Is There Now An Opportunity In Diageo (LSE:DGE) After The Recent Share Price Slump

Uncategorized

Is There Now An Opportunity In Diageo (LSE:DGE) After The Recent Share Price Slump

012 mins

Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

If you are wondering whether Diageo’s current share price reflects its long term potential, you are not alone. This article will walk through what that price might really imply about value.

The stock has faced heavy pressure recently, with a 5.2% decline over the last week, 13.3% over the past month and 28.2% over the past year. This comes alongside a 52.0% return over three years and 42.4% over five years.

These moves sit against a backdrop of ongoing investor debate about premium spirits demand, cost pressures and how consumer brands are being valued more broadly. Recent coverage has focused on how global drinks groups are being priced relative to their brand strength and cash generation, which gives helpful context when you look at Diageo’s own numbers.

On our checks, Diageo scores 4 out of 6 on valuation, and you can see the breakdown in our valuation score. Next we will look at what different valuation methods suggest about the shares and then finish with a way of thinking about value that goes beyond any single model.

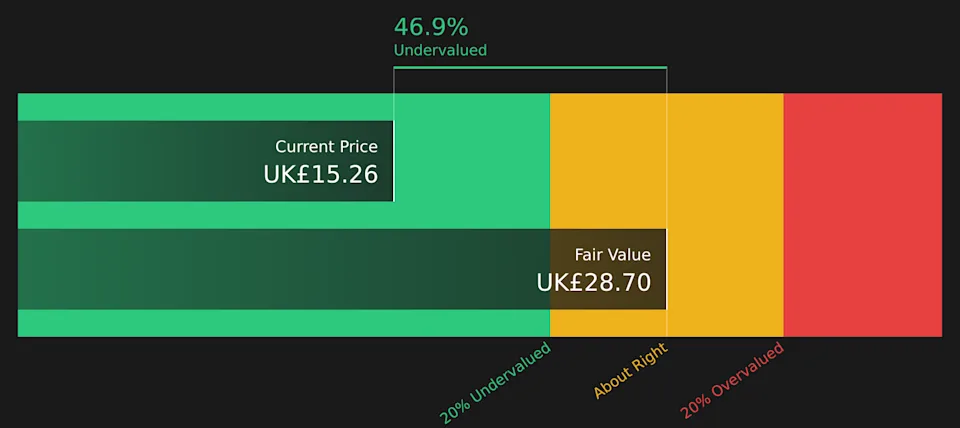

A Discounted Cash Flow, or DCF, model takes estimates of the cash a company might generate in the future and discounts those cash flows back to today, to arrive at an estimate of what the business could be worth now.

For Diageo, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month Free Cash Flow is about US$2.6b. Analysts have provided explicit forecasts out to 2030, with projected Free Cash Flow of US$3.9b in that year. Beyond the analyst horizon, Simply Wall St extrapolates further annual cash flows using modest growth assumptions to complete a ten year view.

When all these projected cash flows are discounted back and added together, the model estimates a fair value of £28.70 per share. Compared with the current share price, this implies an intrinsic discount of 46.9%, which indicates that the shares are trading materially below this DCF estimate.

For a profitable company like Diageo, the P/E ratio is a useful way to think about what investors are paying for each unit of current earnings. It ties the share price directly to the bottom line, which is usually more stable than sales or book value for mature consumer brands.

What counts as a “normal” or “fair” P/E depends on two big things: growth expectations and risk. Higher expected earnings growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk tends to point to a lower one.

Diageo currently trades on a P/E of 18.82x, compared with a Beverage industry average of about 17.05x and a peer average of 16.71x. Simply Wall St’s Fair Ratio for Diageo is 24.28x. This Fair Ratio is a proprietary estimate of the P/E you might expect given factors like earnings growth, profit margins, industry, market cap and risk profile. Because it blends these company specific drivers rather than just comparing to broad group averages, it can offer a more tailored view than simple peer or industry checks.

Set against the Fair Ratio of 24.28x, Diageo’s current 18.82x P/E suggests the shares are trading below that implied level.

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are Simply Wall St Community tools that let you tell the story behind your numbers by linking your view of Diageo’s future revenue, earnings and margins to a financial forecast, a fair value, and then a clear buy or sell framework that continuously updates as news or earnings arrive. You can, for example, pick a more optimistic Diageo Narrative that lines up with a Fair Value near the £27.32 bullish target, or a more cautious one closer to the £17.19 bearish end. You can then compare each Fair Value to today’s £20.38 share price and quickly see which story you feel most comfortable relying on for your own decisions.

For Diageo however we will make it really easy for you with previews of two leading Diageo Narratives:

🐂 Diageo Bull Case

Fair value: £20.01 per share

Implied discount to this fair value at the last close of £15.26: about 24%

Assumed long term revenue growth in the model: 1.35%

Focuses on premium brands, category expansion and product development to support revenue, margins and portfolio breadth as consumer tastes evolve.

Highlights efforts to sharpen marketing, improve commercial execution and simplify the asset base, with an eye on cash generation and return on invested capital.

Flags risks from moderation in alcohol consumption, regulation, emerging market volatility and competition in low and no alcohol, and frames the consensus analyst target of £23.54 within those assumptions.

🐻 Diageo Bear Case

Fair value: £14.70 per share

Implied premium to this fair value at the last close of £15.26: about 4%

Assumed long term revenue growth in the model: 2.05% decline

Starts from a cautious view that health trends, moderation and regulation could limit volumes, with cost inflation and competition from alternatives weighing on pricing power.

Assumes slower revenue progress and a lower future P/E multiple of 14.72x, which pulls the implied value down toward £14.70 even though margins in the model are not especially weak.

Recognises that premium brands, emerging market exposure and portfolio moves could still support earnings, but argues that a lower valuation multiple may better reflect execution and demand risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include DGE.L.