(Bloomberg) — Corporate America just delivered one of the strongest earnings seasons in recent memory, but you wouldn’t know it looking at the stock market.

Companies in the S&P 500 grew earnings by 13% in the fourth quarter, almost six percentage points better than expected. They also served up optimism about the coming year. The number of firms in the Russell 3000 Index that raised guidance outstripped those cutting it by four to one — a level last seen in the aftermath of recessions or after the 2018 tax reform, according to Jefferies Financial Group Inc. data.

Most Read from Bloomberg

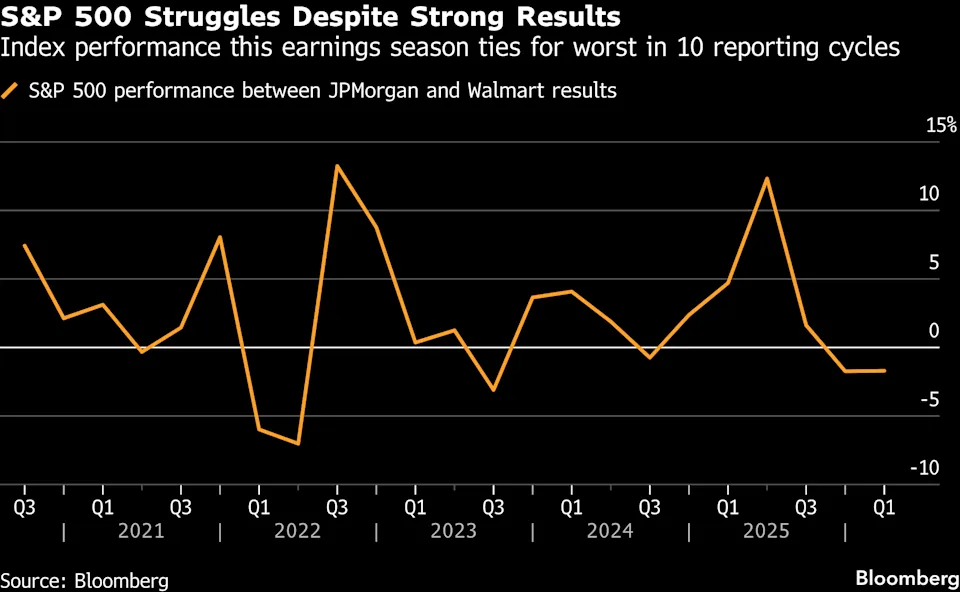

And yet, in the six weeks bookended by reports from JPMorgan Chase & Co. and Walmart Inc., the S&P 500 fell 1.7% — tied for the worst performance during earnings in the past 10 quarters.

Part of the problem arises from where stocks were when earnings started — essentially at a record thanks to bets on artificial intelligence and signs of solid consumer spending. More alarming, though, has been the swirl of uncertainty that has disoriented investors in recent weeks.

The monolithic AI trade, where everything went straight up, morphed into a hunt for winners and losers before shifting again into what’s being called the “scare trade” — a rapid repricing of industries thought to be vulnerable to the technology’s applications.

At the same time, the likelihood of a US invasion of Iran and the implications for the global energy market have forced some investors into safer bets. Trouble at Blue Owl Capital Inc. has also sparked worries over private credit firms.

“Perhaps we are in a buy the rumor, sell the news era for markets, where the big AI/Magnificent Seven bull run over the past three years has driven up expectations to a fever pitch,” Michael Bailey, director of research at Fulton Breakefield Broenniman, said about the disconnect between earnings success and market moves. “In other words, a ‘beat and raise’ quarter is now table stakes, rather than a reason to celebrate.”

Results have been solid but uncertainty around elements like AI and private credit have “dampened” multiples that investors have been willing to pay for sectors like software and fintech, said Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute.

This has caused the S&P 500 to “go sideways,” he added. And while other sectors, including industrials and energy, have gotten higher multiples due to a greater certainty and solid results, Samana notes these areas do not have as large a weighting.