- The Hong Kong government recently raised stamp duty on residential properties valued above HK$100,000,000 to 6.5% and outlined plans to bring REITs under mutual-market access while potentially exempting some non-residential property transfers from stamp duty.

- These policy moves could reshape how developers like Hang Lung Properties balance high-end residential exposure with participation in an evolving REIT and commercial property framework.

- We’ll now examine how the higher stamp duty on luxury homes may influence Hang Lung Properties’ investment narrative and future risk-reward balance.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Hang Lung Properties Investment Narrative Recap

To own Hang Lung Properties, you need to be comfortable with a fairly concentrated bet on premium retail and mixed use assets in Greater China, while accepting pressure on earnings and dividends. The new 6.5% stamp duty on ultra high end homes looks peripheral to that core story, so it does not really change the near term focus on weak rental momentum and high gearing as the key risks, or on a gradual recovery in tenant sales as the main catalyst.

The most relevant recent update in this context is the 2025 full year result, which showed sales falling to HK$9,950 million and net income to HK$1,806 million, even as the company maintained a final dividend of HK$0.40 per share. Those numbers highlight how stretched the payout already is given weaker profitability, so any further policy shocks or sector volatility could put more attention on balance sheet resilience and the sustainability of cash returns.

Yet behind the potential upside in premium retail, investors should also be aware of the risk that persistent earnings pressure and a still generous dividend could…

Read the full narrative on Hang Lung Properties (it’s free!)

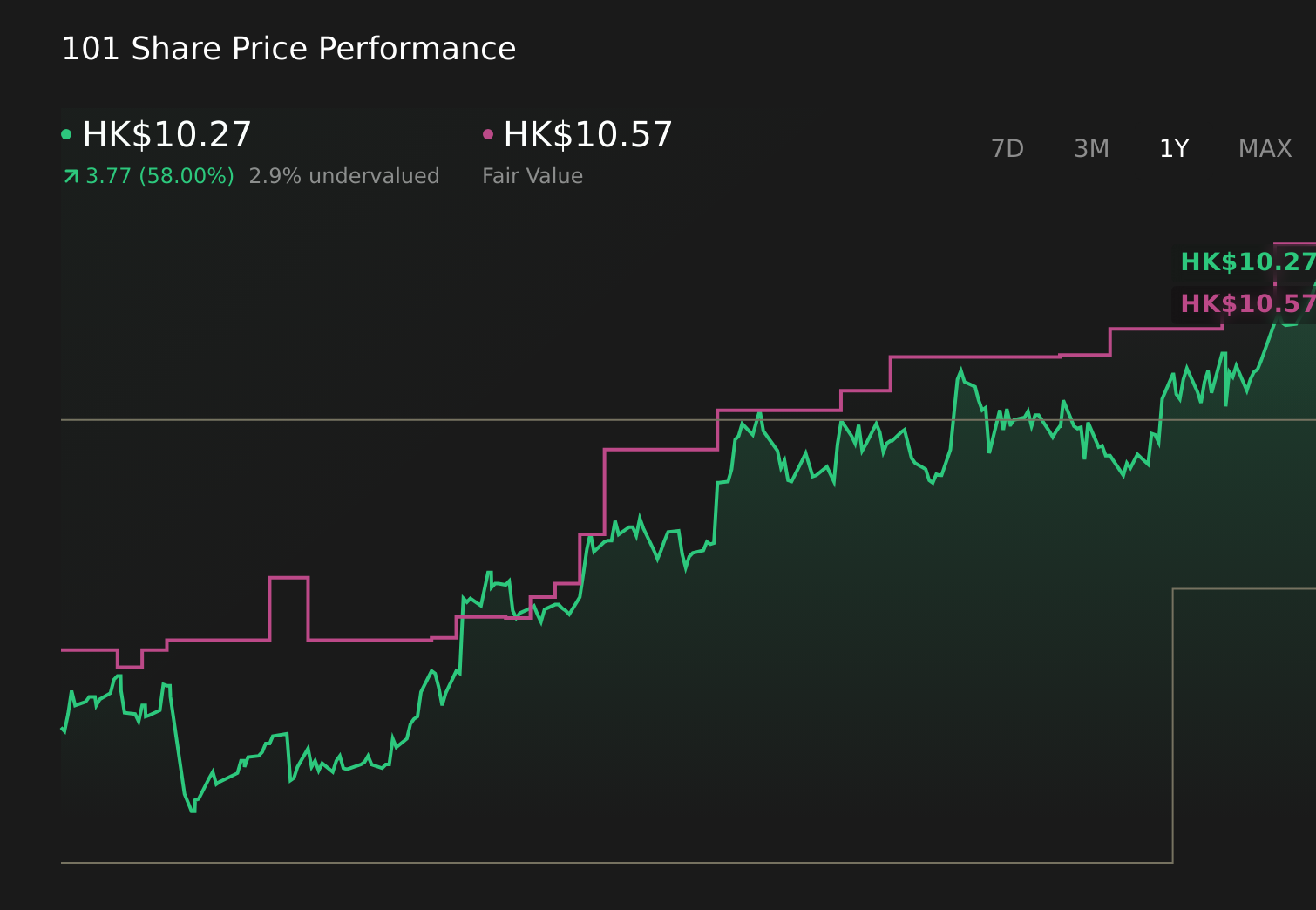

Hang Lung Properties’ narrative projects HK$12.7 billion revenue and HK$4.1 billion earnings by 2028.

Uncover how Hang Lung Properties’ forecasts yield a HK$10.57 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue would shrink about 0.4% a year and still reach roughly HK$11.4 billion by 2028, and the latest stamp duty shift plus REIT policy changes could push that even lower, especially if you are worried about long term demographic and e commerce headwinds in Mainland China.

Explore another fair value estimate on Hang Lung Properties – why the stock might be worth just HK$10.57!

Form Your Own Verdict

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don’t miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hang Lung Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com