Earlier this month, Plug Power (PLUG +0.93%) investors received some great news: The company’s 50-megawatt (MW) hydrogen electrolyzer project in Australia is expected to move into the execution phase. This essentially clears the way for Plug Power to deliver on its end of the bargain and book the related revenue.

While Plug Power has completed other projects elsewhere in Australia, this electrolyzer project is now that country’s largest renewable hydrogen project to reach this level of development. Orica, the customer — a large mining conglomerate that bills itself as the “world’s largest mining-dedicated producer of sodium cyanide, supporting gold processing, silver recovery and other mineral extraction operations” — operates an existing ammonia production facility on Kooragang Island.

Currently, that facility produces most of its electricity from natural gas. Plug Power’s proton exchange membrane (PEM) electrolyzer will use renewable energy sources to produce hydrogen fuel, offsetting around 7.5% of the facility’s natural gas usage.

To put this project into perspective, Plug Power has now deployed around 320 MW of its GenEco electrolyzer systems across six continents. For comparison, one of Plug Power’s biggest installed systems is a 100-MW Galp project in Portugal. That system is now one of Europe’s largest electrolyzer installations. It is expected to be fully online by the end of this year. So while this 50-MW system in Australia is meaningful, it is not a game changer in any large sense.

Today’s Change

(0.93%) $0.02

Current Price

$2.17

Key Data Points

Market Cap

Day’s Range

$2.08 – $2.26

52wk Range

$1.39 – $4.58

Volume

56.9M

Avg Vol

70.6M

Gross Margin

-2565.51%

Still, Plug Power’s management team wants this development to convince investors of its intended growth trajectory. As a press release reads, “The HVHH project adds to Plug’s growing portfolio of landmark hydrogen projects … as the company’s global pipeline continues to advance from development into execution.”

Should investors buy into the hype? There’s still one clear reason to remain cautious.

Here’s why I’m still staying away from Plug Power stock

Plug Power is clearly gaining traction with its GenEco hydrogen electrolyzers. Last year, the company delivered 185 MW of GenEco systems, a 203% growth over the previous year. The company’s project pipeline suggests this growth will continue. In April, for example, Plug Power was selected to deliver a 275-MW GenEco PEM electrolyzer system in Canada.

This project alone, when delivered, would give the company positive year-over-year growth. Other projects in the pipeline, including its Australian 50-MW system, will only further those growth rates.

Image source: Getty Images.

There are concerns about the long-term competitiveness of Plug Power’s PEM systems. My biggest worry is simply shareholder dilution. Plug Power’s management team seems to be taking profitability seriously. Last quarter, losses narrowed significantly following large improvements in gross margins.

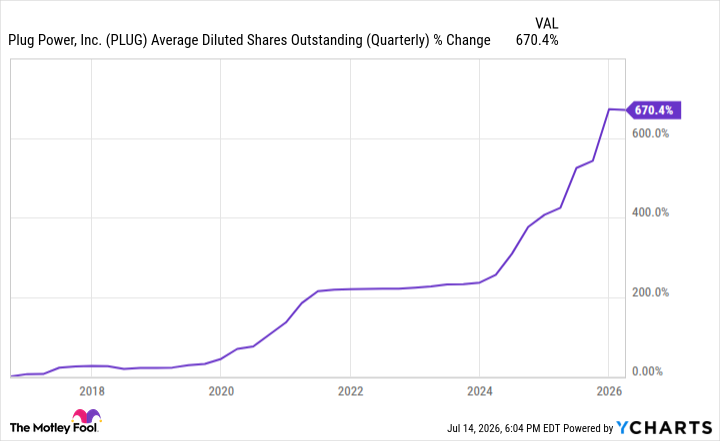

PLUG Average Diluted Shares Outstanding (Quarterly) data by YCharts.

However, net losses continue to accumulate, forcing the company to sell more stock to stay afloat. Over the past five years, Plug Power’s outstanding share count has soared by nearly 700%. Over the past 12 months alone, diluted shares are up roughly 20%. I expect more dilution to occur until the company is sustainably profitable.

So the issue isn’t whether Plug Power is gaining market traction. Rather, it’s a question of whether this growth can offset ongoing shareholder dilution. While Plug Power’s business seems to be improving, I’m still comfortable remaining on the sidelines until the financials have stabilized.