Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

Quilter is back in focus after a fresh round of price target moves, with the new fair value estimate nudged from £1.87 to £2.04 and published targets now stretching from around 170 GBp up to 223 GBp. Those numbers sit alongside a split in analyst opinion, with some seeing room for the share price to close part of the gap to the higher targets, while others argue much of the improvement is already reflected. In the sections that follow, you will see what is driving that debate and how to keep track of the evolving narrative around Quilter.

-

JPMorgan has one of the higher targets on Quilter, lifting its fair value view to 223 GBp from 210 GBp while keeping an Overweight rating, which signals confidence that the shares have room to better reflect its thesis.

-

Citi and Berenberg have also adjusted their targets upward in recent months, with Citi making multiple small increases and Berenberg lifting its target by 20 GBp, which points to a generally constructive stance among part of the analyst group.

-

Barclays, despite raising its target to 170 GBp from 140 GBp, maintains an Underweight rating. This underlines a view that the shares may be pricing in a lot of the potential already.

-

The spread between Barclays at 170 GBp and JPMorgan at 223 GBp highlights a clear divide on valuation and execution risk. This gives you a sense that expectations across the Street are far from aligned.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

We’ve flagged 1 risk for Quilter. See which could impact your investment.

-

Quilter’s Board has recommended a final dividend of 4.3 pence per share for 2025, with an expected total cost of £58 million, subject to shareholder approval at the 2026 AGM.

-

The proposed final dividend is scheduled to be paid on 18 May 2026 to shareholders on the UK and South African registers as of the 17 April 2026 record date.

-

For shareholders on the South African register, the Board has set the final dividend at 94.67035 South African cents per share, based on an exchange rate of 22.01636.

-

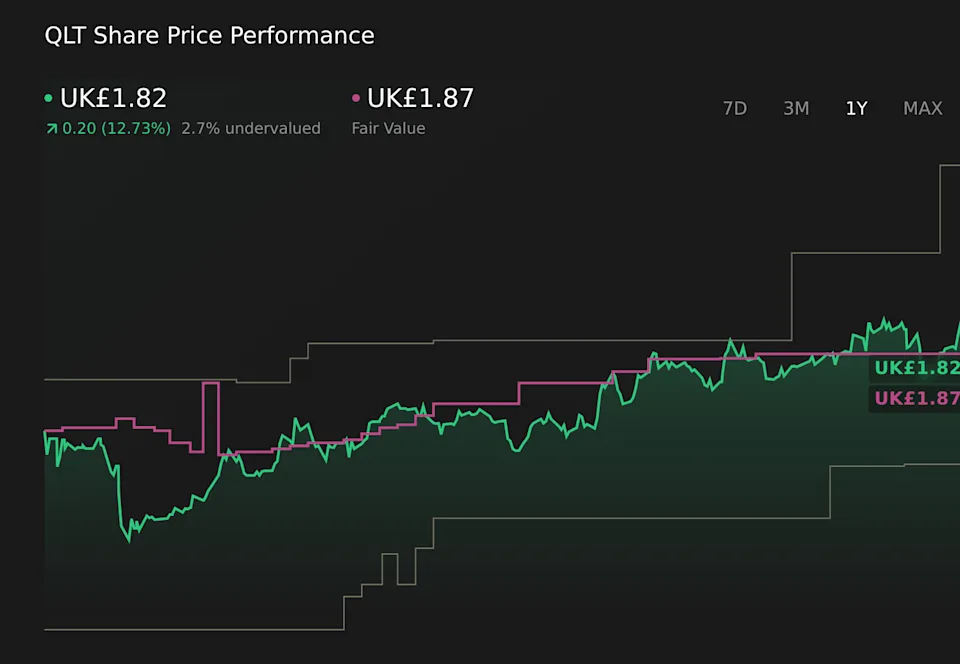

Fair value estimate has moved from £1.87 to £2.04.

-

Forecast revenue contraction has shifted from about a 43.68% decline to a 43.54% decline.

-

Forecast net profit margin has adjusted from 21.25% to 21.27%.

-

The future P/E multiple used has moved from 18.6x to 19.7x.

-

The discount rate used in the model has shifted from 8.66% to 8.36%.