If you are wondering whether Four Corners Property Trust is fairly priced or offering hidden value right now, you are not alone.

The stock last closed at US$25.68, with returns of 0.6% over the past week, 3.2% over the past month and 10.5% year to date, alongside a 7.3% decline over the past year and total returns of 16.4% over three years and 16.6% over five years.

Recent news around Four Corners Property Trust has mainly focused on its role as a net lease REIT and how investors are weighing its long term income profile against changing interest rate expectations. This context helps explain why the share price has seen shorter term support, while the longer term return picture looks more mixed.

Our valuation framework gives Four Corners Property Trust a 4 out of 6 score for being undervalued on key checks. Next, we will look at what traditional valuation approaches say about that number, before finishing with a broader way to think about the company’s value.

A Discounted Cash Flow, or DCF, model estimates what a business could be worth today by projecting its future adjusted funds from operations and discounting those cash flows back to the present.

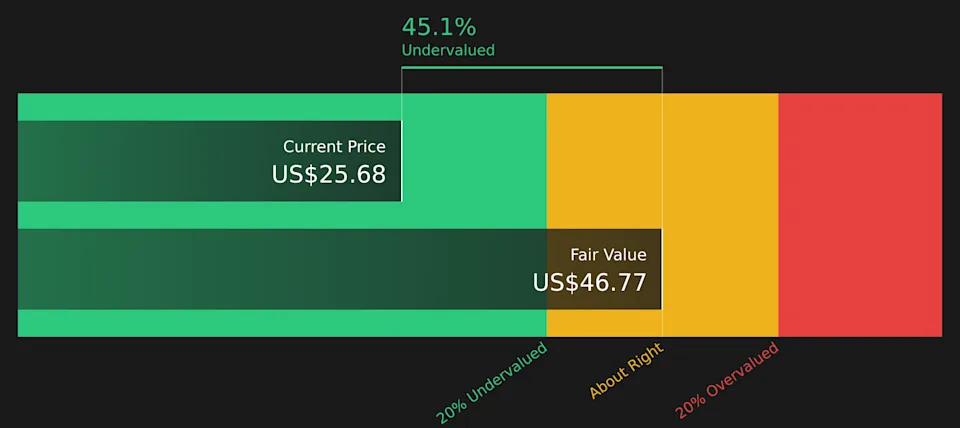

For Four Corners Property Trust, the model uses last twelve months free cash flow of about $183.4 million, expressed as adjusted funds from operations. Analysts provide estimates for several years. For example, Simply Wall St uses projections such as $203.2 million in 2026 and $236.1 million in 2028. Beyond the analyst horizon, cash flows up to 2035 are extrapolated, with each future value discounted to reflect the time value of money and risk.

Adding these discounted cash flows together gives an estimated intrinsic value of about $46.77 per share. Compared with the recent share price of $25.68, the model implies an intrinsic discount of 45.1%, which indicates that the shares are trading at a substantial markdown relative to this cash flow based estimate.

For profitable companies like Four Corners Property Trust, the P/E ratio is a straightforward way to see how much you are paying for each dollar of earnings. It ties the share price directly to today’s earnings, which many investors find easier to relate to than long term cash flow models.

What counts as a “normal” P/E ratio often depends on how the market views a company’s growth prospects and risk profile. Higher expected growth or lower perceived risk can support a higher P/E, while slower expected growth or higher risk can point to a lower one.

Four Corners Property Trust is currently trading on a P/E of 25.08x. That sits above the Specialized REITs industry average P/E of 16.30x and also above the peer group average of 20.06x. Simply Wall St’s Fair Ratio for the stock is 36.20x, which is its proprietary view of what the P/E “should” be after factoring in earnings growth characteristics, industry, profit margins, market cap and specific risks.

This Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for those company specific traits instead of assuming all REITs deserve similar multiples. Since the Fair Ratio of 36.20x is meaningfully higher than the current 25.08x P/E, this framework points to the shares trading below that implied fair level.

Earlier we mentioned that there is an even better way to understand valuation. Narratives let you tell a clear story about Four Corners Property Trust by combining your view on its future revenue, earnings and margins with a financial forecast and a Fair Value, then comparing that Fair Value to the current price, all in an easy tool on Simply Wall St’s Community page that updates automatically as new news or earnings arrive. For example, one investor might build a more optimistic Four Corners Property Trust Narrative closer to the Fair Value of about US$28.14 per share, while another might lean on the lower analyst price target of US$25. You can then see how each story leads to a different decision about whether the current price looks attractive or not.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.