Stocks just suffered their worst day in weeks as the data hinted the US economy may not be slowing toward a downturn so much as overheating into one.

- The S&P 500 fell the most in a single day since mid-May, ending a nine-day grind to record highs

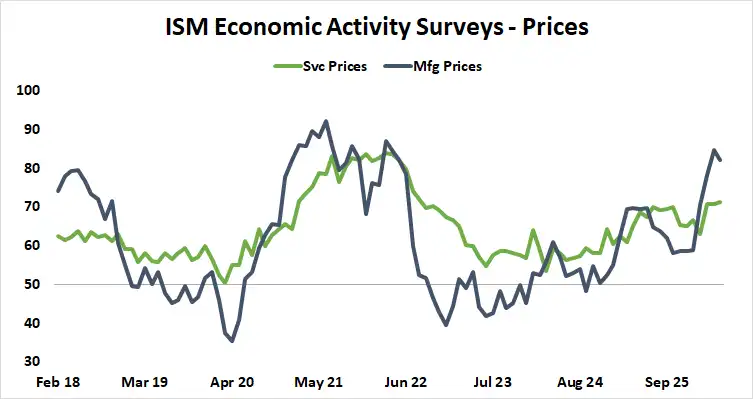

- ISM services PMI growth held up, but employment kept contracting as price pressure neared COVID-era extremes

- Is the real risk a downturn driven not by fading demand but by an economy overheating under strain?

Wall Street finally flinched. The bellwether S&P 500 suffered its largest single-day drawdown since mid-May, ending a nine-day grind to record highs, as a jump in crude oil and a telling set of economic data revived fears about inflation and interest rates. The catalysts were nothing equities had not shrugged off for weeks. What changed is that stocks chose to care — joining the warning every other major market has been sounding.

Stocks join the warning other markets keep sounding

The selloff has not yet broken the trend. The series of higher highs and higher lows that defines the advance since late March remains intact, with former resistance turned support as the line in the sand. For the S&P 500, that looks to be at about 7550. A close below that would set the first lower low and signal a larger reversal. So far, the damage is a single brutal session rather than a confirmed turn, but it stands out plainly against the slow grind that preceded it.

Everywhere else, the “Iran war trade” simply extended. Treasury bond prices were rejected at former range support turned resistance and resumed their slide, pushing yields higher. Gold leaked lower toward support near $4,400/oz. The US dollar broke out of the congestion range that had contained it since mid-April, a far more convincing move after weeks of failed attempts to hold above resistance.

All of it traces to crude oil, climbing for a third straight day and locked in a wartime range with a floor near $80 to $85 a barrel for West Texas Intermediate (WTI) — about $20 above its pre-war level. With energy stuck high, the inflation implication never faded, which is why these markets never unwound their war-trade moves. Only stocks continued to blissfully levitate higher past their pre-war highs, perhaps until today.

The data says the economy is overheating, not cooling

Today’s service sector purchasing managers index (PMI) data from the Institute for Supply Management (ISM) may have made a difference. The headline reading printed a bit better than expected, but as with the manufacturing survey earlier in the week, the real story lay under the hood. Growth held up and new orders improved, but employment stayed in contraction mode while the prices component registered the strongest inflation since near the COVID-19 pandemic peaks of mid-2022. Manufacturing’s inflationary surge was even more aggressive.

Stitch the surveys together and a striking picture emerges. For roughly three years, the US economy has grown at a fairly steady pace, carried by the dominant services sector. But it has been achieving that same growth with progressively less labor — manufacturing employment has been shrinking for years and services have now joined it — and progressively more inflation, especially since tariffs arrived at the start of 2025 and the US-Iran war layered on this year.

Rising prices often come alongside an economic pickup as demand outruns supply. Here, growth is no faster, yet prices keep climbing. It is as if the economy is straining harder for the same result and overheating despite only modest expansion.

The growth mix confirms the strain

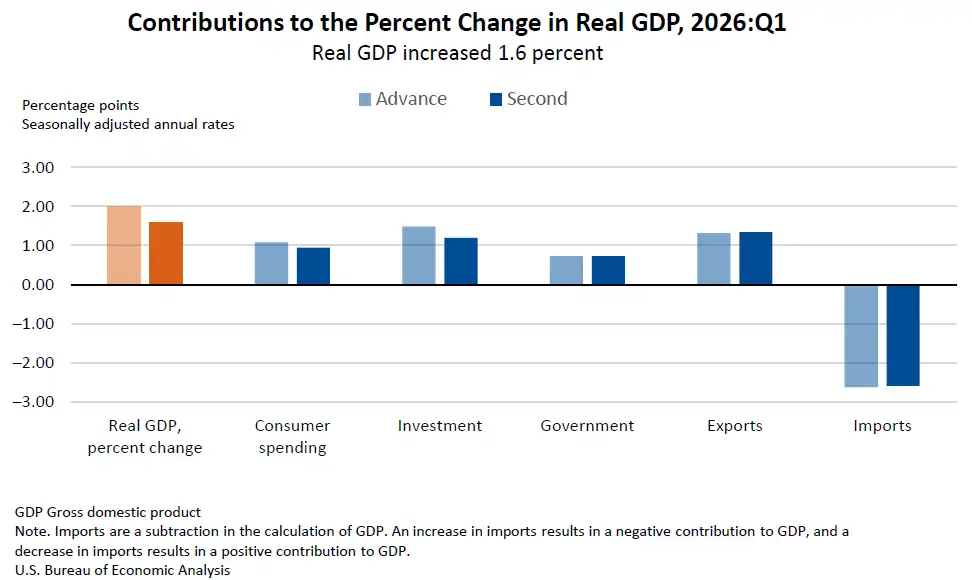

First-quarter US gross domestic product (GDP) data shows the same stress. Business investment, just 14% of the economy, contributed more to the 1.6% growth rate than consumer spending, which is nearly five times larger at 68%. The only way that happens is if investment grows far faster than consumption — the AI data center buildout running hot. Yet even that produced only half the roughly 4% pace for GDP growth logged in the two quarters before a government shutdown detailed the last three months of the year. The economy had to run hot on investment just to manage a modest rebound, and it worked up inflation doing so even before the war’s energy shock entered the picture.

That reframes the AI boom. It has been touted as the engine keeping growth alive in spite of a myriad headwinds, including the Iran war. Rather, the conflict now looks like an amplifier on an economy that already was already spinning up more inflation simply to expand at all.

Data center builders face the same cost pressures that are squeezing consumers. Manufacturers are seemingly hoarding inputs amid worries about still higher prices, thanks to three concurrent forces: tariff policy uncertainty as the levy regime is rebuilt after last year’s setback at the Supreme Court, the war’s energy shock, and the AI buildout’s voracious appetite for materials and chips.

Why an Iran deal would not fix it

Central banks offer no rescue when growth has turned this inflationary. Far from cutting to support soft demand, they are leaning the other way: Fed funds futures now price about a 68% chance of a Federal Reserve rate hike this year, with nearly every other major central bank shifting hawkish in tandem. Weak growth will get no help, because even a modest amount of it is arriving with too much inflation.

That is what makes the setup precarious. A Strait of Hormuz deal — should one ever materialize — would not change the bottom line, because the war amplified an inflation problem rather than strictly causing it. Stocks spent weeks treating the AI buildout as the reason to look away even as inflation preoccupied other markets. The latest ISM data suggests that same buildout is part of the problem, not the escape from it. The trend has not broken yet. But the longer equities cling to a story the rest of the market has abandoned, the more likely it is that the eventual reckoning is violent.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.