Key Points

-

Amazon’s capital expenditures budget for 2026 is well above Wall Street’s expectations.

-

Investors are overlooking that Amazon’s artificial intelligence-related services are generating high-margin revenue streams.

-

Amazon stock is trading at a steep discount compared to prior levels throughout the AI revolution.

- 10 stocks we like better than Amazon ›

After beginning the year on a strong note, shares of e-commerce and cloud computing giant Amazon (NASDAQ: AMZN) have recently fallen off a cliff.

Let’s dig into why Amazon investors are running for the hills. Is now a good opportunity to buy the dip in Amazon, or is the stock turning into a falling knife?

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Why is Amazon stock dropping?

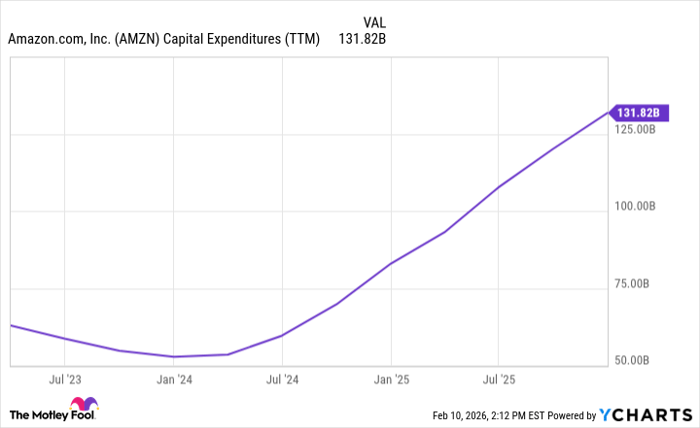

Over the last three years, Amazon has accelerated its capital expenditures (capex) significantly. Rising demand for artificial intelligence (AI) is causing Amazon to invest heavily across the infrastructure value chain — from building data centers, designing its own custom silicon, and complementing these chips with GPUs from Nvidia.

AMZN Capital Expenditures (TTM) data by YCharts

Amazon reported earnings for the fourth quarter and full year 2025 on Feb. 5. Prior to the report, Wall Street was expecting management to guide for around $150 billion in capex this year. With this in mind, investors had sticker shock when the company’s plans for $200 billion capex were revealed.

Is Amazon’s rising infrastructure spend worth it?

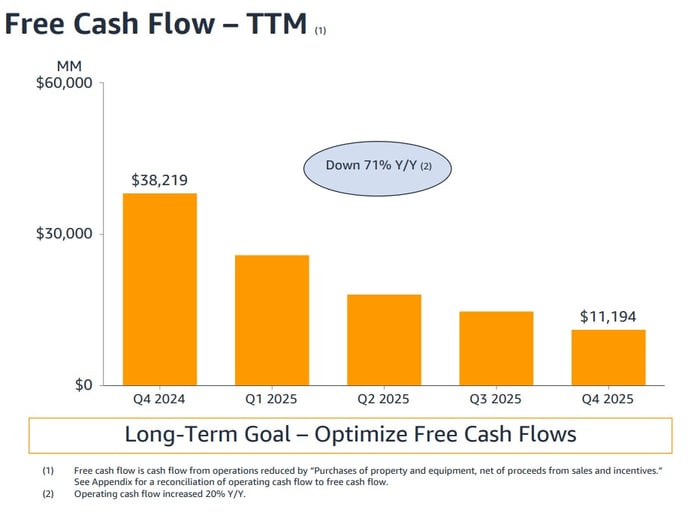

The trends in the chart sum up why Wall Street is getting skittish over Amazon. The inverse correlation between rising infrastructure spend and decelerating cash flow generation is a major concern for investors.

Data source: Amazon investor relations.

Where investors may be missing the mark is looking at Amazon’s revenue growth. Over the last year, sales and operating profits from the Amazon Web Services (AWS) division have consistently risen. In other words, Amazon’s high-margin cloud business is experiencing both accelerating sales and profit margins.

This dynamic is allowing the company to allocate capital across so many different AI-related projects. Building its own data centers and custom chips, alongside its strategic investment in Anthropic, is helping Amazon vertically integrate its AI operations.

In the long run, this should significantly reduce costs and lead to stronger earnings growth. When you think about it this way, Amazon’s playbook to double down on its AI infrastructure roadmap looks savvy. While rising capex may be a near-term dent for free cash flow, the long-term gains are hard to deny.

Should you buy the dip in Amazon stock?

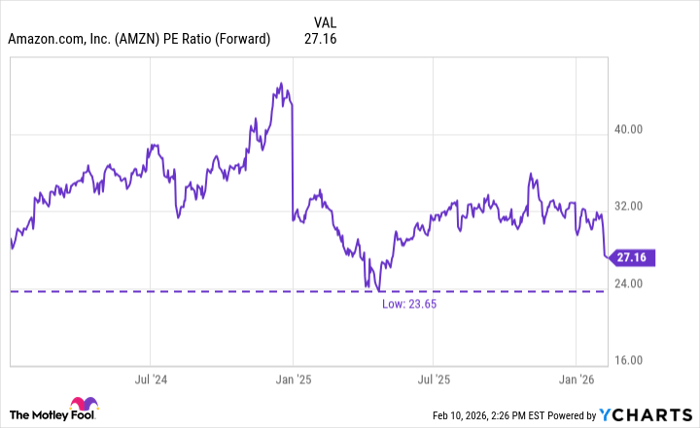

As of this writing, Amazon’s forward price-to-earnings (P/E) is hovering near its lowest level throughout the entire AI revolution.

AMZN PE Ratio (Forward) data by YCharts

Considering sales from AWS are beginning to reaccelerate and are complemented by robust profit margins, I am confident that Amazon’s decision to continue investing in AI infrastructure makes sense strategically. While I understand investor concerns around execution risk, I think Amazon has already done a fine job of mitigating these worries.

To me, the sell-off in Amazon stock is overdone, and the stock looks like a no-brainer right now. Against this backdrop, I’d say Amazon isn’t just a good stock to buy — it’s a great one for long-term investors to buy and hold.

Should you buy stock in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $409,108!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,145,980!*

Now, it’s worth noting Stock Advisor’s total average return is 886% — a market-crushing outperformance compared to 193% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 13, 2026.

Adam Spatacco has positions in Amazon and Nvidia. The Motley Fool has positions in and recommends Amazon and Nvidia. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.