Key Points

-

CEO Elon Musk recently touted enormous potential for Tesla’s robotaxi, artificial intelligence (AI)-powered at-home robots, and solar panels.

-

All these industries, however, are already rife with competition. There’s no assurance Tesla will lead them as it did by ushering electric vehicles into the mainstream.

-

The waiting period between now and when these new initiatives begin making meaningful contributions to the bottom line could be longer and more harrowing than many investors expect.

- These 10 stocks could mint the next wave of millionaires ›

Big changes for Tesla (NASDAQ: TSLA) are afoot. While the company will continue manufacturing electric vehicles, it’s adding solar panels to its mix, hastening the development of its robotaxi technology, and perhaps most amazingly, intends to start selling humanoid household task-tackling robots at an expected price of between $20,000 and $30,000 apiece to consumers by the end of 2027.

Although the company’s been working on all of these initiatives for some time, CEO Elon Musk’s confidence in their readiness was on full display at this year’s annual gathering of world leaders in Davos, Switzerland, held in late January. And as usual, his optimism has been very well verbalized. The company’s “overall shift to an autonomous future” underway now was described as an “infinite money glitch” back in October, suggesting billions of accessible liquidity are in the offing.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Just don’t dismiss the possibility that Tesla’s talkative founder may also simply be trying to divert attention away from the fact that his electric vehicle business is stagnating, biting into its profitability. He might not be diving neck-deep into robotics or solar because he wants to. He may be doing so because he needs to in order to rekindle growth.

And “needing to” isn’t exactly the encouraging sign investors want to see.

Tesla’s all-important EV business is stuck in the mud

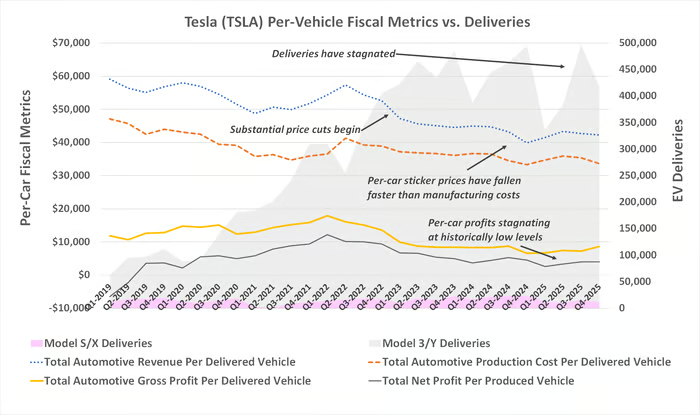

The overarching challenge here is explained with one (relatively) simple chart. That is, even though Tesla’s average per-vehicle production costs have fallen as it makes more of its affordable Model 3 and Model Y cars, it’s not been enough to restore the degree of per-vehicle profits the company was enjoying prior to the beginning of the EV price wars that kicked off in early 2023.

As of the end of last year, the company was only clearing a little over $4,000 per car, versus a net profit of more than $10,000 per vehicle back in 2022. Never even mind the fact that actual production peaked in 2023, when revenue did the same.

Data source: Tesla. Chart by author.

Give credit to its competition, mostly. Numbers from Rho Motion suggest 20.7 million new EV sales were made last year, up 21% from 2024’s count. It’s just that rivals like China’s BYD (OTC: BYDDF), Europe’s Volkswagen (OTC: VWAGY), and domestically, General Motors‘ (NYSE: GM) Chevrolet absorbed all this growth, leaving none for Tesla.

More to the point, it’s arguable that “the brand that mainstreamed electric vehicles by making them cool” is no longer the coolest EV brand to buy. If that’s the case, it’s not an easy fix. Musk may not even be interested in attempting to fix it.

It matters simply because battery-powered automobiles still account for a little more than 70% of Tesla’s revenue.

Meet the new Tesla (same as the old Tesla?)

But does Musk actually need to fix anything if his expectations of autonomous androids, solar panels, and self-driving taxis are on target?

Maybe. There’s certainly no denying solar power is a huge part of the planet’s future. The International Energy Agency says the worldwide amount of energy production coming from renewables should more than double between now and 2030, with solar accounting for 80% of that growth. And as for autonomous taxis, Precedence Research believes the nascent robotaxi business could be worth nearly $190 billion by 2034.

The only real unknown here is the potential of Tesla’s AI-powered robot. Since there’s nothing quite like it, we can only assume Musk’s optimistic assessment that it will be a key part of an “infinite money glitch” means this technology will generate at least as much cash flow as the company can constructively use.

Image source: Getty Images.

There are several critical footnotes to add here, however. Chief among them is that Tesla isn’t the only player — and certainly not the first — in any of these markets, including the robotics arena. Neura, 1X, Atom, and Figure AI are just some other companies with household-minded robots that seem near-ready for launch. It remains to be seen if Tesla can thrive within any of these spaces.

Then there’s the other thing: Elon Musk’s well-documented penchant for overpromising and then underdelivering… at least when it comes to timelines. His plans for a high-speed train — called Hyperloop — and the first manned mission to Mars by 2021 come to mind, for instance.

Tesla’s at-home chore androids could easily hit a similar developmental wall.

At this price, not enough reward for too much risk

There’s the rub for shareholders, of course, made worse by the fact that TSLA stock is already priced at over 200 times this year’s very plausible expected earnings of $2.06 per share. Even if the company trounces analysts’ consensus forecasts, it’s still priced for perfection and for growth that may or may not ever materialize as much as it’s needed to.

In the meantime, Musk is sure to be at least a little bit distracted by the recent merger of SpaceX and xAI, both of which he also leads.

The point is, Tesla appears to be backing away from its breadwinning EV business so it can focus on several other opportunities with completely uncertain payoffs and timelines. Diversifying your profit centers isn’t a bad thing. But, given the speed and sheer uncertainty of so many sudden changes with Tesla, it wouldn’t be crazy to presume that panic is at least part of Musk’s motivation here. It’s a potential problem simply because that’s not what you want to sense or see of the chief executive of any company you’re considering investing in.

This might help drive the point home: Despite all the recent scintillating storytelling of robots, self-driving taxis, and more, the analyst community isn’t swayed. It still says TSLA stock is only worth $422.09 per share, which is 2% from the ticker’s present price, perhaps reflecting the headwind the company’s EV business is now running into. You might want to take that hint.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $474,159!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $48,705!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $414,554!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of February 15, 2026.

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool recommends BYD Company, General Motors, and Volkswagen Ag. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.