step aside, along with Chancellor Rachel Reeves. The rise in bond yields in recent days suggest that financial markets are not impressed by potential left-leaning replacements like Andy Burnham or Angela Raynor. Fears that they will ditch Reeves’ fiscal rules and boost spending are already triggering capital flight out of UK bonds, especially at the long end, where fears about debt sustainability tend to fester. The pound is also at a crossroads, after outperforming its G10 peers in March and April, May is proving to be a trickier month for pound bulls.

There are two local elections that are worth watching closely on Thursday night. The outcome of elections in Essex and in Hackney could gauge whether Reform and the Greens will make big inroads into UK council seats. These two areas are traditionally Conservative and Labour strongholds, respectively. If these are lost, then it could suggest a period of political upheaval ahead for the UK, which may add to the upward pressure on UK yields.

An alternative view, If Labour outperforms, this could be the peak for UK yields

The bond market is pricing in a fractured political landscape, and a potential shift even more to the left for the Labour party on the back of these elections. However, if the showing for Labour is not as bad as expected, then this could be the peak for UK yields and bonds may even stage a recovery at the end of the week. The Greens are facing increasing media scrutiny in the lead up to these elections, we will have to see if this impacts them at the ballot box.

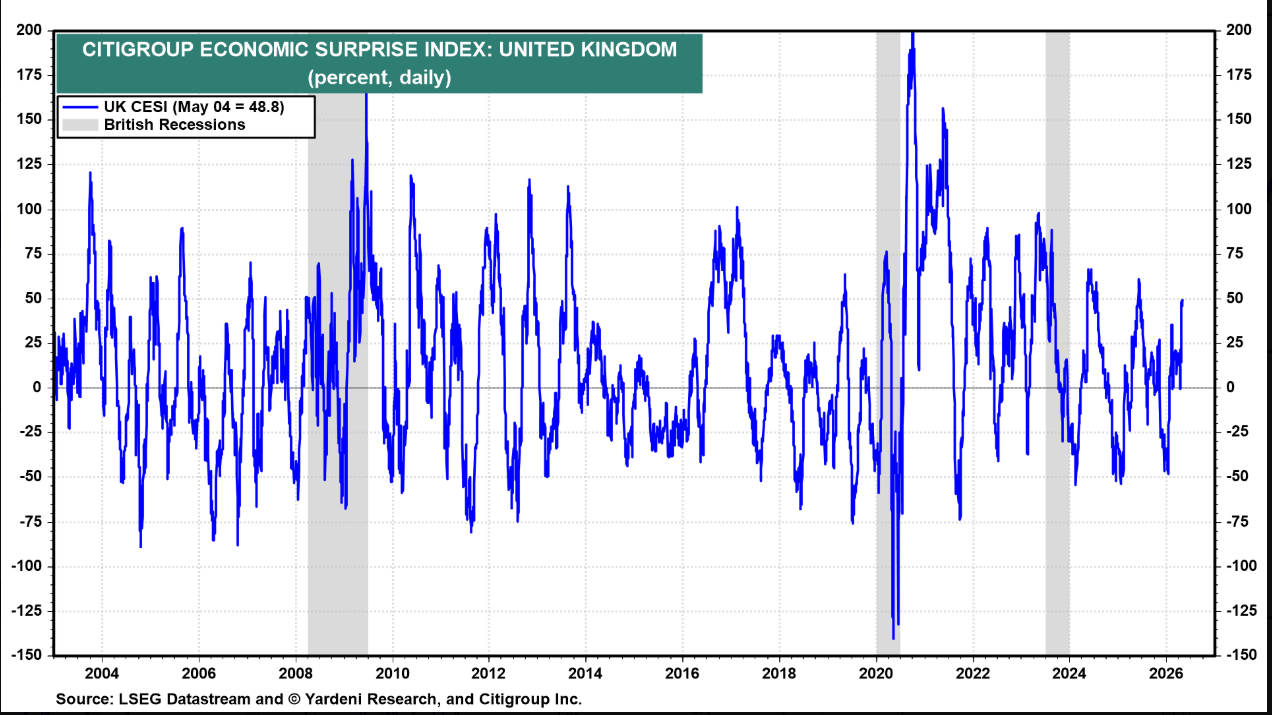

UK’s resilient economy fails to impact bond market

While the ultimate direction for UK yields in the short term will depend on the outcome of Thursday’s elections, it is worth noting that the 23bp increase in 10-year UK Gilt yields in the past month has occurred even though economic data has surprised on the upside this year. April PMIs were stronger than expected, house prices rose unexpectedly in April, and car sales also grew by 24% compared to a year earlier. The NISER Institute predicts growth of 0.6% in Q1, and 0.4% in Q2, which may not be stellar, but would not support the view that the UK is a struggling economy that is drowning in its debt burden. While the UK’s debt pile is a problem, and the government should restrict spending now that the tax burden is growing at the fastest rate in the OECD, the UK’s bond market does appear to be trigger happy in recent months.

Chart 2: Citi UK’s Economic Surprise Index

Source: XTB

Overall, the UK’s bond market is pricing in a hefty risk premium ahead of local elections. However, a stronger performance for the Labour party that silences Kier Starmer’s critics and solidifies his position in 10 Downing Street could trigger a decent reversal in UK yields and a recovery in sentiment towards the UK.

Chart 3: GBP/USD chart 1-year

Source: XTB

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.