Stock market volatility is the new norm, Goldman Sachs says, and it’s not as simple as markets being upset by geopolitical turmoil like the Iran war.

The conflict in the Middle East has fueled the recent spike in equity volatility, Goldman says, but the firm’s macro strategy research team sees an ongoing structural rise in long-term volatility beyond the war’s end.

“We have argued that there are good reasons to expect that equity volatility could move structurally higher over time, even with a benign macro backdrop and even if equity prices continue to rise, as some of the forces that pushed equity volatility higher in the late 1990s as the tech investment boom matured come increasingly into play.”

Goldman’s strategists reexamined the models they use to forecast stock volatility, updating their forecasts for longer-term volatility.

The “obvious” route to higher stock market volatility is cyclical economic deterioration, they say, though they explained that there are other underlying structural forces contributing to their outlook for a longer period of volatility.

“Models of the macro and market drivers of equity volatility suggest that longer-dated implied volatility ‘should’ have been rising in recent years, driven largely by rising equity market concentration and a slowly rising unemployment rate,” the bank said.

Instead of the Iran war, the two biggest drivers of a swingier stock market will be higher market concentration and higher unemployment, in Goldman’s view.

AI-driven market concentration sets up stock volatility

AI has fueled the stock market’s bull run in the past few years as investors pile into the emerging tech, a backdrop that sets up equities for more volatility.

“We think the concentration of value in AI-related areas of the market adds to the risk of higher volatility over time as focus increases on whether the benefits from AI justify that value as the AI cycle matures,” Goldman wrote.

Market concentration has become historically top-heavy as the AI trade fuels gains for the largest companies. The last time the stock market was this concentrated at the top was 1932, during the Great Depression.

This phenomenon was on display earlier this year when AI hype soured, driving major losses in AI stocks and the broader market.

Goldman says market concentration and high valuations are the “non-macro” factors they considered in their volatility model.

“Rising concentration and high valuations are symptoms of this AI-driven market, as they were in the tech boom of the late 1990s,” the note read.

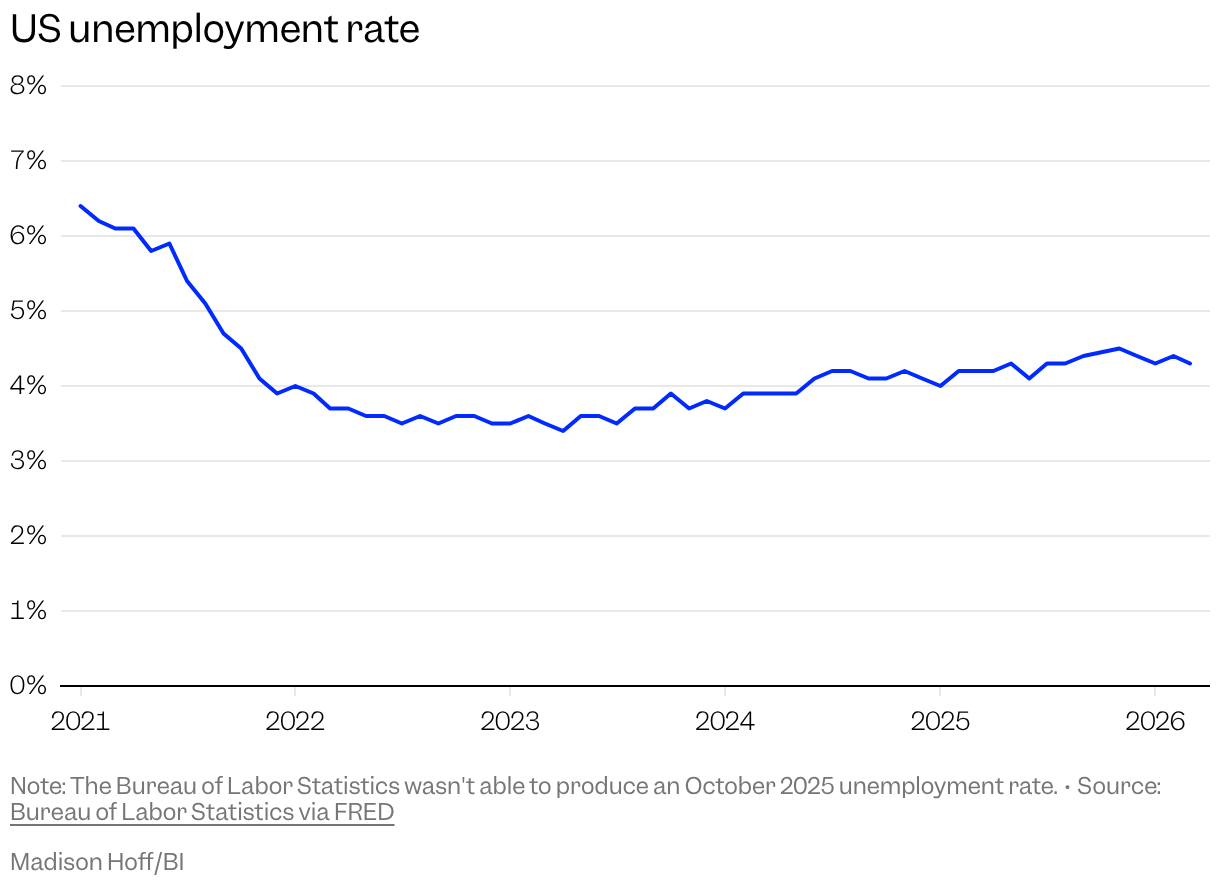

Unemployment data signals an uptrend in equity volatility

Unemployment is the second main driver of equity volatility that Goldman highlighted.

The bank’s volatility model considers levels and changes in the US unemployment rate, with higher unemployment being associated with higher volatility.

“The intuition here is that these measures are indicators of the stage of the economic cycle,” they wrote.

The unemployment rate has risen slowly from 2023 lows.

“We find a statistically significant relationship between volatility in labor market data and equity volatility—the channel here is likely through uncertainty about future outcomes (where higher data volatility is associated with increased uncertainty about the macro outlook),” the bank wrote.