According to data compiled by the Gasgoo Automotive Research Institute, China’s ADAS supply chain landscape showed a clear competitive structure in January 2026. Local players have already established a dominant position in segments such as air suspension, LiDAR, HD map, and high precision positioning. Meanwhile, in areas including driving ADAS, forward-facing cameras, and APA solution, global giants continue to lead, with China’s local suppliers rapidly catching up.

This market dynamic reflects the steadily strengthening core competitiveness of China’s automotive supply chain as electrification and intelligence continue to converge at a deeper level. It not only lays a solid foundation for the industry’s transition toward higher-level intelligent connectivity, but also provides important insights into the future development trends of China’s auto components sector.

Top air suspension system suppliers

Tuopu Group: 55,265 sets installed, 39.7% market share

KH Automotive Technologies: 38,309 sets installed, 27.6% market share

Baolong Automotive: 35,609 sets installed, 25.6% market share

Vibracoustic: 4,375 sets installed, 3.1% market share

Continental: 3,602 sets installed, 2.6% market share

Others: 1,881 sets installed, 1.4% market share

In January 2026, China’s air suspension market remained dominated by local suppliers, with a highly concentrated competitive landscape. Tuopu Group led the market with 55,265 sets installed (39.7% share). KH Automotive Technologies and Baolong Automotive ranked second and third, with 38,309 and 35,609 sets installed, accounting for 27.6% and 25.6% of the market, respectively. Together, the three players held over 92% of the market, reflecting a clear and stable competitive hierarchy.

By contrast, global suppliers such as Vibracoustic and Continental saw their competitiveness weaken , with installations of 4,375 and 3,602 sets, respectively, accounting for a combined market share of just 5.7%. Meanwhile, other small and mid-sized suppliers recorded only 1,881 sets installed, representing a mere 1.4% share, highlighting the difficulty of breaking through.

Overall, China’s air suspension market had largely completed localization substitution by January 2026, with the market share of foreign and smaller players continuing to be squeezed, resulting in a highly consolidated competitive landscape.

Top LiDAR suppliers

Huawei Technologies: 146,899 units installed, 39.9% market share

Hesai Technology: 115,985 units installed, 31.5% market share

Seyond: 60,083 units installed, 16.3% market share

RoboSense: 37,053 units installed, 10.1% market share

Others: 8,028 units installed, 2.2% market share

In January 2026, China’s LiDAR market maintained strong growth, with a competitive landscape characterized by high concentration at the top and leadership from local suppliers. Huawei Technologies ranked first with 146,899 units installed (39.9% share). Leveraging advantages in sensing accuracy, cost control, and automotive-grade reliability, its products have become a core choice for advanced intelligent driving solutions adopted by multiple automakers. Hesai Technology followed with a 31.5% share, and together the two China’s local players accounted for over 70% of the market, shaping the overall competitive landscape.

Seyond and RoboSense ranked third and fourth with market shares of 16.3% and 10.1%, respectively, forming the core supply matrix of China’s LiDAR market alongside the leading players. Overall, local suppliers continue to consolidate their market leadership through rapid technology iteration and expanding production capacity. Meanwhile, the “primary LiDAR + blind-spot LiDAR” product strategy has become a key lever for top vendors to grow share, further accelerating LiDAR penetration in intelligent vehicles.

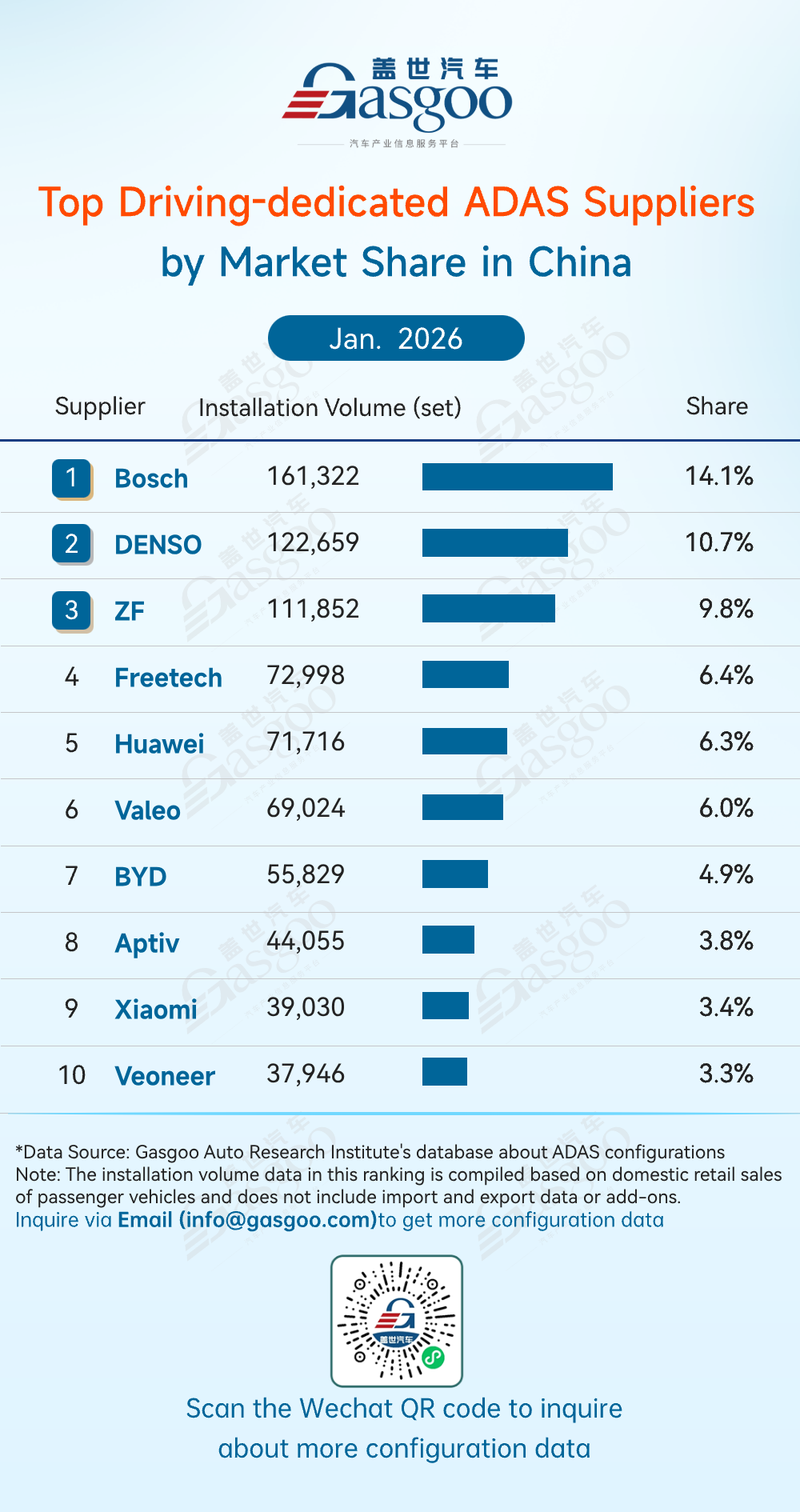

Top driving-dedicated ADAS suppliers

Bosch: 161,322 sets installed, 14.1% market share

DENSO: 122,659 sets installed, 10.7% market share

ZF: 111,852 sets installed, 9.8% market share

Freetech: 72,998 sets installed, 6.4% market share

Huawei Technologies: 71,716 sets installed, 6.3% market share

Valeo: 69,024 sets installed, 6.0% market share

BYD: 55,829 sets installed, 4.9% market share

Aptiv: 44,055 sets installed, 3.8% market share

Xiaomi: 39,030 sets installed, 3.4% market share

Veoneer: 37,946 sets installed, 3.3% market share

In January 2026, China’s driving ADAS market continued to be led by international giants, while Chinese suppliers accelerated their catch-up. Bosch ranked first with 161,322 sets (14.1% share) installed. DENSO and ZF followed with market shares of 10.7% and 9.8%, respectively, forming the leading tier together with Bosch.

China’s local suppliers including Freetech, Huawei Technologies, and BYD ranked among the top players. Freetech placed fourth with a 6.4% share, while Huawei Technologies and BYD ranked fifth and seventh with 6.3% and 4.9%, respectively. As a new entrant, Xiaomi EV entered the top 10 with a 3.4% share, reflecting strong local advantages in algorithm iteration, vertical integration, and rapid market response.

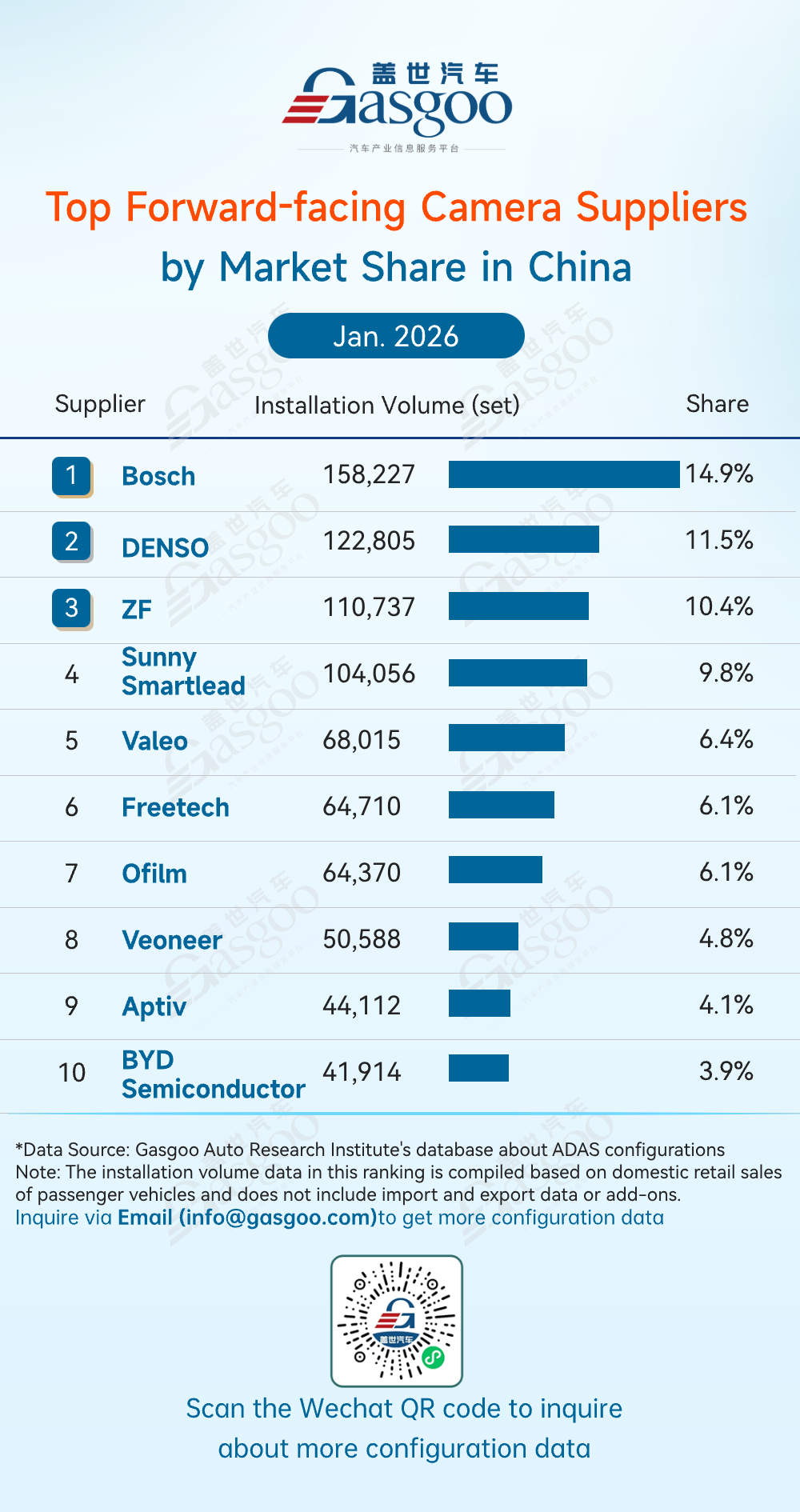

Top forward-facing camera suppliers

Bosch: 158,227 sets installed, 14.9% market share

DENSO: 122,805 sets installed, 11.5% market share

ZF: 110,737 sets installed, 10.4% market share

Sunny Smartlead: 104,056 sets installed, 9.8% market share

Valeo: 68,015 sets installed, 6.4% market share

Freetech: 64,710 sets installed, 6.1% market share

Ofilm: 64,370 sets installed, 6.1% market share

Veoneer: 50,588 sets installed, 4.8% market share

Aptiv: 44,112 sets installed, 4.1% market share

BYD Semiconductor: 41,914 sets installed, 3.9% market share

In January 2026, China’s forward-facing camera market continued to be led by global giants, while local suppliers accelerated their penetration. Bosch ranked first with 158,227 sets installed (14.9% share), remaining an industry benchmark thanks to its strong technology foundation and global supply capabilities. DENSO and ZF followed with market shares of 11.5% and 10.4%, respectively, forming the leading tier together with Bosch. The three players jointly accounted for 36.8% of the market.

Sunny Smartlead ranked fourth with a 9.8% market share. Other local suppliers, including Freetech, Ofilm Autolink, and BYD Semiconductor, also entered the top ten with shares of 6.1%, 6.1%, and 3.9%, respectively, leveraging advantages in cost control, algorithm iteration, and scenario-based adaptation.

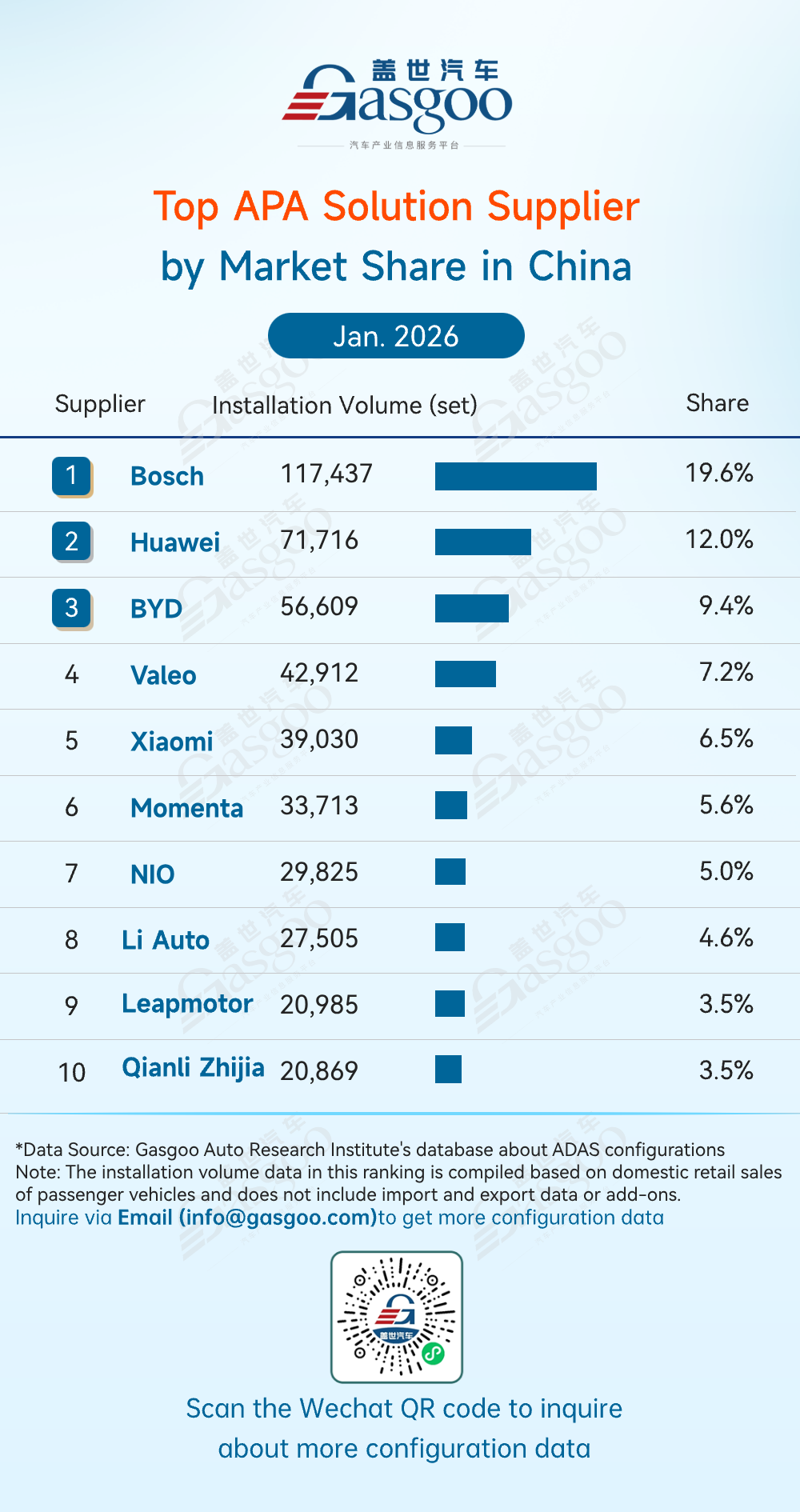

Top APA solution suppliers

Bosch: 117,437 sets installed, 19.6% market share

Huawei Technologies: 71,716 sets installed, 12.0% market share

BYD: 56,609 sets installed, 9.4% market share

Valeo: 42,912 sets installed, 7.2% market share

Xiaomi EV: 39,030 sets installed, 6.5% market share

Momenta: 33,713 sets installed, 5.6% market share

NIO: 29,825 sets installed, 5.0% market share

Li Auto: 27,505 sets installed, 4.6% market share

Leapmotor: 20,985 sets installed, 3.5% market share

Qianli Zhijia: 20,869 sets installed, 3.5% market share

In January 2026, China’s APA solution market was led by international giants, while domestic suppliers accelerated their catch-up. Bosch ranked first with 117,437 sets installed (19.6% share). Huawei Technologies and BYD followed with shares of 12.0% and 9.4%, respectively, highlighting the strong competitiveness of local players in intelligent parking and confirming the ongoing rise of China’s local market share.

The top three suppliers—Bosch, Huawei Technologies, and BYD—together held over 40% of the APA market, highlighting high concentration. Overall, competition is shifting from basic functionality to scenario coverage, user experience, and algorithms, with China’s local suppliers driving technological independence and ecosystem growth in China’s intelligent parking market.

Top HD map suppliers

AutoNavi: 87,189 sets installed, 44.0% market share

Tencent: 29,825 sets installed, 15.1% market share

Langge Technology: 28,022 sets installed, 14.2% market share

NavInfo: 18,608 sets installed, 9.4% market share

Others: 34,303 sets installed, 17.3% market share

In January 2026, China’s high-definition map market remained highly concentrated and domestically dominated. AutoNavi led with 44.0% share (87,189 sets), followed by Tencent, Langge Technology, and NavInfo with 15.1%, 14.2%, and 9.4%, respectively. Other suppliers held 17.3%. The market has largely completed Chinese replacement, with foreign brands nearly absent. AutoNavi’s lead, supported by data accuracy, update frequency, and automotive-grade compatibility, sets a high benchmark, while Tencent and Langge Technology continue to compete through differentiated solutions, reinforcing the top-three structure and solid market barriers.

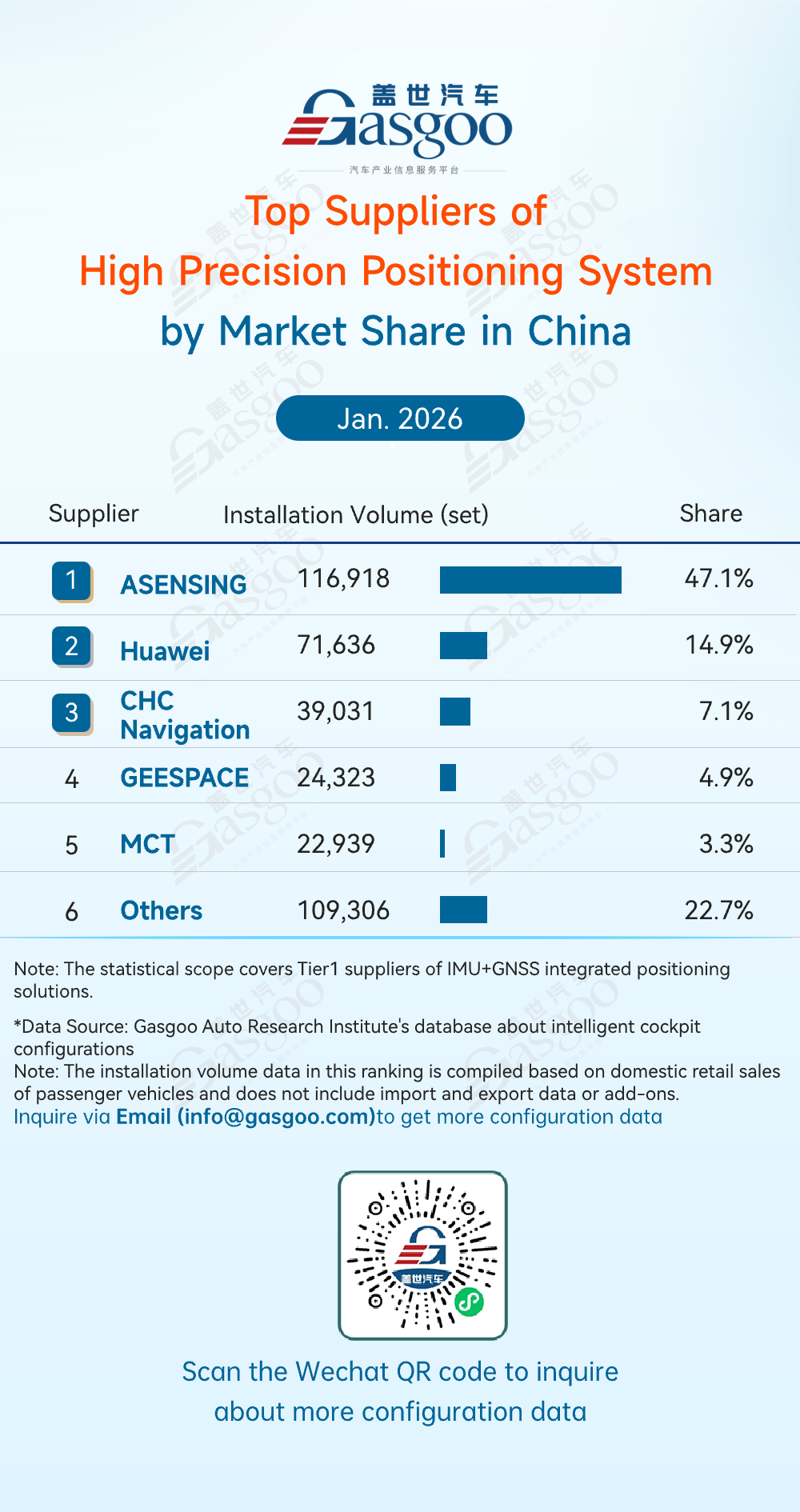

Top suppliers of high precision positioning system

ASENSING: 116,918 sets installed, 47.1% market share

Huawei: 71,636 sets installed, 14.9% market share

CHC Navigation: 39,031 sets installed, 7.1% market share

GEESPACE: 24,323 sets installed, 4.9% market share

MCT: 22,939 sets installed, 3.3% market share

Others: 109,306 sets installed, 22.7% market share

In January 2026, ASENSING led China’s high precision positioning market with 47.1% share (116,918 sets), capturing nearly half of the market. Huawei, CHC Navigation, GEESPACE, and MCT followed, leveraging fusion positioning, multi-source perception, and automotive-grade reliability to serve advanced intelligent driving solutions. Other suppliers held 22.7%, showing the market remains diversified and open to new entrants.